- HRC offers drop, sellers remain focused on booking profits

- Buyers unwilling to engage with higher BF rebar prices

- Need-based trades pressure IF rebar tags, bulk deals absent

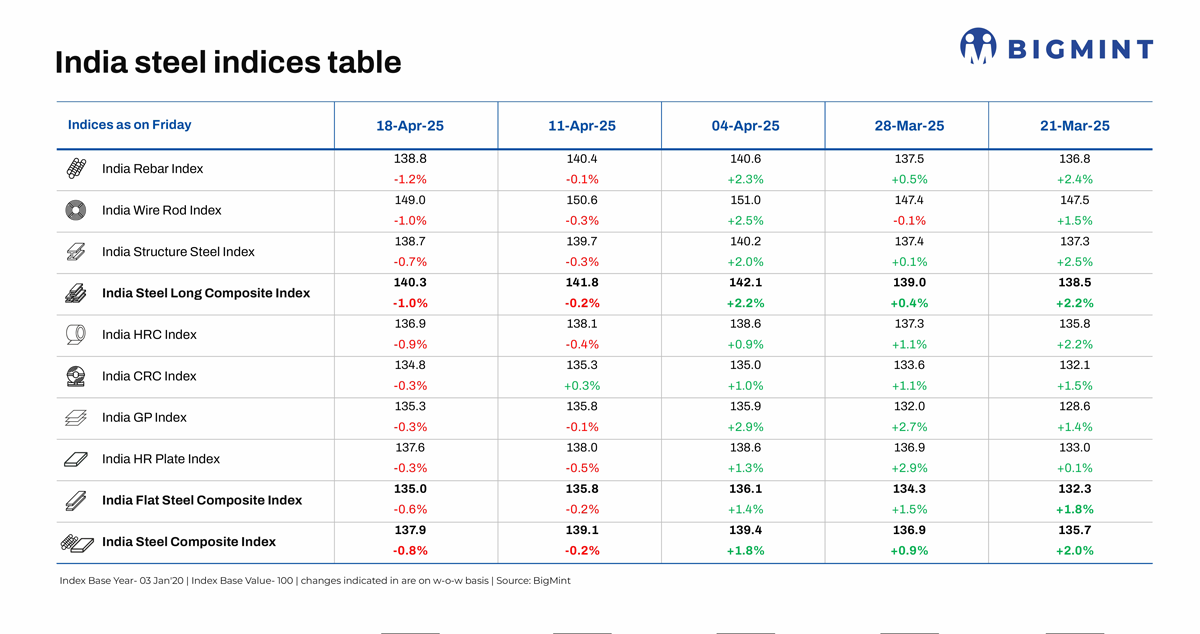

Morning Brief: Lacklustre demand continued to drive down steel prices last week, with BigMint’s India Steel Composite Index, a barometer for the domestic market, declining 0.8% w-o-w to settle at 137.9 points on 19 April 2025.

The flat steel index eroded by 0.6%, weighed down by a 0.9% drop in hot-rolled coils (HRCs). Longs dropped by 1%, with all of its sub-indices losing ground: rebars by 1.2%, wire rods by 1%, and structure steel by 0.7%.

Prices had catapulted upward from end-February, spurred by supply shortages and, subsequently, the safeguard duty recommendation. However, amid muted demand in the end-user segments, trades had failed to keep pace with the increase in pricing. As a result, prices have witnessed corrections since early April.

Factors impacting index last week

Subdued demand pulls down BF rebar tags w-o-w: Trade-level blast furnace (BF) rebar prices declined w-o-w, with tags in Mumbai down by INR 100/tonne (t) ($1/t) w-o-w to INR 57,100/t ($669/t) exy, ex-GST.

Demand was subdued, with buyers unwilling to engage in trades at higher prices. Notably, BF mills had announced a number of hikes earlier last month, and list prices had been raised even at the beginning of April. Cumulatively, trade-level prices in Mumbai had climbed up by roughly INR 4,000/t ($47/t) from end-February to early April.

Project segment prices continued to hover within INR 56,500-57,500/t ($662-673/t) FOR Mumbai, a stable range w-o-w. Demand was moderate.

IF rebar prices decline as trades remain depressed: Trade segment prices of induction furnace (IF) rebars dropped w-o-w, by INR 100/t ($1/t) w-o-w to INR 49,300/t ($577/t) exw-Mumbai.

Trade momentum was moderate, with bulk deals absent, as buyers were uncertain about future price direction and awaited further clarity. While mills were able to secure decent bookings, these deals were closed largely after offers were reduced, at lower values. Need-based buying was observed at higher levels.

Inventory pressure on mills remained minimal, with holding periods averaging 7-8 days.

Trade-level HRC offers drop amid cautious buying: Trade-level HRC offers decreased by INR 150-1,250/t ($2-15/t) w-o-w across markets, with Mumbai registering a drop of INR 600/t ($7/t) to INR 51,300/t ($601/t) exy, ex-GST.

As in the previous week, buyers were conservative with regard to procurement, and distributors received limited inquiries. As a result, suppliers reduced offers, to stimulate trade.

In fact, distributors actively pursued buyers, intent on booking profits. To illustrate, even after the drop, prices (exy-Mumbai) were at least around INR 3,000/t ($35/t) higher than end-February levels. This meant that distributors could secure higher margins by selling off their inventories at these values.

Trades were concluded predominantly at lower prices, and buyers flat-out rejected higher offers. There is an expectation that mills may introduce price support measures to counter the sluggish market momentum.

On the imports front, arrivals of bulk HRCs and plates stood at 93,459 t as of 14 April, based on vessel line-up data from BigMint. Another 82,733 t are expected this month.

HRC export offers to EU remain flat amid holiday mood: Indian HRC (SAE1006) export offers to the EU were stable w-o-w at around $630-635/t CFR Antwerp amid muted buying interest due to the Easter holidays. However, sources suggested that some Indian mills may be holding back allocations, expecting a potential price increase.

Conversely, Indian mills kept HRC offers to the Middle East on pause due to competitive Chinese offers, which dropped by $10/t w-o-w to $480-485/t CFR UAE.

Outlook

In the short term, prices are expected to remain subdued, given that a substantial uptick in end-user consumption is still awaited and the market has been unable to absorb the price hikes seen over the last few weeks. Prices will likely be range-bound as steel supply will remain sufficient. The global trade war and economic uncertainty will affect prices. There is little room for optimism- steel being a deregulated sector is naturally vulnerable to shifting global economic sentiments and trade dynamics.

However, further rate cuts by the RBI are likely to boost domestic consumption and the effects should be visible by the next quarter.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply