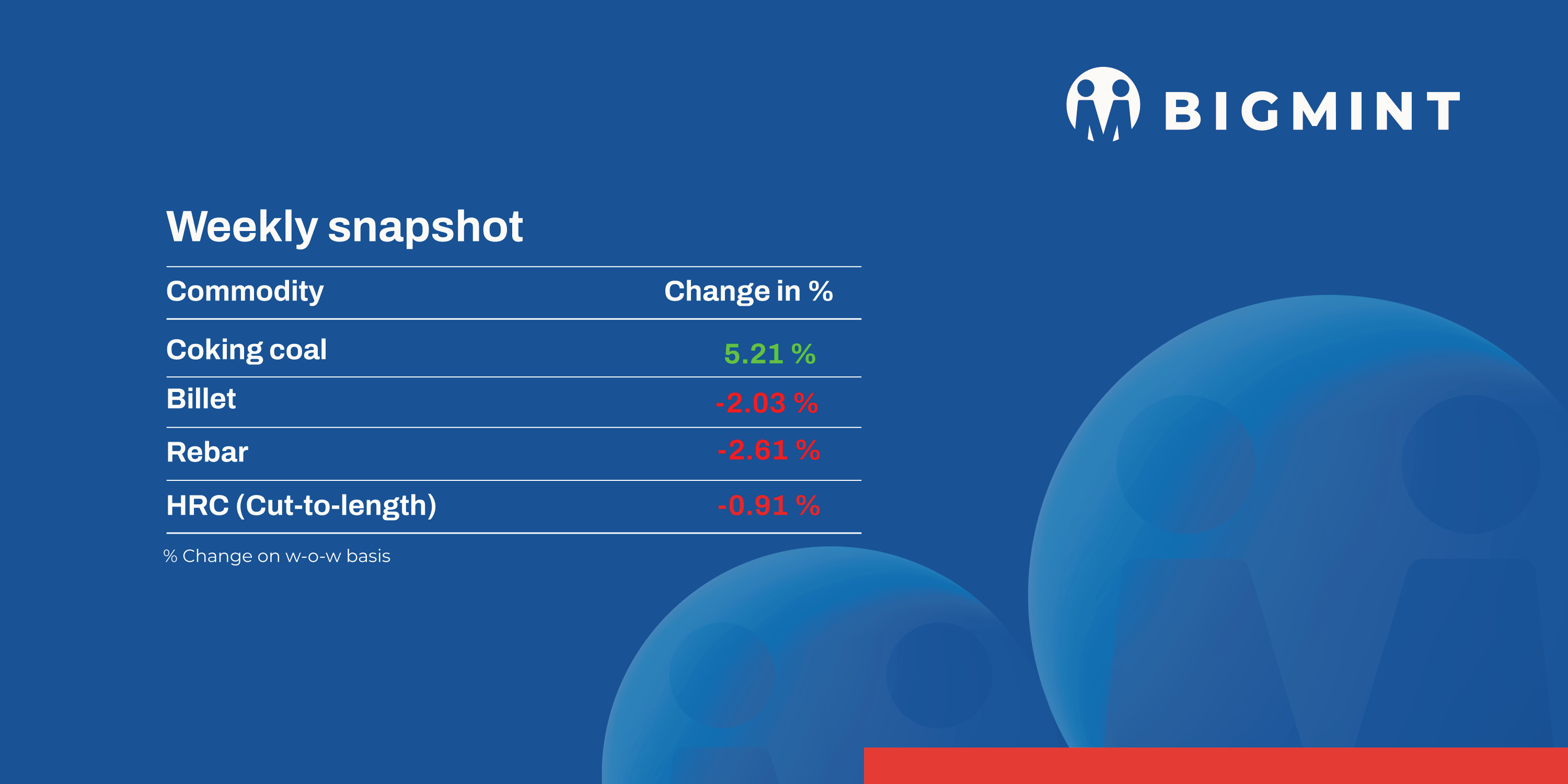

The domestic steel market witnessed a negative trend in prices during week 16 (14 -19 Apr, 2025). Semi-finished steel prices fell in the range of INR 200-1050/tonne (t).

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index dropped by INR 100/t ($1/t) w-o-w to INR 10,150/t ($119/t) DAP Raipur on 18 April. Around 20,000 t pellet (Fe62.5/63%) deals were concluded in Raipur by local and Odisha-based suppliers. Sellers in Raipur maintained their offers, although competitive prices from Odisha mounted pressure on prices.

- OMC scheduled an auction for 2.676 mnt of iron ore (1.141 mnt lumps and 1.535 mnt fines) on 19 April. The miner increased base prices by INR 100/t and INR 350/t m-o-m for fines and lumps, respectively. Prices rose amid the tight availability of higher-grade iron ore in the region. Hike in sponge iron prices m-o-m also supported the hike.

- Freights from the Indian Ocean to China were recorded at $9.6/t, dipping by $0.9/t w-o-w. With global iron ore prices hovering around the $100 mark, charterers exercised caution and refrained from finalising fixtures. However, as iron ore prices are expected to improve, market participants expect a resumption in fixture activity.

Coal

- South African RB2 and RB3 coal prices remained mostly stable across east coast ports amid weak sponge iron demand. Limited buying and a quiet market led to minor price changes, with two RB2 deals reported at INR 8,400/t.

- Met coke prices in India remained unchanged w-o-w despite rising coking coal costs. Domestic BF-grade coke was stable at INR 34,200/t (Jajpur). The imported market was quiet with minimal deals, while Chinese prices saw a slight rebound after long weakness.

- IOCL kept pet coke prices unchanged for all refineries in April. Road and rake rates remained flat, indicating pricing stability in domestic and export markets. Imported US-origin prices fell slightly, while Saudi-origin pet coke held firm on limited supply.

- BigMint’s PHCC index rose by $15/t to $203/t CNF Paradip as Australian supply tightened due to mine disruptions. India’s March coking coal imports rose 23% m-o-m. Australian FOB prices rebounded sharply from March lows, signalling strengthening global fundamentals.

Ferro Scrap

- India’s imported scrap market remained bearish this week, weighed down by weak global cues and volatile domestic steel market sentiments. Shredded offers from the UK/Europe initially hovered at $390/t CFR Nhava Sheva but saw little interest, with buyers aiming below $380/t. Limited trades and a wide bid-offer gap signalled caution.

- Falling domestic rebar prices, rising sponge iron usage, and sufficient inventories weighed on bookings. Australian and UK HMS deals were heard at $350-365/t CFR, but overall demand stayed sluggish.

- Towards the weekend, UK shredded scrap prices fell by 2% w-o-w to $380/t CFR India. The outlook remained cautious amid currency volatility and fears of Chinese billet imports.

- Around 17,500-18,000 t of imported scrap arrived in India, including a bulk shredded cargo of 10,500 t priced between $380-385/t, a partial bulk HMS 80:20 lot of 2,000 t at $380/t, and a partial bulk bonus-grade cargo of 3,000 t at $395/t. Additionally, 1,500-2,000 t of mixed HMS-LMS bundles, MS turnings, and HMS 80:20 also arrived.

Ferro alloys

-

Silico Manganese:Indian silico manganese prices decreased w-o-w by INR 600/t ($7/t) to INR 71,200-71,600/t ($834-839/t) in the key regions of Durgapur, Raipur and Vizag. Fluctuations in domestic steel prices have led to a slowdown in the silico manganese market due to weaker demand from the steel sector.

-

Ferro Manganese:Indian ferro manganese (HC 70%) prices inched down by INR 250/t ($3/t) w-o-w to INR 74,750/t ($875/t) exw in Durgapur. However, prices exw-Raipur, edged down by INR 200/t ($2/t) at INR 74,800/t ($876/t). Prices went down on need-based purchases and market cautiousness.

-

Ferro Silicon:Indian ferro silicon prices declined by INR 1,100/t ($13/t) w-o-w to INR 95,000/t ($1,113/t) exw-Guwahati. Meanwhile, prices were in Bhutan also dipped by INR 500/t ($6/t) at INR 96,000/t ($1,124/t) exw. Prices fell majorly in the northeastern region of India, owing to limited inquiries and a wide gap between bids and offers.

-

Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices inched up by INR 300/t ($4/t) w-o-w to INR 100,600/t ($1,178/t) exw-Jajpur.The ferro chrome market remained stable, as evidenced by Vedanta-FACOR’s auction on 14 April. Market participants are now closely monitoring the Odisha Mining Corporation’s chrome ore auction, scheduled for today, which may impact future pricing.

Semi-Finished Steel

- Indian semi-finished steel prices showed a downtrend w-o-w, as per BigMint assessment. Domestic billet prices in almost all key locations decreased by INR 200-1,050/t, with a major decrease of INR 1,050/t seen in Raigarh. However, sponge iron prices declined by INR 200-1,000/t, with a major decrease of INR 1,000/t seen in the Ramgarh market.

- Indian DRI (Direct Reduced Iron) export offers decreased by $8 for CPT Raxaul to $354/t, while CPT Benapole offers decreased by $3/t to $360/t.

- SAIL-BSP held an auction for 3,900 t of steel-grade pig iron on 16 April in which the entire quantity was booked at an average price of INR 35,400/t exw. In the previous auction, conducted on 13 January for 9,880 t of steel-grade pig iron, the entire volume was booked at an average price of INR 31,600/t exw.

Finished Long Steel

- IF-rebar: India’s induction furnace finished long steel prices decreased w-o-w. Moderate trading activity was witnessed in most regions. Manufacturers lowered their trade offers slightly to encourage sales. However buyers are resisting bulk bookings, waiting for further clarity amid uncertainty surrounding prices. Lifting and dispatches are going on smoothly keeping the inventory levels at approximately 7-8 days. Market participants expect volatility to continue in the near term.

- On a weekly basis, rebar prices fell in the range of INR 100-1,600/t across regions, as per BigMint assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 44,500-45,100/t exw Raipur, and INR 48,700-49,300/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel stands at INR 46,200-46,500/t exw Raipur.

- Trade reference prices of wire rods hovered at INR 45,300-45,700/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices witnessed a decline w-o-w amid slow domestic demand across markets. Buyers adopted a cautious approach and were reluctant to purchase at higher prices.

- Rebar prices (12-32mm) in the trade segment edged down by INR 100/t w-o-w to INR 57,100/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered at INR 56,500-57,500/t FOR Mumbai.

Flat Steel

- Trade-level hot-rolled coil (HRC) offers remained stable w-o-w at INR 51,000-52,700/t ($597-617/t) across markets. Cold-rolled coil (CRC) prices also held steady at INR 56,400-58,500/t ($661-685/t). Softening demand has led to a cautious market sentiment, with participants opting to book profits on existing inventories.

- India’s bulk imports of HRCs and plates touched 93,459 t as of 14 April, based on vessel line-up data from BigMint. Another 82,733 t are expected to arrive this month.

- Indian hot-rolled coil (HRC, SAE1006) export offers to the European Union (EU) remained stable due to subdued demand during the Easter holidays. Offers to the Middle East (ME) were absent amid competitive, declining w-o-w Chinese offers. Indian HRC export offers to Europe held steady, hovering around $630-635/t CFR Antwerp. A transaction of approximately 5,000 t was reportedly concluded at $650/t CFR Antwerp last week.

Leave a Reply