- Slow domestic recovery warrants production cuts

- Focus on net zero compulsions, high quality steels

- Production may fall below 1 bt in by end of 2025

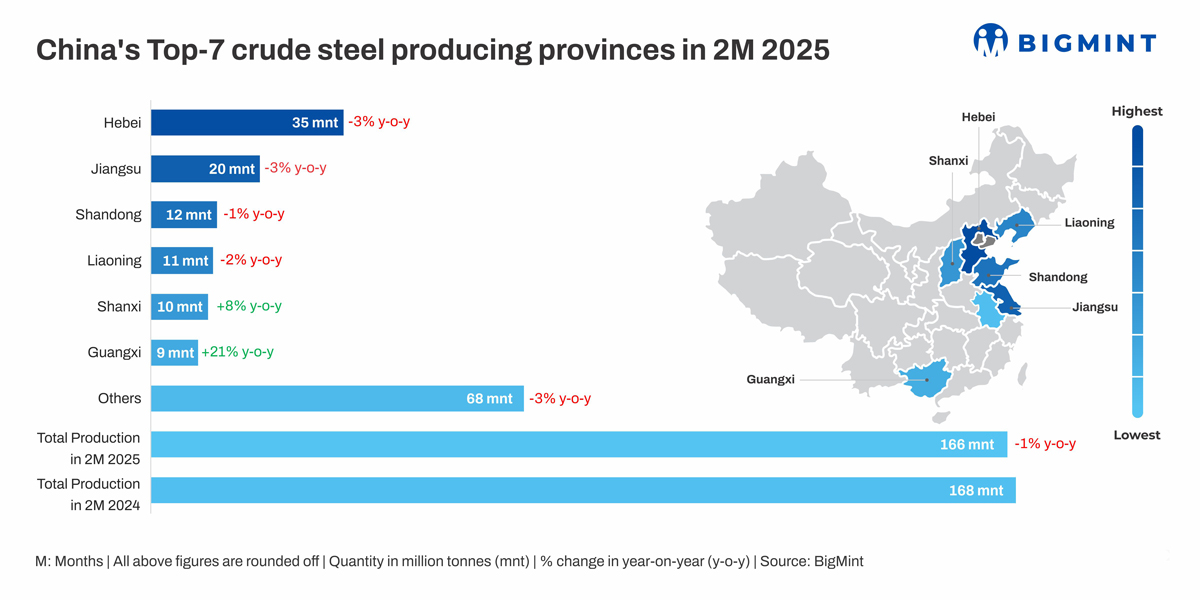

Morning Brief: China’s crude steel production fell a slight 1% y-o-y to 166 million tonnes (mnt) over the first two months of the current calendar of 2025, as per BigMint’s compilations. Volumes had been at 168 mnt in the same two months in 2024.

Province-wise break-up

The top six key crude steel-producing provinces contributed around 60%, at 98 mnt, to the total, flat y-o-y. Four of these showed a y-o-y decline.

Hebei, the largest producer amongst the six, recorded a 3% y-o-y drop to 35 mnt (36 mnt) in this two months.

Jiangsu, the second-largest producer, and housing the largest number of electric arc furnaces, also saw volumes dipping 3% to 20 mnt (21 mnt).

Of the balance four, Shangdong (-1%) and Liaoning (-2%) showed a decline. Shanxi and Guanxi rose 8% and 21% respectively.

It may be noted, for the full year 2024, output dropped 1.70% to 1,005 mnt.

Factors that impacted China’s crude steel production in Jan-Feb’25

Slow home demand recovery: Manufacturing investment growth remained range-bound, hovering in the vicinity of 9% across both months under consideration and this is a slight drop from the 9.2% seen in December 2024 and 9.3% over October-November 2024. The manufacturing industry grew by 6.9% y-o-y, supported by strong gains in high-tech and equipment manufacturing. Growth remains steady, but mounting external pressures, including US trade tariffs and subdued global demand, are beginning to weigh on the country’s manufacturing sector.

Infrastructure investment grew an average 5.3% in the first two months of the calendar. Actually, February’s growth of 5.7% was at an 11-month high since May 2024, reinforcing that the economy improved somewhat with the start of the year. Infrastructure investment expanded by 5.6% y-o-y.

Realty still losing ground but momentum eases: Real estate investment contracted by a further 9.8% provisionally in February 2025 but which was a tad better against a decline of -10.2% in January. However, the decline in newly built commercial building sales showed signs of easing. The floor space of newly built commercial buildings sold decreased 5.1% y-o-y, but this was a 7.8 percentage point improvement compared to 2024. Similarly, total sales value of commercial buildings fell by 2.6%, a significantly narrower decline than the 14.5 percentage point drop recorded in the previous year. Real estate demand is a huge crude steel production influencer since it historically dominated the steel end-user charts.

However, since 2021, its share in steel consumption has been declining. As per some reports, building construction’s steel consumption share fell to 24% in 2023 from 42% in 2010.

Stress on high quality steels: This continued production undercutting denotes the pressures mills are facing in the face of sustained overcapacity amid tardy home demand recovery. China had decided to continue with crude steel output controls and industry restructuring this year to promote development of high-quality steels, as per a draft plan for national economic and social development in 2025, released during the much- anticipated “Two Sessions” meetings — the annual conference of the National People’s Congress and National Committee of Chinese People’s Political Consultative Conference, held last month in Beijing. Although the National Development & Reforms Commission (NDRC) has not specified any production cut targets, speculations are rife on further cuts to rebalance market dynamics.

Focus on net zero: China is focused on meeting its carbon emission goals, which entails cleaning up steel, one of the heaviest contributors to the emission footprint. Recently, the country said, it aims to introduce 200 rules and regulations to calculate the carbon footprint of major industrial products, by 2027. Priority will be given to sectors like steel, non-ferrous metals, construction materials, new energy vehicles etc.

Cumulatively, China has already eliminated outdated capacity in both steel and coal — about 300 mnt/year in the former and 1 billion tonnes/year in the latter. Although no timeframe has been set, China has indicated, paring steel and coal surplus to acceptable levels will take about eight years.

Global protectionism warrants output cuts: In an era of growing protectionism, it is extremely unviable for China to keep nursing its overcapacity especially when domestic demand will take time to recover to a satisfactory level. Several anti-dumping investigations from regions/countries like the European Union, Vietnam, Turkiye and Malaysia are ensuring that Chinese steel exports will taper off in the medium-to-long term as they move in swiftly to protect their domestic mills. Reduced exports in the long term will warrant production cuts.

Outlook

China may continue to see a paring of its overcapacity in the medium to long term keeping its net zero targets in mind. Plus, growing protectionism and a newly-emerging tough tariff regime from the US will also keep the dragon on guard. It will focus more on high margin value-added specialised items rather than run-of-the-mill commercial grades. As per some reports, China’s crude steel production may fell below 1 billion tonne in 2025.

Leave a Reply