Mills raise BF rebar prices, but demand softens

HRC tags fall in most markets, barring south India

IF rebar prices range-bound amid moderate trade activity

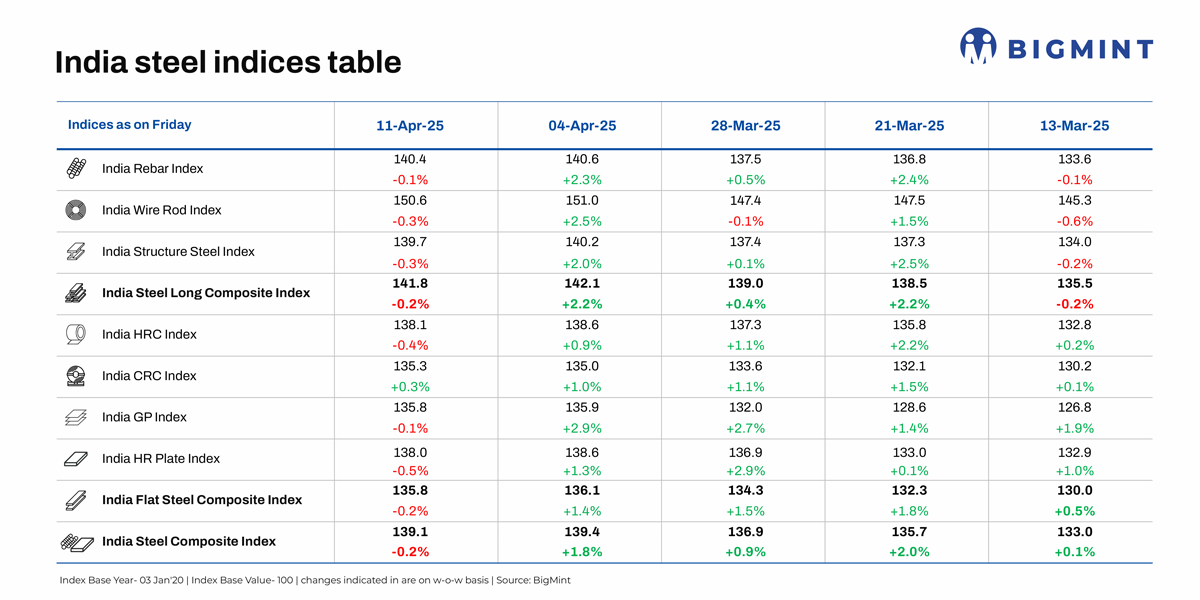

Morning Brief: BigMint’s India Steel Composite Index, a barometer for the domestic market, edged down by 0.2% w-o-w on 11 April 2025, following a steady uptrend lasting six weeks. Buyers largely took a guarded approach to procurement, spooked by the steep price hike recently.

Both the longs and flats indices moved down marginally, by 0.2% w-o-w, and cold-rolled coils (CRCs) were the only segment to witness a rise.

Factors impacting index last week

Mills raise BF rebar list prices: Trade-level blast furnace (BF) rebar prices climbed up w-o-w across key regions, with Mumbai witnessing a marginal rise of INR 200/tonne (t) ($2/t) w-o-w to INR 57,200/t ($664/t) exy, exclusive of GST at 18%.

This followed a price hike announced by some private steel mills, by up to INR 1,500/t ($17/t). Revised list prices were at INR 57,000-58,500/t ($662-679/t) on landed basis, BigMint learnt.

However, demand-wise, the market was subdued. Trade was conducted largely to fulfil immediate needs, but material shortages and range-bound raw material prices kept rebar tags supported.

Demand from the projects segment also moderated this week. Prices were at around INR 56,500-57,500/t ($656-668/t) FOR Mumbai.

Moderate buying keeps IF rebar tags range-bound: In the trade segment, prices of induction furnace (IF) rebars were range-bound w-o-w, with moderate buying activity exerting downward pressure.

BigMint assessed IF rebar prices at INR 49,400/t ($574/t) exw-Mumbai, down by INR 200/t ($2/t) w-o-w.

However, the sluggish trade momentum did not pose too much of an inconvenience. Inventory pressure was not significant, with (1) mills having received substantial orders last month and (2) idling time standing at an average of 7-8 days.

Limited demand pulls down HRC prices in most markets: Trade-level hot-rolled coil (HRC) offers declined w-o-w in most markets. However, prices moved up in south India.

In Mumbai, the benchmark market for BigMint’s assessment, HRC prices (IS2062, Gr E250, 2.5-8 mm/CTL) fell by INR 550/t ($6/t) w-o-w to INR 51,800/t ($602/t), pressured by limited demand and need-based procurement. Buyers resisted higher prices, and deals were concluded mostly for low-priced material.

Additionally, the escalating global tariff conflict and uncertainty around the implementation of safeguard duty kept buyers wary. Suppliers also prioritised the offtake of inventory, with most offering discounts or reducing offers to sell off material and secure profits.

Previously, a few months back, when the market was on a steady downtrend, some suppliers had decided to limit the material available for sale, hoping to gain better margins. Following the recent price hikes, these suppliers have decided to offload stocks, after conceding to buyers’ calls for a price cut.

On the other hand, in south India – specifically, Bangalore, Chennai, and Hyderabad – prices rose by INR 700-1,700/t ($8-20/t), boosted by supply shortage. Notably, lower-priced material, be it domestic or imported products, were not available at all, which gave sellers grounds to keep offers high.

HRC export activity remains sluggish: India’s HRC export activity remained subdued amid lukewarm demand.

Offers (SAE 1006) to the Middle East were muted following Eid, amid cautious buyer sentiment due to tariff-driven uncertainties. For a few weeks now, Indian mills have stopped actively offering to this region, given reduced activity during Eid.

Meanwhile, export offers to the EU were firm w-o-w at $630-635/t CFR Antwerp, with Indian suppliers having their safeguard quotas tightened from this month. Additionally, domestic HRC prices rose, buoyed by safeguards and anti-dumping duties, though demand remained weak.

Outlook

The optimism from the safeguard duty announcement has fizzled out, and the market is now back to being shaped by the fundamental forces of demand and supply. As such, prices are expected to remain range-bound in the short term, given that end-user demand continues to be slack.

There are concerns that the rise in prices has far outstripped the pick-up in demand. As a result, prices may also face corrections. However, the rumoured supply shortages may help suppliers defend higher offers.

Overall, bearish sentiment prevails. Heightening trade tensions and uncertainties, spurred by Trump’s announcement of reciprocal tariffs and swift rollback of them, are expected to adversely impact India. The downtrend in steel imports may reverse, a possibility that the ministry seems to be carefully evaluating. Sources suggest that the quantum of the safeguard duty may be increased to 20%, to further fortify the domestic industry.

Leave a Reply