- Indonesia top exporter but volumes edge down

- Domestic coal production up 5% y-o-y in FY’25

- Coal imports in Mar’25 climb to a 10-month high

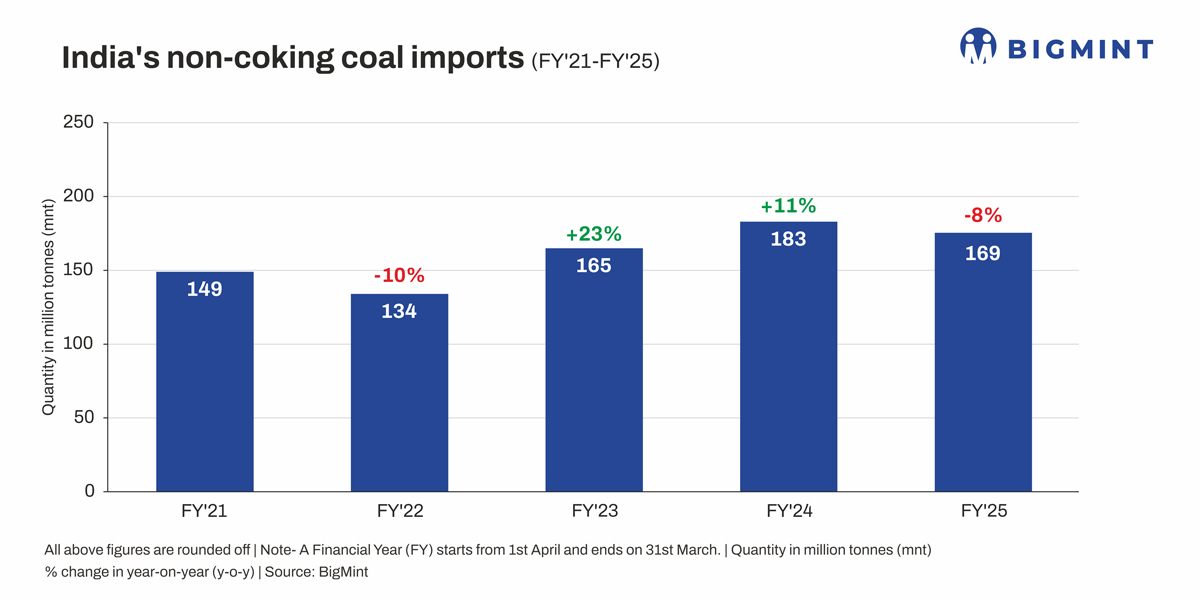

Morning Brief: India’s imports of non-coking coal, used for power production and in other industrial sectors, dwindled by 8% y-o-y in financial year 2024-2025 (FY’25) to around 169 million tonnes (mnt) compared with 183 mnt in the preceding fiscal, as per latest BigMint data.

Imports of mainly low-ash and high-calorific non-coking coal decreased amid higher domestic production and availability. Imports dropped y-o-y for the first time since the pandemic period.

Country-wise imports

Indonesia remained the top coal exporter to India, shipping over 104 mnt in FY’25, a decrease of over 6% y-o-y. Weather disruptions and logistical bottlenecks weighed on imports from Indonesia, but demand was certainly weaker than in FY’24.

In comparison, India’s coal imports from South Africa increased by 13% y-o-y to over 33 mnt in FY’25 from around 29 mnt due largely to higher demand from the domestic steel sector.

Imports from other key suppliers – mainly the US and Russia – also declined y-o-y.

How India reduced its import dependency in FY’25?

Record domestic production: According to data from the Ministry of Coal, India’s coal production reached 1,047.57 mnt (provisional) in FY’25, compared to 997.83 mnt in FY’24, marking a 4.99% growth. BigMint data show that Coal India Ltd., the largest coal miner in the world, saw production increasing marginally – by 1% y-o-y – in FY’25 to over 781 mnt. Among CIL’s subsidiaries, MCL raised production by around 10% y-o-y, while SECL witnessed a decline in output.

Production from commercial and captive mines also saw a remarkable surge, reaching 197.5 mnt (provisional) – a 28.11% increase from 154.16 mnt recorded in the previous year, as per government data. Increased domestic production and dispatches reduced the need for imports.

Drop in share of imported coal for blending: Ministry data reveal that imports for blending by thermal power plants dropped 29.8% in FY’25, despite a 3.53% rise in coal-based power generation. Notably, the government’s mandate on imported coal blending for power plants ended in February and has not been renewed since. The mandate has been revised several times since 2020.

Higher stocks at power plants: Coal stocks at thermal power plants decreased slightly to a tad below 58 mnt as on 9 April, as per assessment, which is sufficient to meet 20 days’ requirement. Of the over 180 domestic coal-based thermal power plants in India only 10 were assessed having critical stock levels. Therefore, imports could be avoided to a large degree.

More volumes on offer at CIL auctions: Volumes offered at auctions by CIL subsidiaries registered a notable growth y-o-y in FY’25. Notably, coal imports by the non-regulated sector (NRS) dropped 12% y-o-y, signaling higher availability at auctions.

CIL reduced the Earnest Money Deposit (EMD) for its e-auctions from INR 500/t to INR 150/t last year. E-auction premiums have dropped significantly from 252% in FY’23 to 29% in FY’25. By lowering entry barriers, CIL seeks to stimulate bidding activity and cater to a larger segment of buyers.

Increased sponge iron production: India’s crude steel production increased by 4.7% y-o-y in FY’25 and BigMint data show that sponge iron production rose by 5% to over 54 mnt. Over 80% of India’s sponge iron production is through the coal-based route and imported South African coal is preferred by producers for its higher fixed carbon content.

Higher generation from renewable sources: Data show that although thermal generation has a share of around 75% of India’s power mix, renewable energy growth has been phenomenal. In FY’25, generation from solar, wind, biomass and other renewable sources increased over 13% y-o-y to 232 billion units, while large hydropower generation edged up by 10% y-o-y. India’s installed renewable energy capacity, excluding large hydro, was assessed at over 220 GW as of 31 March, 2025.

Outlook

As per BigMint data, non-coking coal imports in March rose to a 10-month high of over 15 mnt from less than 12 mnt in February. The IMD has predicted heatwaves in vast swaths of the country this summer, and the mercury seems to have already touched unbearable levels in late-March and early-April. The drawdown of stocks at coal plants has naturally accelerated resulting in a slight decline in coal stocks.

The Short-Term National Resource Adequacy Plan (ST-NRAP) released by the National Load Despatch Centre projects India’s peak power demand to reach 273 GW in June compared to 250 GW in 2024. Therefore, coal imports in Q1FY’26 will obviously pick due to seasonal factors and especially to meet the surge in demand for cooling.

So, it remains to be seen how successfully the government manages to keep coal imports in check in the current fiscal through higher production, dispatches and development of logistics.

On the supply side, Indonesian coal exports may decline going forward, with the government in that country seeking to streamline export prices by adopting the HBA index for coal exports. BigMint notes that this may erode Indonesia’s unique price competitiveness in the global coal market and result in decreased shipments, especially to India and China.

Leave a Reply