- Deep-sea Imported market quiet with delays in fresh bookings

- Mills shift focus to billet amid weak demand

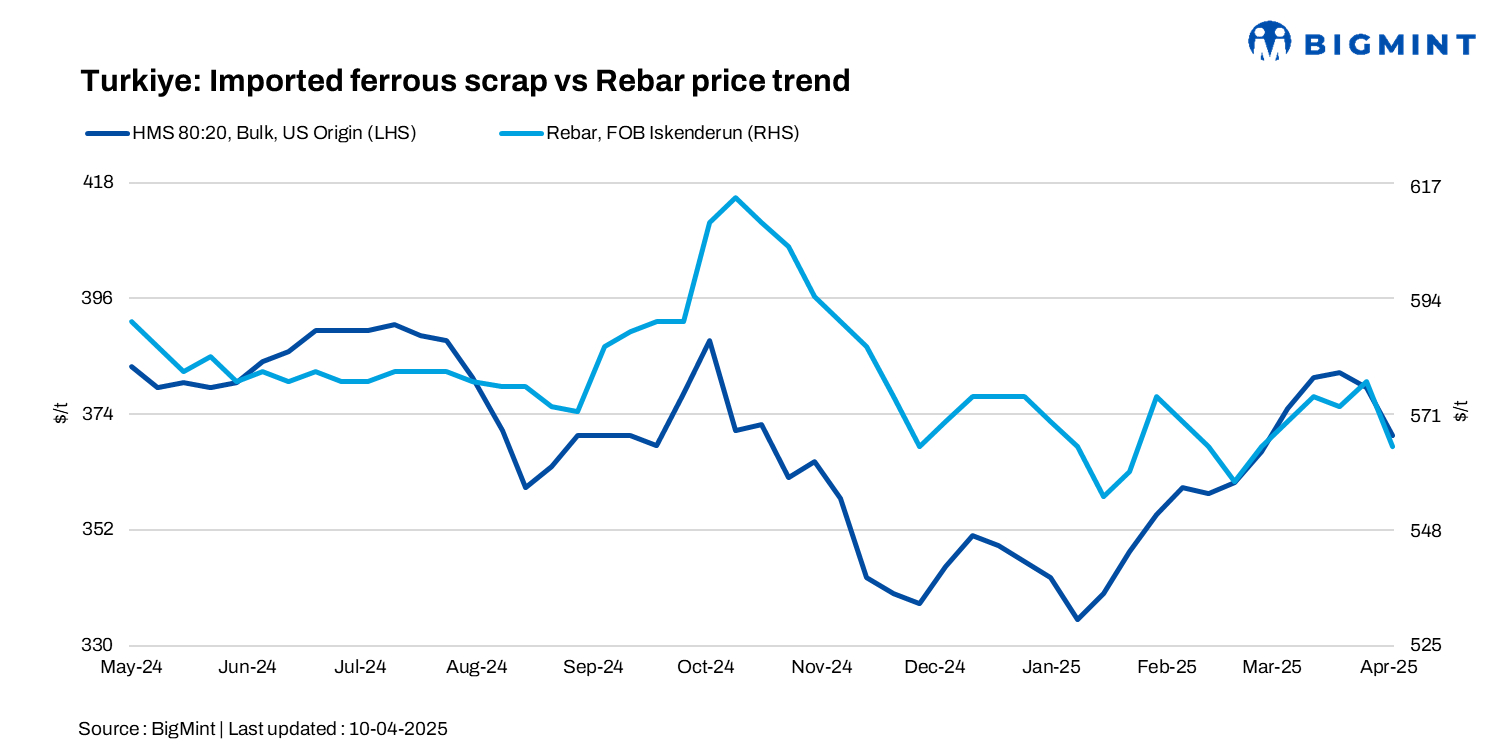

The Turkish deep-sea imported scrap prices declined by $8-10/t w-o-w, with the market continuing its quiet stance and showing little sign of recovery. Both buyers and sellers stayed cautious, avoiding new deals amid ongoing uncertainty.

Turkish mills faced sluggish demand for finished steel both domestically and abroad, limiting their ability to raise prices or offset rising energy costs. With weak buying interest, mills held back from deep-sea scrap purchases and considered production cuts, while exporters remained largely inactive. To maintain inventory, some mills turned to short-sea scrap and billet imports from the Far East as more cost-effective alternatives.

Chinese billet was offered at $465-470/t CFR, while Turkish buyers were bidding closer to $457/t CFR. Malaysia-origin billets are offered at up to $490/t CFR. However, no import deals have been reported due to continued weakness in the rebar market.

HMS collection prices in the Benelux region were reported at Euro 290-300/t delivered to docks.

However, the strength of the euro was making it difficult for European suppliers to adjust their export offers to Turkiye downward.

According to market insiders, reported indicative offers for US and Baltic regions for HMS 80:20 quoted below $375/t CFR. Meanwhile, tradable values for EU-origin HMS 80:20 were mostly at $365-370/t CFR.

BigMint’s price assessments

- US-origin HMS 80:20 bulk scrap stood at $370/t CFR Turkiye, down $9/t w-o-w.

- Bulk HMS 80:20 from the US East Coast was at $354/t FOB, down $2/t w-o-w.

The Turkish scrap-to-rebar spread widened w-o-w to $190-195/t as rebar export prices inched down w-o-w to $560-565/t FOB.

Market comments

As per a US-origin scrap supplier, “Last week saw 1-2 bulk vessels getting booked, and now there are about 15-20 offers circulating in the market. Mill inventories are running quite low, so we expect a buying spree to kick off soon. That kind of urgency usually keeps prices from sliding–at least for this week.”

“It’s quite difficult to pin down a market price right now with so much uncertainty globally. It could very well be around $373-375/t as suggested, but it might just as easily fall to $360-365/t at this point, it’s more of a guessing game. Let’s see how the second half of the week unfolds; more deals should emerge, and that’ll show us how scrap recyclers are truly reacting.” — As per a European scrap supplier

A market participant noted, “Despite ample scrap availability for May shipment, sellers held firm and did not reduce their offers.”

Another market participant said that “sluggish activity continued, as Turkish mills postponed restocking for May shipments due to persistently weak rebar demand.” Mills are choosing to wait, and suppliers aren’t making any effort to push offers either.”

Domestic market

In the domestic market, rebar production remains unprofitable at current offer levels, with workable prices seen at $555-565/t exw. Buyers are securing only small volumes to meet immediate needs.

Kardemir returned to Turkiye billet market this week with stable pricing and managed to sell moderate volumes. However, overall demand remained limited as the rebar market continued to show little improvement.

Outlook

Recent energy price hikes in Turkiye–10% for electricity and 20% for industrial gas–have added an estimated $5-7/t to rebar production costs, pressuring mills to recover margins. While some mills are interested in buying scrap, weak finished steel demand is keeping them cautious. Scrap prices may see a slight decline in the near term.

Leave a Reply