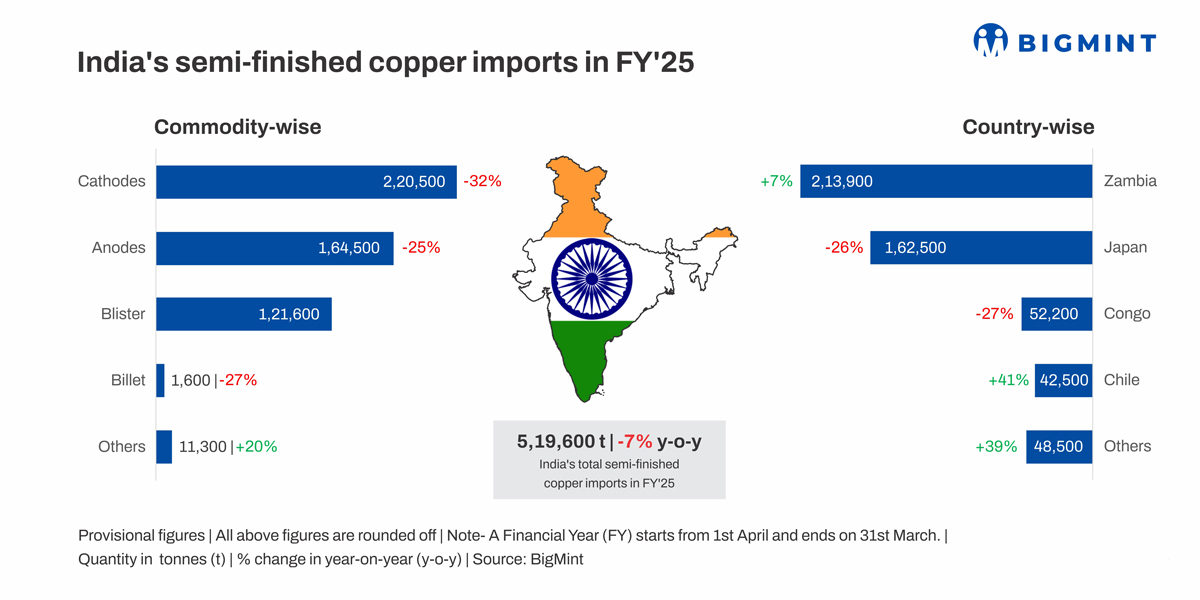

- Semi-finished copper imports down 7% y-o-y

- Imports of finished copper edge up by 20%, scrap up 10%

- Copper concentrate imports rise on higher demand from smelters

This was driven primarily by a 32% fall in cathode and 25% decline in anode imports as buyers turned to blister copper, an intermediate product, which witnessed an astounding surge in demand with total imports rising to 121,601 t in FY’25.

This change in the pattern of imports signals a broader shift in strategy adopted by Indian smelters and manufacturers – importing upstream inputs like blister instead of finished or semi-finished copper, allowing them to refine and add value domestically. Produced during the extraction of copper, blister has to undergo further refining through an electrolytic process.

India scrapped import duties on blister copper in early 2025, making it an even more attractive alternative for downstream producers. With blister now serving as a feedstock to produce cathodes and anodes locally, the need for direct imports of these refined products has declined.

Imports of finished copper up 20%

While semi-finished copper imports dipped, finished copper import shipments increased by 19.56% y-o-y in FY’25, rising to 657,414 t from 549,857 t in FY’24.

Imports of finished flats rose by 27.17% y-o-y to 164,574 t, while finished longs stood at 164,133 t, up 12.79% y-o-y.

This growth in imports of finished products was largely driven by strong demand in the building construction, consumer goods, automobiles, power, and renewable energy and transportation sectors. Constrained domestic availability of semi-finished products arose from demand outstripping supply which led to higher imports of finished material.

Policy support drives scrap imports

India’s copper scrap imports also rose by 10.1% y-o-y, reaching 335,218 t in FY’25 from 304,583 t in the preceding fiscal. With zero import duties, and faster processing timelines, scrap has become a viable feedstock for many producers hit by high prices of refined inputs.

With large smelting capacities being set up in India, many producers are securing more scrap as a feedstock for recycling/refining. Importing scrap is often cheaper and quicker than importing refined products. In early 2025, the Indian government scrapped import duties on copper scrap, making it more attractive for buyers.

With large smelting capacities being set up in India, many producers are securing more scrap as a feedstock for recycling/refining. Importing scrap is often cheaper and quicker than importing refined products. In early 2025, the Indian government scrapped import duties on copper scrap, making it more attractive for buyers.

Domestic cathode production rises

The reduced reliance on imported cathodes also aligns with a 9.8% increase in domestic cathode production, reaching 560,000 t in FY’25, driven by better plant utilisation and capacity additions.

Copper concentrate imports rose 18.8% y-o-y to 1.19 million tonnes (mnt) in FY’25, reflecting increased smelting activity to support the shift toward raw materials.

India’s copper consumption stood at over 1.7 mnt in FY’24 and BigMint data show that refined copper production is around 555,000 t per year against domestic consumption of more than 750,000 t. Hence, imports have to meet the shortfall.

Outlook: Cathode imports to remain under pressure

With large new capacities such as Adani’s 0.5 mnt Kutch Copper project coming online, cathode imports could decline further as domestic supply improves. Adani and JSW have secured long-term concentrate deals with miners in Australia, Chile, and Peru, strengthening India’s upstream value chain.

Leave a Reply