- Indian buyers resist firm offers

- Turkish mills pause on energy hike

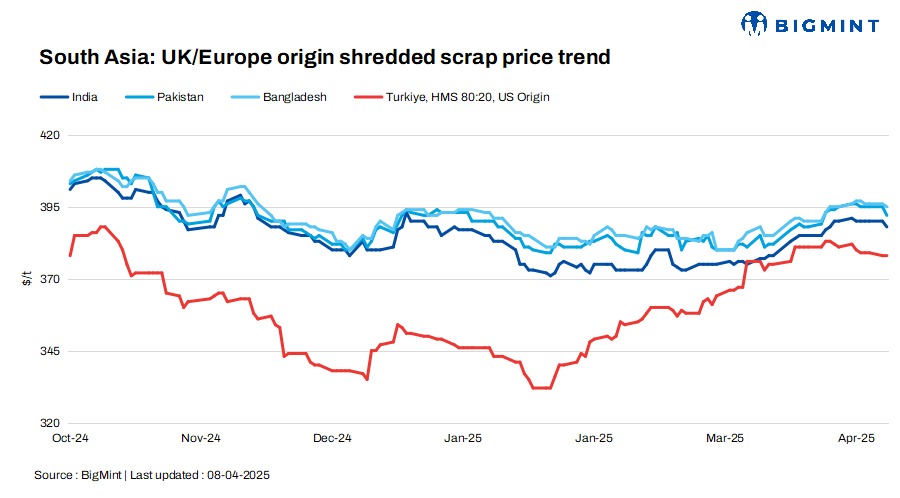

South Asia’s imported scrap markets remained cautious and quiet today, as buyers remained largely inactive due to a mix of factors such as global uncertainties, high offer levels, and domestic challenges. In India, improved steel sentiments were overshadowed by bid-offer gaps and cheaper sponge iron as an alternative.

Pakistan’s market stayed sluggish post-Eid, with limited activity amid weak demand and security concerns. Bangladesh continued to grapple with LC issues, dampening trade despite competitive offers.

Meanwhile, Turkiye saw a slight dip in scrap prices as mills paused amid rising energy costs and slow rebar demand.

UK-origin shredded scrap offers edged down by $2/t in India, while $3/t in Pakistan and $1/t in Bangladesh. However, bulk offers for HMS 80:20 from the US to Turkiye remained unchanged d-o-d.

Overview

India: India’s imported scrap market remained rangebound, with buyers largely inactive due to bid-offer mismatches and expectations of prices softening despite improved domestic steel sentiments. Shredded scrap offers stood at $390-395/t CFR Nhava Sheva, but buyers stuck to $5-7/t below that level, keeping trades limited.

Strong seasonal demand kept finished steel prices firm, while domestic sponge iron remained cheaper, pressuring scrap buying. The stronger euro and positive domestic cues supported seller confidence. However, buyers stayed cautious, awaiting clearer market direction amid mixed signals from local and global markets.

Pakistan: Pakistan’s imported scrap market remained sluggish, with limited activity as buyers resisted high offer levels amid weak domestic demand and post-Eid business inertia. Shredded scrap offers from the UK/EU hovered around $390-395/t CFR Qasim, while UAE-origin materials ranged between $385-400/t, holding firm due to global uncertainty. Domestic sentiment remained muted, influenced by security concerns in Balochistan and a delayed return to full business operations.

Local scrap prices stood at PKR 135,000-140,000/t ($487-505/t), billets at PKR 200,000-205,000/t ($722-740/t), and rebars at PKR 235,000-240,000/t ($848-866/t). Prices may rise to PKR 145,000-148,000/t ($524-535/t) due to tight supply, but not immediately, as the market remains slow.

Bangladesh: Bangladeshi buyers showed limited interest in fresh scrap bookings as caution prevailed and persistent LC issues continued to disrupt trading activity. Offers for UK-origin shredded scrap to Chattogram were heard at $380/t CFR, while UK HMS 80:20 remained unconfirmed. Australian HMS 80:20 was offered at $365/t CFR, and Hong Kong PNS was quoted higher at $392/t CFR. Despite available offers, trading remained muted amid financial constraints and subdued buying appetite.

Turkiye: The Turkish imported scrap market saw a slight dip as mills remained cautious amid rising energy costs and weak rebar demand. Offers for US-origin bulk HMS 80:20 were assessed at $378/t CFR, but trade remained limited as mills paused restocking. A 10% hike in electricity and 20% rise in industrial gas prices added pressure on mill margins, increasing expectations for further price reductions. While mills stayed in wait-and-watch mode, some market participants anticipate a return for May bookings. Meanwhile, the steepening backwardation in the scrap futures curve reflects expectations of continued price softness ahead.

Price assessments

India: UK-origin shredded indicatives were assessed at $388/t CFR Nhava Sheva, down by $2/t d-o-d.

Pakistan: UK-origin shredded indicatives edged down by $3/t d-o-d to $392/t CFR Qasim.

Bangladesh: UK-origin shredded indicatives stood at $395/t CFR Chattogram, down by $1/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were stable at $378/t CFR Turkiye compared to the yesterday.

Leave a Reply