- ME overtakes Vietnam as leading importing region

- Steel exports to India drop considerable 39% y-o-y

- Protectionism, carbon concerns may cap future volumes

Morning Brief: China continued its exports onslaught into the new calendar of 2025 despite several governments across the globe adopting protectionist stances.

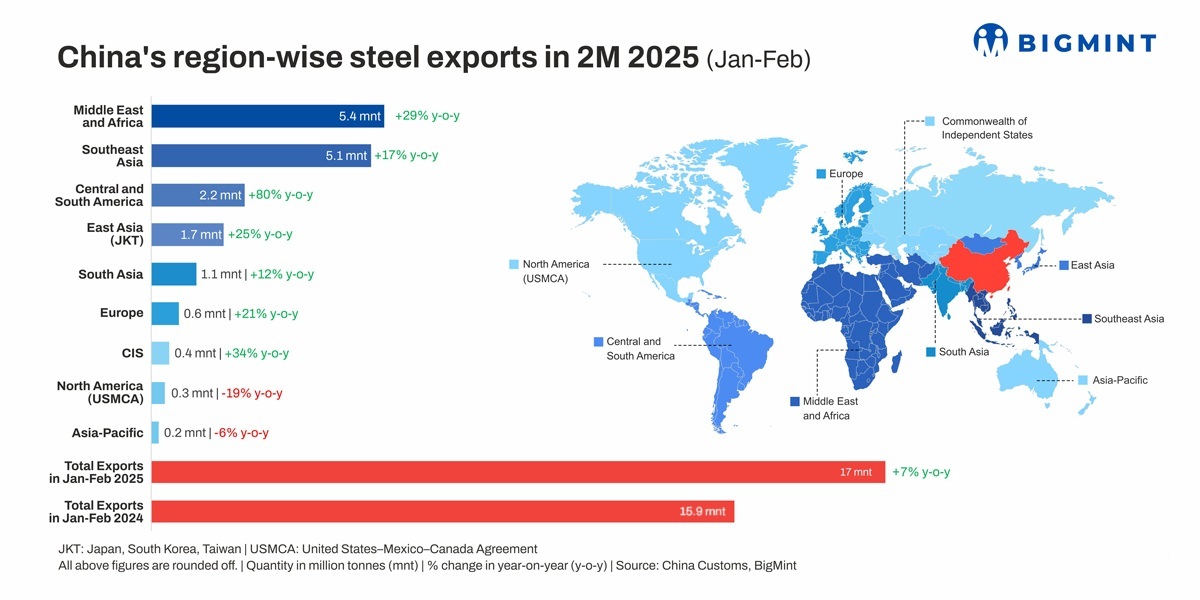

Steel exports in the first two months of the current calendar (January-February, 2025) totalled 17 million tonnes (mnt), a healthy 7% increase over 15.9 mnt recorded in the same two months in 2024, as per China Customs data, compiled by BigMint.

Middle East & Africa overtook Southeast Asia as the No.1 importing region with a 29% y-o-y increase in volumes to 5.4 mnt (4.2 mnt) over January-February, 2025. All the countries here, except for Turkiye, recorded a positive growth in this period under review. Turkiye has been experiencing dampened domestic and export demand. The UAE led with a handsome 0.90 mnt (0.74 mnt).

SE Asia was a close second with 5.09 mnt (4.34 mnt), a y-o-y increase of 17%. Vietnam, China’s leading importer, saw a 16% drop in volumes to 1.56 mnt (1.86 mnt) in the run-up to and imposition of provisional anti-dumping duties on the dragon country.

Chinese steel exports to East Asia saw a 25% y-o-y growth in January-February 2025 to 1.69 mnt (1.35 mnt).

South Asia witnessed a modest 12% increase to 1.05 mnt (0.94 mnt). Volumes to India actually fell 39% y-o-y to 0.27 mnt (0.44 mnt) in these first two months of 2025.

Amid concerns over tariff impositions, exports to North America saw a 19% decline y-o-y to 0.33 mnt (0.41 mnt).

Factors sustaining high Chinese steel exports

Domestic demand improves but still a long way to go: Domestic steel demand is still slow although it is better than before. Manufacturing investment growth remained range-bound, hovering in the vicinity of 9% across both months under consideration and this is a slight drop from the 9.2% seen in December 2024 and 9.3% over October-November 2024.

Infrastructure investment grew an average 5.3% in the first two months of the calendar. Actually, February’s growth of 5.7% was at an 11-month highest since May 2024, reinforcing that the economy improved somewhat with the start of the year.

Real estate investment contracted by a further 9.8% provisionally in February 2025 but which was a tad better against a decline of -10.2% in January.

But, many say, end-user demand recovery is still slow despite some booster shots injected periodically in the last one year.

This scenario is still forcing mills to sustain the exports upswing.

Domestic price squeeze forces exports: China’s steel prices faced downward pressures during February due to the widespread bearish sentiment among market players. In fact, domestic prices have been another key reason that has forced mills to thrive on exports.

For instance, data reveals that Tangshan HRC prices were down 15% over January-February 2025 at an average RMB 3,484/t ($479/t) against RMB 4,108/t ($565/t) in January-February, 2024. Similarly, rebar fell 21% to RMB 3,230/t ($444/t) in the first two months of 2025 against RMB 3,881/t ($534/t) in this period in 2024. Faced with the double whammy of low sales volumes and squeezed margins, exports seem a more lucrative option.

Predatory pricing gives China edge over competitors: Chinese mills, to ensure that they had an edge over other exporting countries, in a calculated move, kept their prices lower in comparison. This ensured that markets remained enticed by this predatory pricing.

Average export offers for benchmark hot rolled coils averaged $471/t FOB over January-February 2025, whereas Japan’s were at $477/t FOB and India’s, at $505/t FOB. The rock-bottom offers allowed the Chinese to play in volumes.

Outlook

Rising trade barriers and sustained capacity down-sizing may eventually see China’s steel exports falling back.

Anti-dumping actions against Chinese steel are becoming more frequent in international markets, with the US, India, South Korea, and Vietnam all announcing plans to impose additional tariffs on steel imports from China.

Plus, China is cutting down on production with an eye on net zero and a greener economy. Crude steel production over January-February, 2025 showed a 1.50% y-o-y decline to 166.30 mnt. For the full year 2024, output dropped 1.70% to 1,005 mnt.

If domestic demand improves with subsequent policy support, then possibly mills would focus more on feeding home demand.

Leave a Reply