- Indian SS market fails to gain momentum

- LME nickel prices dip 1% w-o-w

Prices of Indian stainless steel (SS) finished products remained stable w-o-w, amid sluggish market activity. Market has remained less active due to Eid and FY closing.

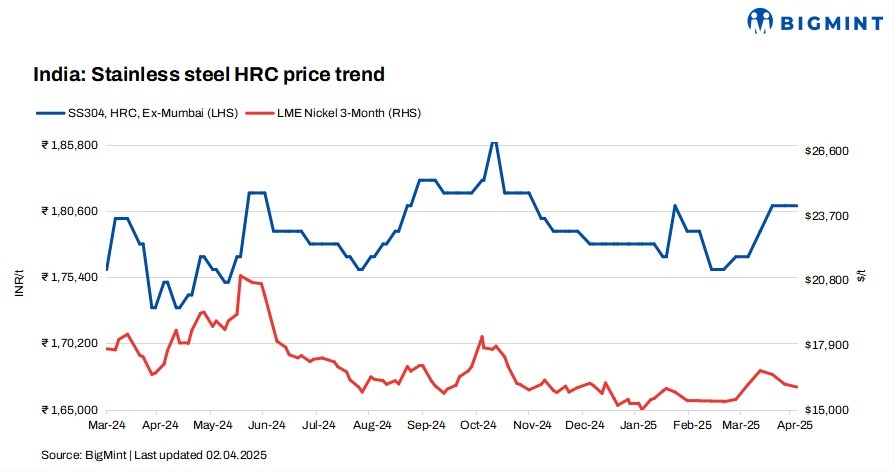

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 181,000/tonne (t), steady w-o-w, while 304L (25-100 mm) black round bars also remained stable at INR 160,500/t, both ex-Mumbai.

LME nickel tags drop, Asian NPI rises

At the time of reporting, three-month LME nickel prices stood at $16,005/t, reflecting a marginal dip of 1% from last week’s $16,170/t. Nickel stocks in LME-registered warehouses remained largely stable at 199,020 t compared to 201,330 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) witnessed an increase of RMB 5/metric tonne unit (mtu) ($0.5/mtu) w-o-w to RMB 1,030/mtu ($141/mtu). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $123/mtu, up by $1/mtu w-o-w.

Finished market remains steady w-o-w

As per BigMint’s assessment, SS 316 HRCs remained stable w-o-w at INR 325,000-327,000/t ex-Mumbai.

According to a market participant, “The stainless steel market has seen a slowdown in recent days, primarily influenced by the Ramadan and the financial year-end. These events have caused a temporary pause in local trading activities, resulting in limited market movement. As a result, market participants are holding back, waiting for a resumption of normal trading activity once the holidays conclude.”

Demand in the longs segment has been sluggish in recent months, but a positive market movement is expected in the coming weeks.

BigMint’s assessment of SS 316L (25-100 mm) black round bars stood at INR 270,000-272,000/t ex-Mumbai, unchanged w-o-w. Prices of SS 316L (25-100 mm) bright bars stood at INR 288,000-290,000/t ex-Mumbai, steady w-o-w.

Additionally, sources indicated that payments from buyers are still pending, and mills have yet to fully close their books for FY25. This has created liquidity pressures, contributing to a downturn in the market.

Chinese stainless steel prices drop

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 14,150/t ($1,944/t) exw, down by RMB 100/t ($13/t) w-o-w, while FOB prices of 304-grade CRCs were at $1,910/t.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices moved down slightly by INR 13,000/t ($152/t) as compared to the previous assessment on 26 March. Minimal price movements were observed in global markets.

Ferro molybdenum prices in India were at INR 2,559,000/t ($29,935/t) exw-India, as per BigMint’s assessment on 2 April. Approximately, 25 t of trades were heard last week within the price range of INR 2,545,000-2,580,000/t ($29,771-30,180/t) exw.

As per BigMint’s assessment on 2 April, ferro molybdenum prices in India were at INR 2,559,000/t ($29,945/t) exw on a 60% pro rata basis.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,100/t ($1,171/t) exw-Jajpur, down by INR 400/t w-o-w amid limited market movements.

Outlook

In the short term, market activity is expected to stay moderate, with hopes that the start of the new fiscal year will bring some improvement in demand as well as the prices.

Leave a Reply