- Indian buying limited on bid-offer mismatches

- Turkish scrap pressured by weak rebar demand

South Asia’s imported scrap market remained largely subdued as buyers in India, Pakistan, and Bangladesh navigated post-holiday lulls, financial closures, and liquidity constraints.

Indian buyers showed limited interest due to bid-offer mismatches, while Pakistan’s market stayed quiet due to the observance of Eid, with mills operating at reduced capacity. In Bangladesh, restricted LC approvals kept trade activity low.

Meanwhile, Turkiye’s scrap market faced downward pressure amid weak rebar demand, with sellers anticipating stronger May shipments despite global uncertainties.

Overview

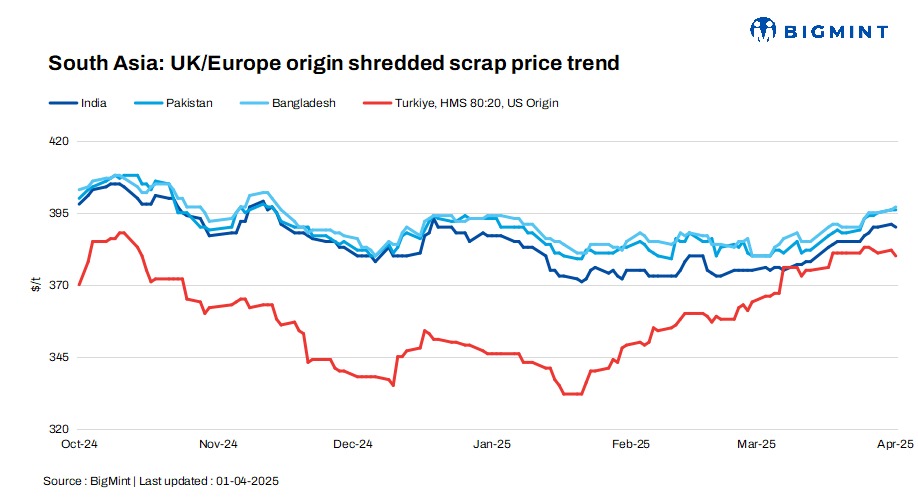

India: Indian buyers showed moderate interest in imported scrap due to a bid-offer mismatch, while market activity remained subdued as buyers focused on financial year-end closures and awaited clearer price trends. Shredded scrap offers from the UK/Europe were at $390-395/t CFR Nhava Sheva, with buyer bids at around $385-390/t CFR. Meanwhile, HMS 80:20 offers from the UK/Europe and West Africa ranged between $365-375/t CFR.

In the domestic market, BigMint’s Mandi Gobindgarh’s domestic end-cutting scrap index held steady at INR 38,300/t DAP on 1 April 2025, with stable semi-finished and scrap prices amid moderate finished steel demand. Mills remained optimistic as scrap arrivals improved, keeping production levels high. Sponge iron and pig iron prices saw slight increases, while steel ingots stayed flat. Rebar and HR strip prices edged up on moderate buying. In Alang, ship-breaking scrap prices rose by INR 300/t, driven by strong demand from induction furnaces.

Pakistan: Pakistan’s imported scrap market remained muted as buyers stayed on the sidelines ahead of Eid, awaiting clarity on post-holiday trends. UK/EU-origin shredded offers stood at $395-400/t CFR Qasim, though potential buying interest was closer to $390-395/t. UAE-origin shredded remained slightly higher at $400-405/t but saw limited interest.

Domestically, scrap hovered at PKR 140,000-145,000/t, while rebar and billets were at PKR 244,000-245,000/t and PKR 208,000-210,000/t, respectively.

Mills operated at reduced capacity due to liquidity constraints and LC issues, keeping trading activity sluggish. While market participation is expected to resume mid-week, elevated global scrap prices and economic uncertainty could limit a sharp rebound.

Bangladesh: Bangladesh’s imported scrap market stayed quiet as buyers have yet to resume normal operations post-Eid holidays. Limited LC approvals ahead of Eid further constrained trade, keeping domestic scrap prices stable.

Turkiye: The Turkish imported scrap market started the week with prices edging lower as buyers stayed on the sidelines amid the Eid holidays. Low rebar demand kept mills cautious, limiting scrap purchases. While sellers expected firm demand for May shipments, US recyclers remained bullish, unwilling to lower prices despite potential domestic softness.

European recyclers also saw steady demand for May cargoes, with tradable values hovering at $375-383/t CFR.

Political uncertainties in Turkiye encouraged sellers to close deals early, while market participants awaited the US Section 232 tariff announcement for potential market impact.

Price assessments

India: UK-origin shredded indicatives were assessed at $390/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives remained unchanged at $396/t CFR Qasim.

Bangladesh: UK-origin shredded indicatives edged up by $1/t d-o-d to $397/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $380/t CFR Turkiye, down by $2/t d-o-d

Leave a Reply