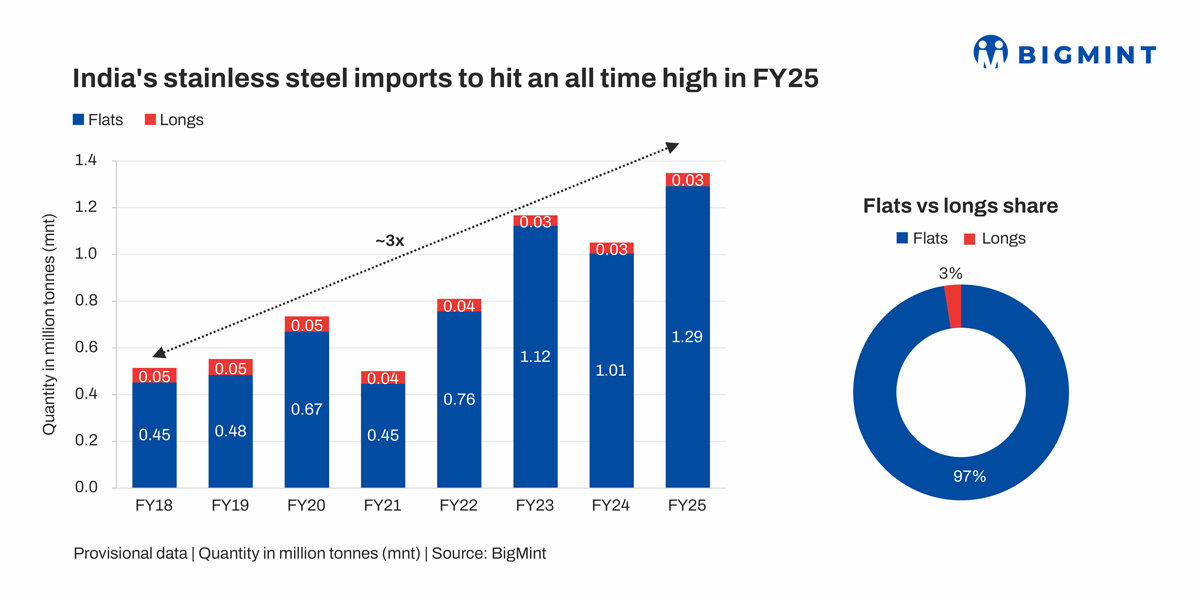

- Imports increase threefold in 8 years since FY’18

- Total inbound shipments rise 28% y-o-y in FY’25

- Liberal trade policy driving imports, especially from Asian countries

Morning Brief: India’s imports of finished products of stainless steel are projected to tough a new high of 1.3 million tonnes (mnt) in FY’25, climbing to the highest level in the last eight years since FY’18 when imports stood at just 0.5 mnt, as per provisional and historical data maintained with BigMint.

This reflects a nearly a threefold increase in finished stainless steel imports between FY’18 and FY’25 — a surge of 166% in eight years!

In FY’25, finished stainless steel imports are expected to grow by 28% y-o-y from 1.03 mnt in FY’24.

Product-wise imports

Out of total import shipments, finished flat products are projected to be around 1.29 mnt, or over 97% of total imports, while finished long products may account for 0.03 mnt.

300-series austenitic stainless steel imports have a share of roughly 52% of total imports and reflect the sharpest growth y-o-y. In the flats segment, imports of 300- and 400-series formed the bulk of shipments, and both in the flats and longs segments, imports of 300-series stainless steels showed sharp yearly growth.

The country-wise breakdown shows that China continues to be a major supplier of stainless steel, with a share of over 45% in FY’25, although its share is expected to dip by 10% y-o-y to settle at 598,548 t.

Indonesia was the other major supplier, shipping over 312,000 t to India. The country’s production capacity has seen rapid growth in recent years, thanks to large-scale Chinese investments. Indonesia has been the sole supplier of SS 300-series semi-finish slabs and the entire volume went to a single player in India.

Imports from Japan are projected to rise by 34%. Japan is seeing a decline in domestic consumption amid a lull in its construction sector amid labour shortages and rising material costs. Machinery and engineering exports have declined and Japan’s auto production decelerated after the safety test scandal at Toyota’s small car unit, supporting the case for increased exports.

Factors driving SS imports

FTAs, trade policy facilitating higher imports: Volumes from Indonesia, Japan and Vietnam are expected rise in FY’25. India has free trade agreements (FTAs) with Indonesia and Japan, and thus these countries do not have to shell out customs/import duties. Notably, around 40% of stainless steel imports are landing from FTA countries at nil duty. The effective BCD currently stands at 7.5% while the import tariff if 15%.

Again, India rolled back countervailing duties on stainless steel hot-rolled and cold-rolled flat products from China in the General Budget for CY’22 in view of soaring domestic prices of the metal. As per BigMint data, finished flats imports have grown phenomenally since then.

Domestic production falls short on demand and competitiveness: India’s stainless steel capacity is around 7.3-7.7 mnt for both long and flat products. The capacity of flat products is around 5 mnt, while longs are around 2.7 mnt. Consumption of stainless steel is projected to increase by 22% y-o-y in FY’25 from 3.6 mnt in FY’24. Consumption for FY’25 is expected to reach 4.5 mnt and is expected to increase further by FY’30. This growth aligns with India’s economic expansion and substantial infrastructure investments, which are likely to drive stainless steel demand to 6.6-6.8 mnt by FY’30.

Decline in scrap imports: In FY’25 India’s stainless steel scrap imports is expected to drop 9% to 1.2 mnt from 1.32 mnt in FY’24. However, due to limited domestic SS scrap supply (25-30%), the industry relies heavily on imports, leading to challenges in securing adequate volumes and also global price volatility, not to mention increasing restrictions on global scrap exports. The decline in scrap imports was offset by higher imports of semis (slabs & billets) and finished products.

Outlook

The industry has pitched for trade measures to contain opportunistic dumping of stainless steel but India will remain heavily reliant on imports to meet its demand. Notably, stainless steel lies outside the ambit of the proposed 12% safeguard duty on flat steel imports.

Moreover, with the EU and other major geographies clamping down duties to contain imports, there is the distinct possibility of shipments being channeled to high-growth markets with fewer trade restrictions such as India.

Steady increase in consumption (by some accounts, domestic per capita consumption has reached 3.1 kg) coupled with low domestic capacity utilisation and cost competitiveness will ensure that the country remains an importer of stainless steel.

However, with new capacities coming up and offshore investments by producer for raw material security, there is hope that a surge in domestic production will counterbalance imports.

Leave a Reply