- Limited buying interest in India amid bid-offer gap

- Turkish mills cautious amid political uncertainty

South Asia’s imported scrap market remained subdued as buyers navigated bid-offer disparities, weak demand, and holiday-driven slowdowns. In India, despite improved domestic steel demand, firm offers kept trade limited. Pakistan’s market saw minimal activity due to Ramadan and the upcoming Eid holidays, delaying fresh bookings.

Bangladesh faced resistance to high offers, with limited LC approvals tightening liquidity, though prices may soften post-Eid.

Meanwhile, Turkiye’s market remained stable but cautious, with mills holding back on purchases amid political uncertainty and currency concerns.

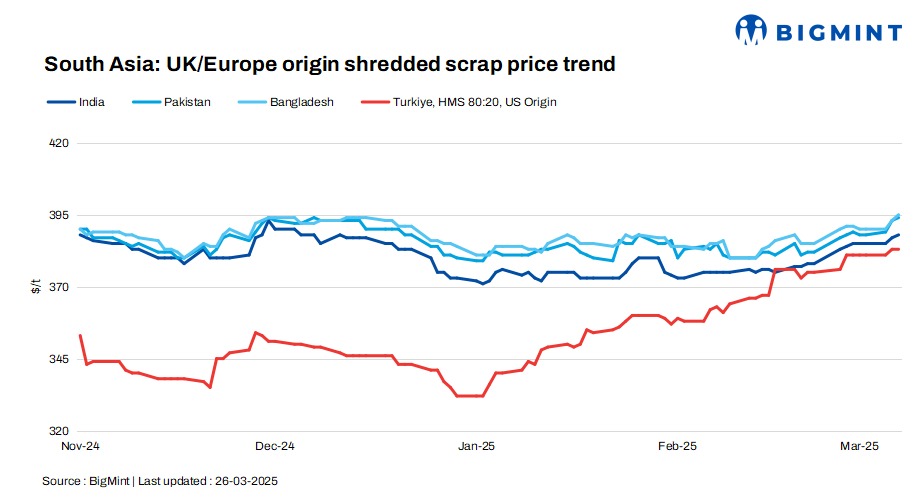

UK-origin shredded scrap edged up by $1/t in India and Pakistan and $2/t in Bangladesh. US-origin bulk HMS 80:20 offers to Turkiye remained unchanged d-o-d.

Overview

India: India’s imported scrap market remained in a stalemate as bid-offer gaps persisted despite improved domestic steel demand. Buyers showed interest, but firm offers kept trade limited. Shredded scrap offers stood at $388-395/t CFR, while bids lagged at $385-388/t, making transactions unviable. HMS 80:20 from UK/Europe and West Africa saw offers at $360-370/t CFR, but buyers targeted $355-360/t. Limited availability at preferred bid levels further slowed trade. Sellers favoured Pakistan due to higher price realisations.

Pakistan: Pakistan’s imported scrap market saw minimal activity as reduced working hours and religious focus during Ramadan kept buyers on the sidelines. The month- and quarter-end, coupled with the upcoming Eid holidays, further limited purchasing interest, with the market expected to fully reopen on 7 April. UK-origin shredded scrap was indicated at $395-400/t CFR Qasim, though buyers saw tradable levels closer to $390-395/t CFR.

Bangladesh: Bangladesh’s imported scrap market remained sluggish as buyers resisted high offers, creating a $5-7/t bid-offer gap. Limited LC approvals had previously driven domestic scrap prices higher, but with Eid approaching and no new LCs expected for 10 days, prices may soften.

Buyers preferred nearshore suppliers like Australia and Hong Kong over UK/Europe-origin material.

Deals were heard for PNS from Hong Kong at $390/t CFR and Australian shredded at $390/t CFR. Domestic rebar prices ranged from BDT 80,000-86,000/t, while imported scrap offers stayed firm despite limited demand.

Turkiye: The Turkish imported scrap market remained stable, with mills stepping back from restocking amid ongoing political protests and currency concerns. US-origin bulk HMS (80:20) offers stayed at $383/t CFR, as sellers resisted mill pressure for lower prices, while EU-origin offers ranged from $375-380/t CFR. Mills hesitated to book new cargoes, with some considering production cuts or alternative methods due to firm scrap offers and domestic rebar market uncertainty. The approaching Eid holidays also added to the cautious sentiment in the market.

Price assessments

India: UK-origin shredded indicatives were assessed at $388/t CFR Nhava Sheva, up by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives stood at $394/t CFR Qasim, up by $1/t d-o-d.

Bangladesh: UK-origin shredded indicatives remained rose by $2/t d-o-d to $395/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $383/t CFR Turkiye, unchanged d-o-d.

Leave a Reply