- Absence of active fixtures on India-China route

- Baltic Supramax Index (BSI) up 82 points w-o-w

Dry bulk iron ore freights from Indian ocean to China are stable w-o-w. Demand for key commodities such as iron ore, coal, and agricultural products from India to China has remained firm, especially with restocking activity for April shipments. While March cargoes were mostly covered, the emergence of new cargoes for the upcoming month has added pressure on vessel availability.

Additionally, with shipowners maintaining high fixing ideas, particularly in the Asia-Pacific region, freight rates have been supported despite mixed sentiments in other markets. A slight imbalance between vessel availability and cargo demand has influenced the rate increase.

However, the increase in Capesize vessel freight rates can be attributed primarily to tightening tonnage availability in the Atlantic. A significant reduction in ballasting vessels has limited the supply of ships in the region, leading to higher freight rates. This tightening is driven by a combination of increased cargo demand and a slower replenishment of available tonnage.

As vessel supply remains constrained in these regions, freight rates have found support. Unlike the Pacific market, where excess tonnage and slow activity have kept freight rates subdued, the Atlantic market dynamics have provided a more favourable environment for rate improvements.

Factors influencing freights

- Baltic indices show mixed trends w-o-w: The Baltic Dry Index (BDI) was recorded at 1,643 points on 24 March, decreasing by 26 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,676 points, down 181 points w-o-w, reflecting volatile market sentiment. However, the Baltic Supramax Index (BSI) inched up by 82 points w-o-w to 1,012 points.

- China’s iron ore spot prices fall by $1/t w-o-w: China’s spot prices of iron ore fines (Fe62%) were assessed at $102.55/t CFR on 25 March, down by $1/t w-o-w, as cautious trading slowed the overall buying activity with the market anticipating production cut news. Steel mills are analysing the impact of the production cut on prices. Prices dropped at Chinese ports with some medium-grade fines procured.

Route-wise updates

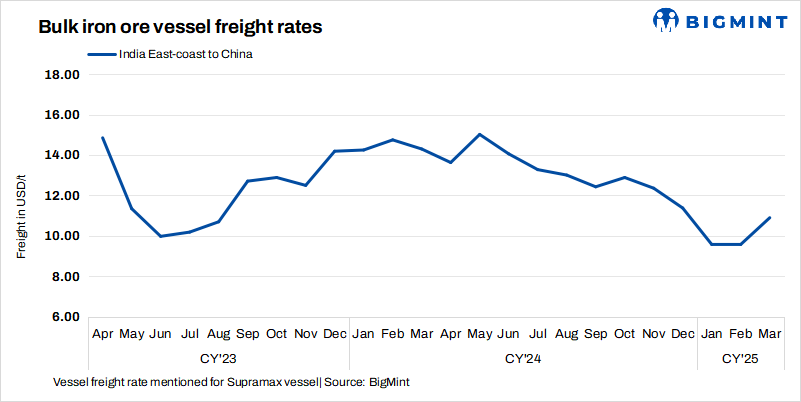

- India-China: Freights from the Indian Ocean to China were recorded at $11/t, edging up by $0.1/t w-o-w. However, fixtures remain muted in this route. Meanwhile, a Charter commented, “We are seeing increased aggression among traders in securing iron ore orders”

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $9.1/t on 26 March, down $0.9/t w-o-w. According to sources, Australian miner Rio Tinto was seen actively booking Capesize vessels from a Western Australia port to Qingdao Port at around $9-9.30/t. Shipment is scheduled for 9-11 April. However, an increasing supply of vessels in the Pacific, coupled with subdued iron ore cargo activity, led to lower freight rates.

- Brazil-China: Freights for Capesize vessels from Brazil to China rose this week. Rates from Tubarao to Qingdao Port were assessed at $24.45/t on 26 March, up by $0.45/t w-o-w. As per sources, one Capesize vessel was booked from Tubarao to Qingdao at around $24/t, with shipment scheduled for 11-20 April.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port increased by $0.80/t w-o-w to $18.7/t amid limited vessel availability. One Capesize vessel was booked from Saldanha Bay to Qingdao at $19/t, with shipment scheduled for 11-17 April.

Leave a Reply