- Scrap demand recovers in Vietnam but mills remain cautious

- Taiwan’s imported scrap market stable as mills favor billets

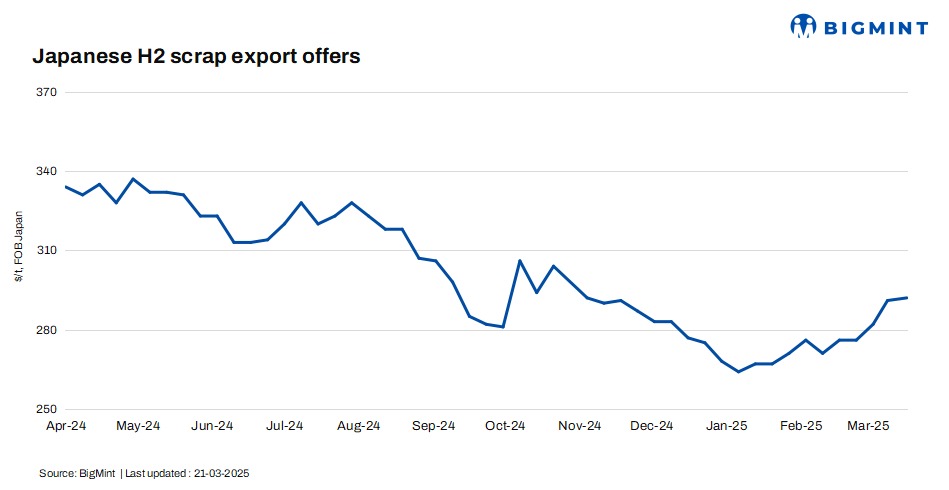

Japanese H2 scrap export prices rose in the week, driven by firm offers following the Kanto March tender and a weaker yen. With April shipment quotas already fulfilled, some suppliers opted for a wait-and-see approach. Vietnam’s demand showed slight improvement due to ongoing construction activity, but weak mill margins and cautious sentiment kept buying limited. Meanwhile, strong buying interest from Bangladesh continued to support prices.

Despite subdued domestic demand in Japan, scrapyards maintained firm offers, keeping export prices elevated. While deep-sea scrap demand remained sluggish, some mills preferred Japanese material for its competitive pricing.

Thus, BigMint’s weekly assessment of Japanese H2 scrap export offer stood at JPY 43,500/t ($292) FOB Tokyo Bay, up by JPY 400/t ($2.6/t) in comparison with JPY 43,100/t ($290/t) in the previous week.

Moving forward, H2 scrap prices are expected to remain rangebound amid cautious mill restocking and weaker Chinese futures market trends.

Other market updates

Vietnam: Vietnam’s imported scrap market saw moderate demand recovery during week, driven by improving construction activity and government project disbursements. However, mills remained cautious due to weak margins and uncertainties in the steel market. Japanese H2 scrap offers ranged from $333-345/t CFR Vietnam, while bids were mostly below $330/t CFR, reflecting a persistent bid-offer gap.

Some buyers opted to stay on the sidelines, waiting for price clarity. Deep-sea scrap liquidity remained thin, with mills favoring Japanese cargoes for their competitive pricing. Despite speculative gains in domestic steel prices, mills were hesitant to accept higher-priced scrap, keeping overall demand in check. Looking ahead, scrap prices are expected to remain rangebound.

South Korea: South Korea’s imported scrap market remained sluggish in mid-March, with weak seaborne demand driven by falling domestic rebar prices, low mill operations, and slow rebar sales. Ferrous scrap inventories at major mills increased by 22,000 t due to reduced production activity, leading to higher stockpiles in both central and southern regions. Imports dropped to 50,713 t from 54,554 t earlier in the month, with Hyundai Steel maintaining its lead at 36.7% of total imports. Special steel companies accounted for 44.8% of imports, slightly lower than early March.

Taiwan: Taiwan’s imported scrap market remained stable as mini-mills held off on price changes due to market uncertainty. Feng Hsin Steel kept its rebar and domestic scrap buying prices unchanged for 17-21 March. US-origin HMS 80:20 scrap paused at $320/t CFR Taiwan, while Japan-origin H2 scrap remained at $325/t CFR. Some mills reduced scrap consumption, opting for billets from China due to competitive pricing. Meanwhile, Chinese rebar prices fluctuated slightly, fueling a wait-and-see sentiment in Taiwan.

Outlook

Japanese H2 scrap export offers are expected to remain firm in the near term, supported by strong buying interest from Bangladesh and tight supply after the Kanto tender. However, a cautious outlook prevails as weaker Chinese futures and slow deep-sea demand may cap further gains. In Vietnam, scrap demand is recovering, but mills remain hesitant due to weak margins and a persistent bid-offer gap. Meanwhile, Taiwan’s market is likely to stay stable, with mills favoring billets over imported scrap amid price uncertainty and fluctuating Chinese rebar prices.

Leave a Reply