- Shipments to key South Asian nations edge down on softening demand

- Higher EU crude steel production, scrap usage affect exports

- Growing export restrictions amid CBAM phase-in to hit developing countries

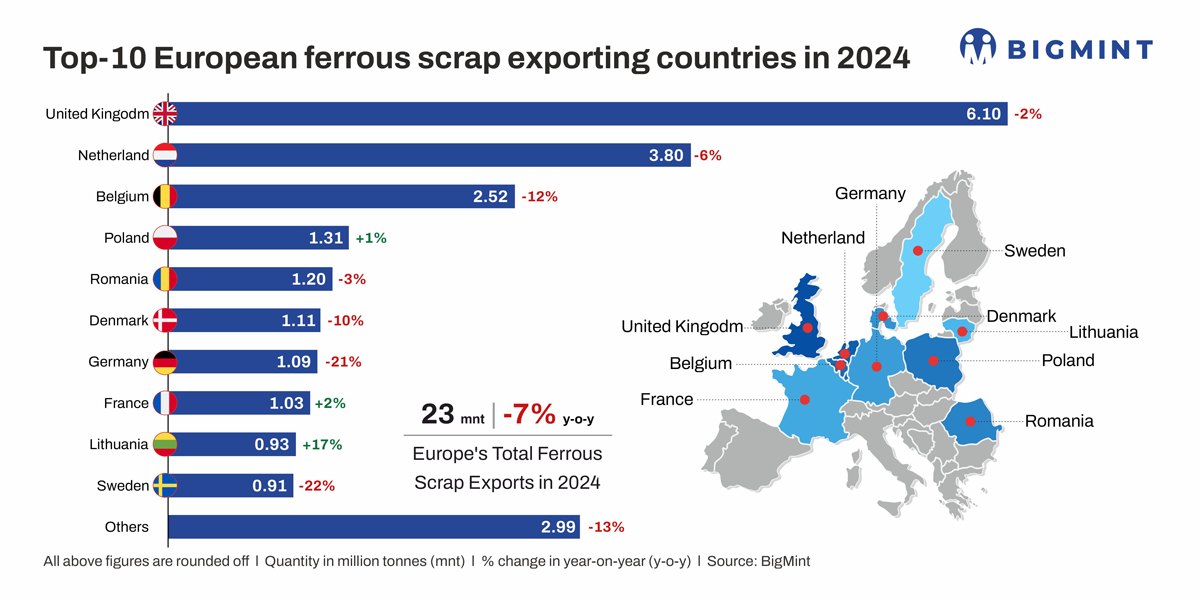

Morning Brief: In calendar year 2024 (CY’24), exports of ferrous scrap, or recycled ferrous material, by the European Union (EU) and the United Kingdom (UK) to third countries (excl. inter EU trade) fell by 7% y-o-y to 23 million tonnes (mnt), as per BigMint data.

The decline was driven by reduced shipments to major destinations such as India, Bangladesh, and the United States, while Turkiye increased its intake. Exports by the EU and UK in CY’23 were 24.67 mnt.

Major scrap buyers

Turkiye remained the dominant importer, receiving 9.9 mnt (+31% y-o-y), accounting for over 60% of total exports, as the country’s crude steel production increasing nearly 10% y-o-y.

The other major destinations were:

- Egypt: 1.7 mnt (+23% y-o-y)

- India: 840,000 t (-52% y-o-y)

Combined with Pakistan, these four countries collectively accounted for over 80% of total EU ferrous scrap exports.

Country-wise exports

In CY’24, Germany’s ferrous scrap exports plummeted 20% y-o-y to 1.09 mnt, compared to 1.37 mnt in CY’23, reflecting weaker demand from key buyers outside the EU-27, such as India, and higher domestic crude steel production

Meanwhile, Belgium’s scrap exports dropped 16% y-o-y to 2.34 mnt, down from 2.78 mnt in CY’23, as demand from India and Pakistan weakened. The Netherlands, a key scrap supplier, recorded a 12% y-o-y decline, with exports falling to 2.91 mnt from 3.31 mnt in CY’23.

In the United Kingdom, the ferrous scrap market faced supply constraints, resulting in heightened competition for all ferrous grades. Exports fell by 2% y-o-y to 6.1 mnt.

Why scrap exports shrunk?

Higher EU consumption: As per World Steel Association, crude steel production in the EU stood at 129.5 mnt in CY’24, an increase of 2.6% y-o-y.

The EU increased scrap consumption by 8.8% y-o-y in H1CY’24, as per Bureau of International Recycling (BIR) data. In CY’24, the EU’s ferrous scrap consumption is estimated at 87–89 mnt, reflecting steady domestic steel production.

The European Central Bank (ECB) stepped in with rate cuts to breathe life into the sluggish EU economies in the year gone by. The ECB made its first move in nearly five years, lowering its main rate by 0.25% points to 3.75% in June, and again to 3.5% in September.

The cuts were an attempt to revive demand and stall the decline in economic growth. This naturally drove consumption.

Decline in shipments to key countries: Overall scrap exports edged down due to the notable decline in shipments to key countries in South Asia, while exports to Turkiye edged up. Exports to India dropped over 50% y-o-y on higher consumption of domestic scrap in India.

Moreover, geopolitical upheavals and the Red Sea crisis dampened demand for imported scrap among key Asian buyers. The decline in exports to India and Pakistan indicates a change in the regional demand structure and possible changes in supply chains. Shipments to Bangladesh headed south on economic and political uncertainties, currency devaluation, and LC opening hurdles.

Declining scrap collection rates: The decline in exports was fuelled by reduced collection rates, with scrap availability dropping from 90.2 mnt in CY’23 to 85-86 mnt in CY’24. Tightening supply limited export volumes, particularly from key exporting countries like Germany, Belgium, and the Netherlands.

Global steel overcapacity, assessed by the European Commission (EC) at over four times the EU’s annual steel consumption, and higher exports by China weighed on global scrap demand and prices.

Trade protectionism amid industry transition: EU regulatory initiatives aimed at preserving scrap — a key industry decarbonisation lever –for domestic production are gradually limiting third countries’ access to European raw materials. EUROFER and IndustriAll have called on the European Commission and EU member states to recognise ferrous scrap as a strategic secondary raw material under the Critical Raw Materials Act and are urging the EC to impose export restrictions beyond the Waste Shipment Regulations (WSR).

Tightening of the WSR could place further restrictions on scrap exports, particularly to Turkiye, which accounts for over 60% of the EU’s scrap exports.

Outlook

While the EU’s steel sector is still predominantly reliant on primary steelmaking, with the BF-BOF route accounting for nearly 60% of the continent’s steel production, climate targets are driving the shift to EAFs, with GMK Center data showing that nearly 50 mnt of fresh capacity, including announced projects after 2027, is likely to come up, if not more.

Although low-emission DRI is likely to emerge as a key feedstock, more scrap will be retained for domestic steel production amid decarbonisation efforts.

Plus, the EU is making efforts to ratchet up domestic scrap usage. To facilitate the uptake of secondary content in sectors traditionally dependent on primary metals, the EU is putting emphasis on proper sorting and treatment of scrap to ensure its usability in high-quality applications such as automotive.

The EC will prepare the setting of targets for recycled steel in key sectors and will also assess the need for recyclability and/or recycled content requirements for additional product groups. Measures such as reciprocal scrap export restrictions on third countries are also being mulled, which will impact exports.

Leave a Reply