- IF rebar prices fluctuate by INR 100-600/t

- HRC trade prices show mixed trends w-o-w

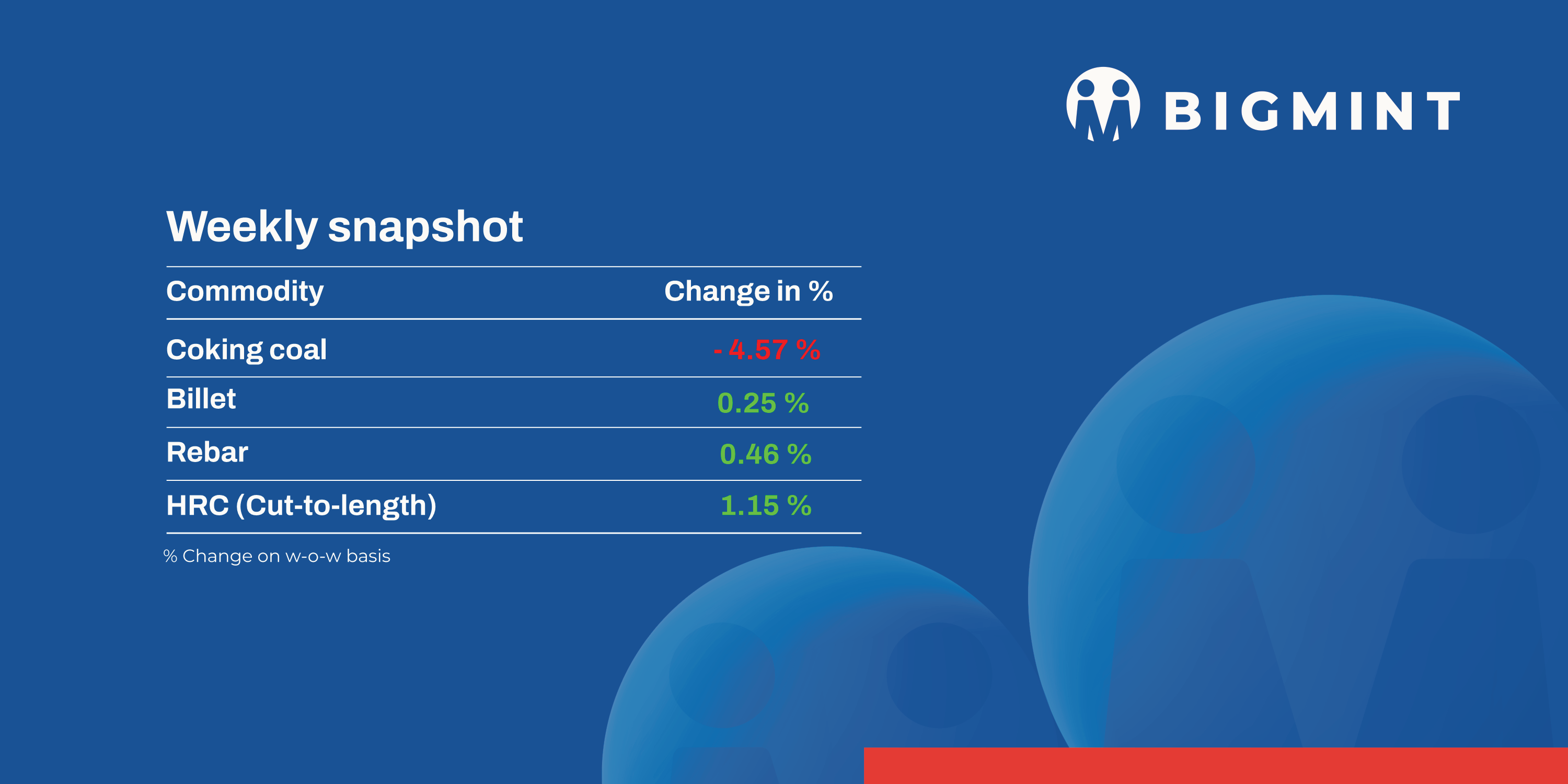

The domestic steel market saw a slowdown in activity amid the Holi festival. Overall, prices witnessed mixed trends during week 11 (10-15 March 2025). Semi-finished steel prices fell by INR 50-500/tonne (t), while sponge iron tags showed mixed trends.

Iron ore, pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index remained stable w-o-w at INR 9,850/tonne (t) ($113/t) DAP Raipur on 11 March 2025. Last week, deals for around 35,000 t of pellets (Fe62/63%) were concluded by Raipur-based steelmakers at INR 9,600-9,800/t exw-Raipur. Around 10,000 t of higher-grade pellet (Fe65%) were also traded in the Raipur region.

- Freights from the Indian Ocean to China were recorded at $10.7/t, inching down by $0.3/t w-o-w. Although no new fixtures were finalised, some rumours suggest otherwise. Freights from India to China edged down following limited inquiries, a surplus of prompt tonnage, and subdued market activity across key regions. In the Indian Ocean, a lack of fresh cargo along the Indian coasts exerted downward pressure on rates.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) remained stable w-o-w at $96/t on 12 March. Additionally, the Indian low-grade iron ore fines (Fe 57%) export index remained stable w-o-w at $62/t FOB east coast, India, on 13 March. Export deals remained absent in the east coast following weak market sentiments and a lack of buying interest.

Coal

- Portside South African thermal coal prices were under pressure amid weak buying interest. South Africa’s thermal coal exports declined to a 7-month low in February 2025.

- BigMint’s coking coal index, CNF India. edged down by $2/t amid a bid-offer disparity. Additionally, India’s coking coal imports dropped 25% m-o-m in February 2025.

- India’s domestic met coke prices remained largely stable w-o-w. India’s met coke imports saw a sharp decline of 64% m-o-m in February 2025 to 0.13 mnt, a 2.5-year low.

Ferrous scrap

- India’s imported scrap market remained sluggish throughout the week, burdened by a persistent bid-offer mismatch and subdued buying interest. UK/EU-origin shredded offers hovered at $375-380/t CFR Nhava Sheva, while bids were slightly lower at $370-375/t. HMS 80:20 from the same region was quoted at $355-360/t CFR. In Chennai, buyers leaned towards sponge iron due to cost advantages, which kept imported scrap demand in check. Despite stronger finished steel sentiment and a rise in global scrap prices, Indian traders remained cautious amid unworkable margins and stiff yard offers.

- UK-origin shredded scrap prices edged up by 1% w-o-w to $378/t CFR India; however, trade activity was limited, reflecting cautious sentiment among buyers. Holi-related holidays restricted any notable upward movement.

- Approximately 4,500-5,000 t of scrap were booked, including 3,000-3,500 t of HMS 80:20 from Australia and West Africa at $350-382/t. Additionally, 500-1,000 t of HMS-LMS bundle mix scrap from Yemen were traded at $348/t, while 1,500-2,000 t of tin can bundle scrap from Israel were booked at $290-300/t.

Ferro alloys

- Silico manganese: Indian silico manganese prices dropped slightly by INR 150/t ($2/t) w-o-w to INR 71,500-73,100/t ($823-842/t) in the key regions of Durgapur, Raipur, and Vizag. Prices dipped due to an imbalance in supply and demand, whereas tags of the medium-carbon variant prices rose, driven by an increase in high-grade ore prices.

- Ferro manganese: Indian ferro manganese (HC 70%) prices inched up w-o-w to INR 76,000/t ($875/t) exw in Durgapur. Meanwhile, in Raipur, prices rose by INR 300/t ($3/t) to INR 75,900/t ($874/t) exw. Both increases were due to a rise in high-grade ore prices.

- Ferro silicon: Indian ferro silicon prices were unchanged w-o-w at INR 99,600/t ($1,147/t) exw-Guwahati. In Bhutan, prices inched down by INR 200/t ($2/t) to INR 99,600/t ($1,147/t) exw. Around 6 suspended ferro silicon plants in Meghalaya resumed operations last week.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices remained stable w-o-w. Additionally, China’s TISCO kept its ferro chrome tender price unchanged for March 2025 at RMB 6,795/t ($939/t) DAP, including taxes.

Semi-finished

- Indian semi-finished steel prices showed a downtrend as per BigMint’s assessment. Billet prices in almost all key locations decreased by INR 50-500/t. Prices increased in only Ahmedabad, by INR 300/t. Meanwhile, sponge iron prices showed mixed trends, with almost all key locations seeing a drop of INR 50-400/t, with the steepest fall of INR 400/t seen in Chennai. Conversely, prices increased in Mandi Gobindgarh, by INR 200/t.

- Indian direct reduced iron (DRI) export offers increased by $7/t for CPT Raxaul to $348/t, while CPT Benapole offers increased by $1/t to $341/t.

- Tata Metaliks increased prices of foundry-grade pig iron by INR 1,500/t ($17/t) due to tight supply and robust demand. Post-revision, prices stood at INR 39,000/t ($447/t) exw-Kharagpur. These prices are applicable for the Kolkata and Howrah markets.

Finished long steel

- IF rebar: The induction furnace (IF) route long steel segment saw limited trading activity in the spot market, with buyers purchasing material based on their immediate needs. Labour shortages and logistical challenges, exacerbated by the Holi festival, further contributed to a slowdown in market activity. As a result, buyers focused on need-based purchasing. Market participants expect prices to remain range-bound in the near term.

- On a w-o-w basis, IF rebar steel prices fluctuated by INR 100-600/t across regions, as per BigMint’s assessment.

- The trade reference prices of Fe 500 grade rebars manufactured via the IF route for 10-25 mm size were assessed at INR 43,300-43,700/t exw-Raipur and INR 48,700-49,300/t exw-Jalna.

- The trade reference price of heavy structural steel for base size 150 mm channel stood at INR 44,800-45,300/t exw-Raipur.

- The trade reference price of wire rods hovered at INR 44,000-44,500/t ex Raipur.

- BF rebar: Trade-level blast furnace (BF) rebar prices rose w-o-w across major markets amid ongoing material shortages. A pre-Holi slowdown in the trade segment and logistics disruptions further constrained supplies, leading to a scarcity of material in the distribution channel. Demand in the trade segment remained slow this week.

- Current week’s rebar prices (12-32 mm) in the trade segment edged up by INR 100/t w-o-w to INR 54,400/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the project segment, prices rose w-o-w to around INR 53,000-54,000/t FOR Mumbai basis.

Flat steel

- Trade-level hot-rolled coil (HRC) prices showed mixed trends w-o-w, maintaining a range of INR 48,900-51,000/t across India. However, cold-rolled coil (CRC) prices remained firm w-o-w, settling at INR 54,800-58,800/t across markets.

- HRC prices showed mixed trends w-o-w, with some markets witnessing an increase, while tags fell or remained stable in others. Demand gradually dwindled ahead of Holi.

- India’s bulk imports of HRCs and plates touched 114,530t on 10 March 2025, according to vessel line-up data with BigMint. An additional 136,344 t are expected to arrive by the end of this month.

- BigMint’s price index for Indian HRC (SAE1006) exports to the Middle East and Vietnam remained steady w-o-w. Recent export deals to the Middle East kept prices stable at $495/t (FOB main port, India). In Vietnam, buyers focused on domestic HRCs despite rising mill prices. Meanwhile, the European market remained slow due to ongoing anti-dumping investigations.

Leave a Reply