- Japan sees higher H2 export offers post-Kanto tender

- Turkish mills exercise caution amid high seller targets

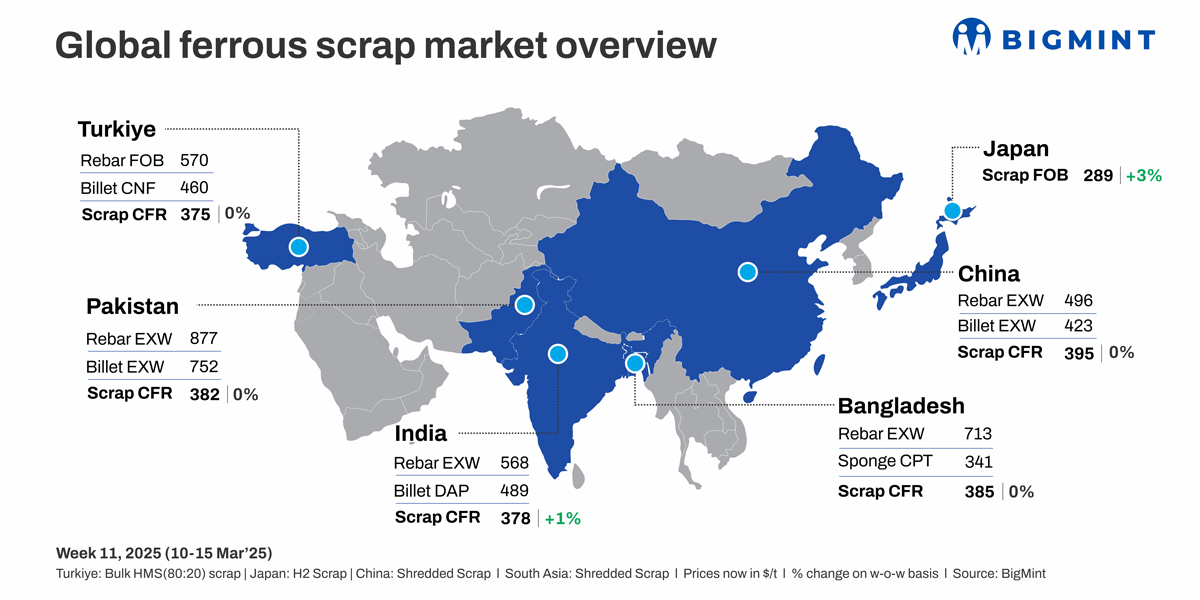

Global ferrous scrap offers remained stable this week, with limited activity across South Asia due to Ramadan and Holi. Turkiye saw mixed sentiment amid firm seller positions. India and Pakistan faced weak demand, while Bangladesh’s market was muted due to letter of credit (LC) delays. Japan’s H2 prices rose following the Kanto tender, while US offers increased on tight supply.

Turkiye: The imported scrap market displayed mixed sentiment throughout the week, beginning with a slight $3/tonne (t) dip in prices due to limited activity and declining collection costs in Benelux. Despite the soft start, sellers – particularly from the EU – held firm and rejected lower bids, maintaining bullish expectations. The euro’s slight depreciation created minor pressure, but overall sentiment remained supported, with US- and EU-origin HMS 80:20 offers hovering at around $370-375/t CFR.

As the week progressed, EU and Baltic suppliers raised offers, driven by the euro’s appreciation and strong seller confidence. US recyclers aimed for higher prices, with some pushing up to $390/t CFR, although Turkish mills tried to resist them.

India: India’s imported scrap market remained sluggish throughout the week, amid a persistent bid-offer mismatch and weak buying interest. UK/EU-origin shredded was offered at $375-380/t CFR Nhava Sheva, while bids were at $370-375/t. HMS 80:20 was quoted at $355-360/t CFR. In Chennai, buyers favoured sponge iron due to cost benefits, keeping scrap demand muted. Despite stronger finished steel sentiment and rising global scrap prices, Indian traders remained cautious due to unworkable margins and high yard offers.

UK-origin shredded prices edged up by 1% w-o-w to $378/t CFR India; however, trade activity remained limited, reflecting a cautious sentiment among buyers. Holi-related holidays restricted any meaningful upward movement.

Approximately 4,500-5,000 t of scrap were booked, including 3,000-3,500 t of HMS 80:20 from Australia and West Africa at $350-382/t. Additionally, 500-1,000 t of HMS-LMS bundle mix scrap from Yemen were traded at $348/t, while 1,500-2,000 t of tin can bundle scrap from Israel were booked at $290-300/t.

Pakistan: The imported scrap market in Pakistan remained largely inactive this week, as Ramadan slowed down activity and mills operated at reduced capacity. UK/EU-origin shredded offers stood at $380-385/t CFR Qasim, but bids were at $378-380/t. Mills focused on maintenance amid payment delays and ample local scrap availability. UK shredded prices were steady w-o-w at $382/t CFR Pakistan.

Traders are optimistic about a possible rebound in demand post-Eid, expecting increased bookings in April-May as market clarity improves.

Bangladesh: The imported scrap market remained quiet amid Ramadan and weak demand. UK/EU-origin shredded offers held at $385/t CFR Chattogram, while Japanese H2 was estimated at $360-365/t CFR, supported by firm FOB levels and freights. Slow LC processing and pricing uncertainty kept market sentiment muted. UK shredded prices remained flat w-o-w at $385/t CFR.

Some buying interest was seen for material from nearby origins such as Australia, Hong Kong, Singapore, and Malaysia, though high prices – especially Hong Kong offers above $390/t CFR – were largely deemed unworkable. Australian shredded was offered at $375-380/t CFR, while HMS 90:10 hovered at around $362-365/t CFR.

Japan: H2 scrap export offers rose w-o-w, supported by stronger sentiment post the March Kanto tender, where the winning bid climbed up by JPY 1,026/t ($7/t) m-o-m for a 15,000 t cargo to Bangladesh. Limited availability and a firm seller stance further backed prices.

Domestic scrap prices stayed mostly stable, with the national average at JPY 38,000/t ($256/t), reflecting a balanced supply-demand outlook.

Vietnam: The imported scrap market remained sluggish, as buyers resisted post-Kanto tender price hikes. Japanese H2 offers rose to $340/t CFR, but mills held back, expecting corrections. While rising finished steel prices offered some support, costly US-origin deep-sea scrap at $360-365/t CFR kept demand weak.

The HS grade remained preferred for its quality and flexibility, though high prices pushed some suppliers to shift focus to India, Bangladesh, and Turkiye.

South Korea: The scrap market remained steady despite a 26,000 t w-o-w inventory drop to 609,000 t. The central region saw sharper declines, led by Hyundai Steel Dangjin (-12.5%) and Dongkuk (-8%), while the southern region stayed mostly stable.

Weak construction demand kept mills cautious, which adjusted production volumes instead of engaging in aggressive restocking. No signs of shortages or price swings were observed.

US: Ferrous scrap export offers rose by up to $9/t w-o-w, driven by tight supply and rising domestic prices. Trade tensions with Canada added pressure, as winter slowed collection and tariffs disrupted flow. Buyers remained cautious despite firm US steel market support and limited availability.

Leave a Reply