- Labour shortages, logistics disruptions emerge

- BF rebar tags edge up as tight supply persists

- HRC, IF rebar prices fluctuate across markets

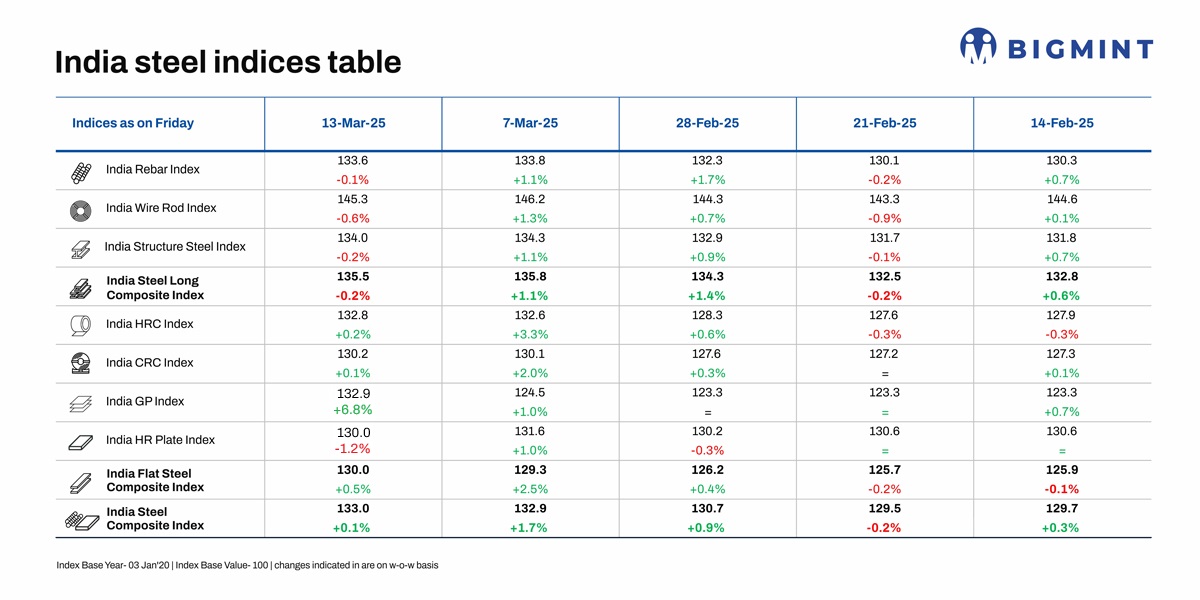

Morning Brief: BigMint’s India Steel Composite Index remained largely stable at 133 points on 13 March 2025, inching up by a minuscule 0.1% w-o-w ahead of Holi. Markets saw muted activity, with most participants busy gearing up for the festival of colours.

The sub-indices were a mix of red and green, with longs down by 0.2% w-o-w and flats up by 0.5%. Galvanised plain (GP) saw a surge of 6.7%, fuelled by a substantial price hike of INR 1,800/tonne (t) w-o-w in Mumbai.

Encouragingly, despite divergent price trends, the steel index remained in the green overall, still straddling a four-month high.

Factors impacting index last week

Supply shortfalls support BF rebar tags: Trade-level blast furnace (BF) rebar prices inched up w-o-w across markets, as the supply crunch seen over the past few weeks persisted. In Mumbai, trade-level BF rebar prices edged up by INR 100/t ($1/t) w-o-w to INR 54,400/t ($626/t) exy, exclusive of GST at 18%.

Last week, the supply deficit was compounded by two factors: Market activity in the trade segment was much lighter, with labourers and other participants away due to the Holi festival.

Additionally, due to the same reason, logistical disruptions emerged, hindering material flow to the distribution channel.

Another key contributor was a list price hike by major private steel mills. Post revision, prices hovered at INR 54,000-54,500/t ($621-627/t) on landed basis, up by INR 750/t ($9/t).

In the projects segment, prices trended up, hovering within INR 53,000-54,000/t ($610-621/t) FOR Mumbai.

IF rebar fluctuates amid festive slowdown: Induction furnace (IF) rebar prices showed varying trends across India, with prices falling in certain clusters due to poor trades. In the Mumbai cluster, prices moved up by INR 100/t ($1/t) w-o-w to INR 49,400/t ($568/t) exw.

The IF segment, which commands 65-70% of the rebar market, continued to witness decent bookings last week. Additionally, mills, having witnessed steady and sufficient offtake in recent times, saw inventory idling time decline to 8-10 days. While these factors helped propel prices in some regions, the gains were capped by sluggish trade activity ahead of Holi, stemming from labour shortages and logistics challenges. Some suppliers faced inventory pressure, which led to price drops.

HRC prices show divergent trends w-o-w: Trade-level HRC prices showed mixed trends w-o-w, settling at INR 48,900-51,000/t ($562-587/t) across India. In Mumbai, prices increased by INR 600/t ($7/t) w-o-w to INR 49,600/t ($570/t) exw, excluding 18% GST.

Trade momentum was muted due to Holi, with both demand and supply contracting. Additionally, there were no signs of the safeguard duty announcement, which suppliers are eagerly looking forward to. This led to market uncertainty and varying price trends.

HRC export offers hold firm w-o-w: BigMint’s India HRC (SAE1006) export index (for the Middle East and Vietnam) remained stable w-o-w at $495/t FOB main port India. Indian mills’ offers to the UAE held steady w-o-w at $515/t CFR, while China’s offers to the Middle East remained stable at around $500-515/t CFR. Additionally, Indian mills continued to refrain from actively offering HRCs in the EU market amid the anti-dumping investigation. Offers are likely to resume with the EU anti-dumping investigations leaving India unscathed.

Notably, the European Commission, following a review of its current steel industry safeguard measures, has cut its import quotas for several products and countries. India, in particular, has had its HRC quota slashed by around 25%. This will further curtail India’s export volumes, a development which raises concerns given that India’s HRC imports still remain at an elevated level y-o-y. India recorded 0.41 mnt of bulk HRC and plate arrivals in February compared to 0.34 mnt in the year-ago period.

Outlook

Certain segments continue to have a bullish outlook for the near term. For example, trade-level BF rebar prices are likely to continue increasing, considering mills’ plans to raise list prices multiple times this month amid material shortages. Additionally, IF rebar prices may recover as market operations normalise after the festive slowdown.

However, given that the HRC segment continues to grapple with weak demand and a surfeit of cheap imported material, concerns have emerged regarding the delayed implementation of the steel safeguard duty. The post-Holi period may see price drops if the current uncertainty persists.

Export offers, on the other hand, are expected to take a beating following the new steel import quotas of the EU.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply