- Removal of BCD on ferro nickel boosts imports

- India’s stainless steel scrap imports drop 9% y-o-y

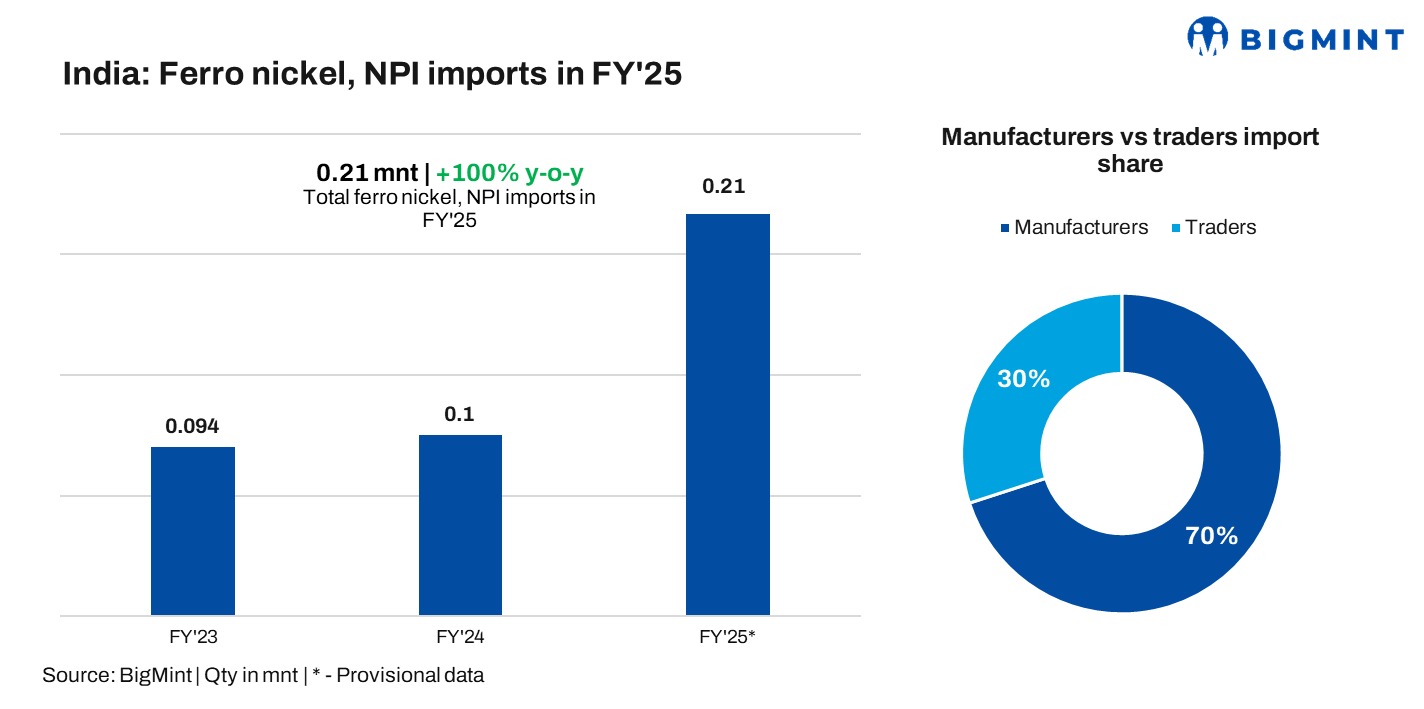

India’s ferro nickel and nickel pig iron (NPI) imports to see a significant increase of 100% y-o-y in FY’25, as per provisional data maintained with BigMint. Imports rose to 0.21 mnt in FY’25 from 0.1 mnt in FY’24.

Meanwhile, imports rose by 88% y-o-y in CY’24 reaching 0.2 mnt from 0.11 mnt in CY’23.

India’s ferro nickel imports were made by 23 players, with 13 coming from the stainless steel manufacturing segment, with the remaining being traders.

What drove ferro nickel, NPI imports in FY’25?

Removal of BCD on ferro nickel imports: In the FY’25 budget, India waived off the 2.5% Basic Customs Duty (BCD) on ferro nickel (FeNi), a critical raw material in the stainless steel industry. This waiver is notable because India currently depends entirely on imports to meet its ferro nickel requirements. The decision is aimed at reducing the cost of production of domestic stainless steel.

Following the removal of the BCD, India’s imports of ferro nickel surged by 125%, increasing from 0.09 mnt in FY’23 to 0.21 mnt in FY’25. This decision came after industry actively advocated for the removal of customs duties on ferro nickel and ferro-molybdenum in January 2024, ahead of the Union Budget, to ensure competitive pricing for these crucial raw materials. At that time, the customs duty on ferro nickel was 2.5%.

Drop in NPI prices in Q4CY’24: Towards the end of 2024, Indonesia’s release of RKAB supplementary quotas coincided with declining premiums and HPM prices, which weakened nickel ore prices.

This shift lowered smelter production costs, boosting NPI production. However, the fall in LME nickel prices and weaker downstream demand led to losses for high-grade nickel matte. As NPI production became more profitable, Indonesian smelters prioritised NPI, increasing supply. The growth in NPI supply outpaced the incremental demand in Indonesia, leading to a rise in exportable volumes. The increased availability of export permits further supported smoother shipments of stockpiled inventories.

Exports of ferro nickel from Indonesia saw an increase of 10% in FY’25, reaching 9.9 mnt from 9 mnt in FY’24.

Declining stainless steel scrap imports: As per provisional data maintained by BigMint, India’s stainless steel scrap imports saw a 9% drop in FY’25 settling at 1.2 mnt from 1.32 mnt in FY’24 amid increased arrivals of stainless steel semis and ferro nickel/NPI which reduced the reliance on scrap in the making of stainless steel finished products and preference for domestic scrap amid volatility in scrap prices.

Better discounts favor ferro nickel, NPI over 300 series scrap: Production cost of nickel from ferro nickel and NPI is often cheaper than from scrap in FY25. Due to over supply of NPI from Indonesian market and lower demand from the mills the prices remained subdued during the period.

Rising stainless steel production & consumption: India’s stainless steel production saw an increase of 9% in FY’25 reaching 3.6 mnt from 3.3 mnt in FY’24. Meanwhile, provisionally consumption stood at 4.3 mnt in FY’25, up by 19% y-o-y from 3.5 mnt in FY’24.

India’s stainless steel production, primarily using electric arc furnaces (EAF) and induction furnaces (IF), is heavily dependent on scrap imports, with 85-90% of scrap sourced from abroad. This reliance stems from limited domestic scrap generation, as India has historically had low stainless steel consumption.

With rising demand for stainless steel, imports of semi-finished products and ferro-nickel/NPI have helped fill the gap left by limited scrap availability. However, the increased supply of nickel pig iron and ferro nickel has reduced the dependence on scrap for production.

Declining LME nickel prices: In FY’25, LME nickel prices dropped by 13% y-o-y, settling at $16,000/t, down from $19,360/t in FY’24, driven by a rise in stocks in LME-registered warehouses. Nickel stocks in these warehouses increased by 138%, reaching 1.38 mnt in FY’25, up from 0.58 mnt in FY’24. This surplus contributed to keeping ferro nickel/NPI prices lower and more cost-effective for India.

Country-wise imports

Indonesia, the world’s largest nickel producer, continued to be the leading supplier, exporting 0.2 mnt out of India’s total 0.21 mnt imports in FY’25, accounting for 98% of the total. Furthermore, India’s Free Trade Agreement (FTA) with Indonesia provides a cost advantage, making Indonesian imports more competitive.

Outlook: Looking forward, scrap arrivals are expected to remain limited due to uncertainties surrounding US tariffs and scrap export restrictions from regions like the EU. To compensate for the shortfall in scrap imports, ferro-nickel/NPI imports are likely to remain steady.

Leave a Reply