- Kanto export tender sees 15,000 t booked at $301/t

- Kanto region domestic ferrous scrap tags rise on tight supply

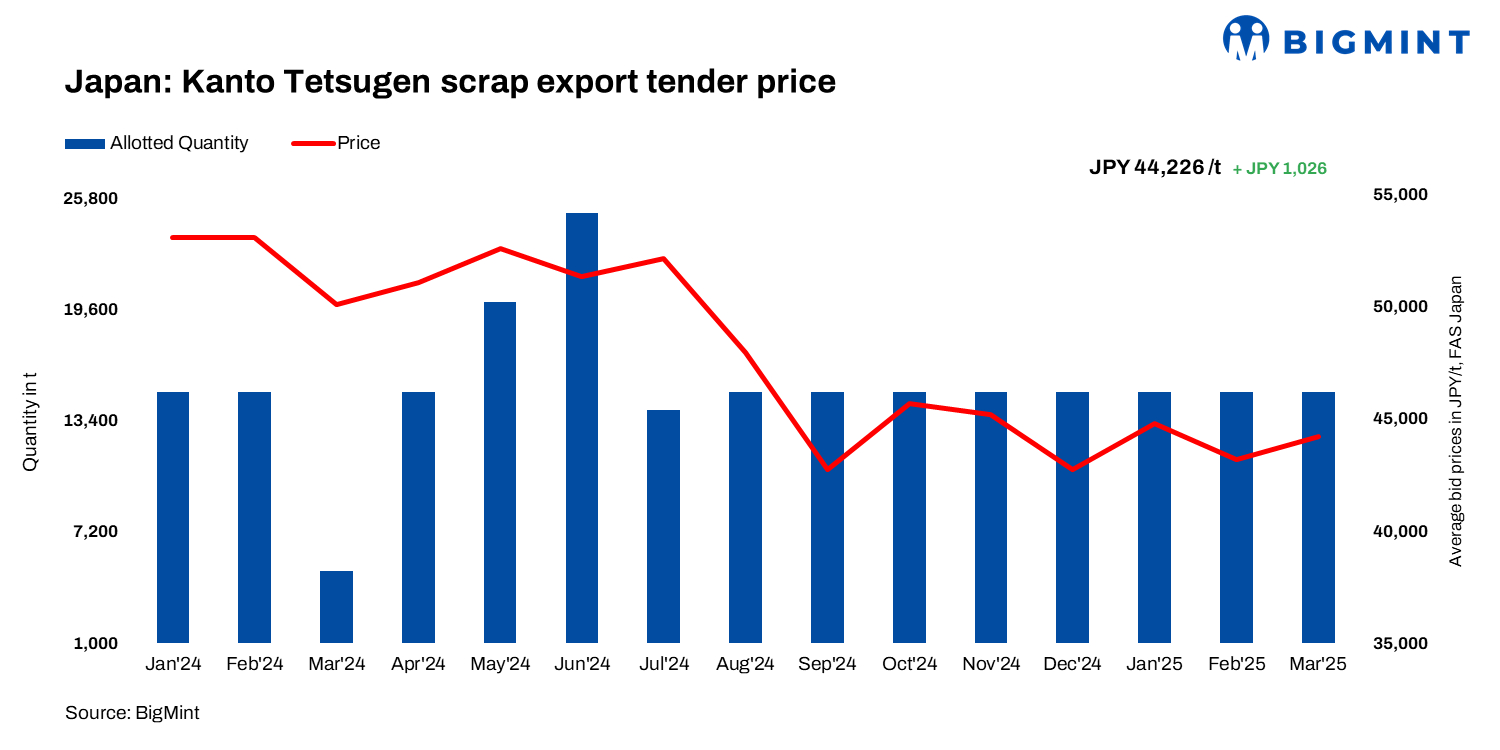

Japan’s March 2025 Kanto scrap export tender saw bids rise by JPY 1,026/t ($7/t) m-o-m, with a Chattogram-based mill securing a 15,000 t H2 lot at JPY 44,226/t ($301/t) FAS.

As per market insiders, a total of 15 trading firms submitted 17 bids, with total bids reaching 138,900 t, up 3,000 t m-o-m. This marked the third consecutive month of bids exceeding 100,000 t and the highest level since October 2021 (148,500 t).

In USD terms, the price rose by a sharper $20/t m-o-m from $281/t FAS in February 2025 to $301/t. The increase in dollar terms was higher because of the JPY’s recent appreciation. CFR Bangladesh prices were assessed at $360-365/t, including freight costs of $60-65/t.

Recently, the sluggish trade momentum for Japanese H2 has been interrupted; this was the first rise in two months, driven by strong demand from Bangladesh and Vietnam, along with higher global scrap prices amid U.S. tariff policy changes.

Only the first bid was accepted due to shipping constraints ahead of Japan’s Golden Week.

Meanwhile, Bangladeshi buyers’ participation in the Kanto export tender remained consistent, with winning bids supported by ease in opening letters of credit (LCs) among major mills.

BigMint’s latest weekly assessment of Japanese H2 stood at JPY 41,700/t ($283/t) FOB Tokyo Bay, which is expected to increase up to JPY 45,000-45,500/t ($305-310/t) following the Kanto tender result.

Kanto ferrous scrap prices rise on tight supply, strong shipments

Ferrous scrap prices in Kanto bay yards have risen recently, supported by steady shipments, tight supply, and increased shipper demand. Gulf H2 scrap prices reached JPY 40,500/t ($275/t), aligning with EAF purchase levels.

The winning bid exceeded initial estimates of JPY 42,500-43,500/t ($289-296/t) and stood nearly JPY 4,000/t ($27/t) above domestic EAF purchase prices of JPY 39,500-40,500/t ($268-275/t).

After dropping to JPY 39,000/t ($209/t) in early February, prices rebounded mid-month following two large shipments (15,000-25,000 t), with weekly shipments totalling 70,000 t. Shortages at dealer yards further supported the uptrend.

High-grade scrap prices remained strong, with HS at JPY 46,500/t ($315/t) and Shinshu at JPY 45,500/t ($308/t), backed by stable Korean demand. EAF mills bought H2 at JPY 39,500-40,500/t ($268-274/t), with most mills maintaining a cautious stance despite some price hikes last week.

Importer market updates

Bangladesh: Mills in Chattogram were relatively slow in bulk inquiries, with small-scale bookings throughout the last few weeks. In the bulk scrap market, Japan’s H2 was offered at $355-360/t, with bids at $350/t, while HS at $385-390/t saw no buyer interest.

Vietnam: Vietnam’s imported scrap prices rose in the last couple of weeks, supported by improved construction sentiment, though buying remained cautious. Japanese H2 scrap was heard at $330-335/t CFR, with tradable levels at around $315-320/t CFR. A 5,000-t H2 deal was concluded at $330/t CFR.

Freights eased slightly due to better vessel availability. Domestic HMS bids remained steady at VND 8,000-9,100/kg.

Construction demand showed slight improvement, with H2 prices supported by government projects in Northern Vietnam. Meanwhile, hot-rolled coil (HRC) buying slowed after February’s surge, with Chinese Q235 HRCs trading at $475/t CFR.

Taiwan: Stronger local rebar demand and firm global scrap prices kept Taiwan’s imported scrap market firm, with Japanese H2 stable w-o-w at $320/t CFR.

Outlook

Japan’s H2 scrap market is likely to stay firm, supported by a stronger JPY and improved demand from Vietnam. The recent Kanto tender saw higher bids, but subdued buying interest in key importing markets could limit gains, keeping prices volatile.

Looking ahead, the next Kanto tender is set for 9 April 2025, will be a key driver. Market participants are also monitoring China’s policies, billet prices, and potential anti-dumping measures.

Leave a Reply