- Iron ore exports up 40% m-o-m in Feb’25 to 2.24 mnt

- Pellet exports rise sharply following price recovery

- Chinese demand outlook subdued, market awaits stimulus

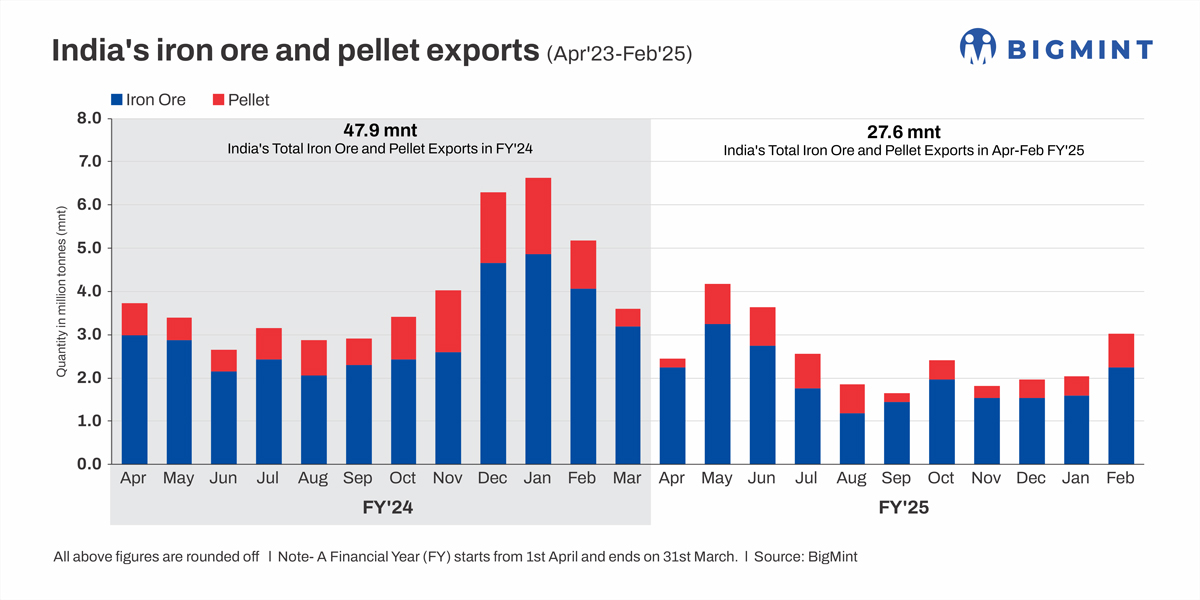

Morning Brief: India’s combined export volumes of iron ore and pellets reached an eight-month high of over 3 million tonnes (mnt) in February 2025, as per latest BigMint data. While iron ore exports increased by over 40% m-o-m to 2.24 mnt in February, exports of pellets rose even more sharply to around 0.79 mnt, according to data. Volumes reached the highest level since June 2024.

The surge in India’s exports of steelmaking raw materials coincides with the marginal improvement in global iron ore prices amid supply disruptions in key producer Australia.

While Rungta Mines was the top shipper, with total volumes at 0.88 mnt in February, the other major exporters were Vedanta, BRPL, KIOCL and AM/NS.

China accounted for over 65% of India’s exports of iron ore and pellets in February at around 1.97 mnt, while shipments to Malaysia, too, increased markedly. China’s share in total exports from India usually stands at over 90%: in 2024 over 92% of total Indian exports went to China.

Factors supporting exports

- Sharp growth in pellet exports: Pellet exports jumped by over 75% m-o-m to reach 0.79 mnt in February as against 0.45 mnt in January. This was due to the resumption in exports, after about a gap of a couple of months, from major producers such as state-owned KIOCL and steel majors, AM/NS and JSP, due to the surge in domestic production as well as recovery in prices. This boosted total export volumes.

- Price recovery propels exports: BigMint’s pellet export index rose from $94/t FOB east coast, India, on 10 January to $105 FOB by end of the month, as per assessment. This was due to the restocking interest among Chinese buyers ahead of the Lunar New Year holidays. Likewise, BigMint’s index for low-grade (Fe 57%) iron ore fines exports climbed up by around 17% m-o-m in February to a monthly average of around $70/t FOB from $60/t in January. This was obviously a direct inducement to suppliers to ratchet up shipments.

- Global prices improve: Global iron ore futures and spot prices recovered from mid-January through to February on expectations of stimulus after the Lunar New Year holidays, as well as tightening of supplies, mainly from Australia, due to cyclonic disruptions. These factors boosted prices.

Outlook

China’s iron ore imports were around 1.24 bnt in CY’24 and projected to rise marginally in CY’25 despite subdued domestic steel demand. Steel exports have edged up by around 7% y-o-y in January and February of this year to over 16 mnt. However, anti-dumping duties and tariffs weigh on export prospects going forward.

Market participants are waiting for positive signs of improvement in the property sector and a stimulus package to shore up domestic demand but the Chinese government has vowed to cut steel production in CY’25 on account of overcapacity in the sector. Australian miners, too, will ramp up shipments in March to make up for the deficit in quarterly volumes.

Against this backdrop, India’s export prospects don’t look too promising. Even in January and February 2025, exports of Indian pellets and iron ore fines to China have dropped sharply y-o-y.

However, looking ahead shifts in the Chinese economy and policies will shape the trajectory of iron ore demand.

Leave a Reply