- Freight rates ease slightly on better vessel availability

- Domestic HMS bids steady in both North and South Vietnam

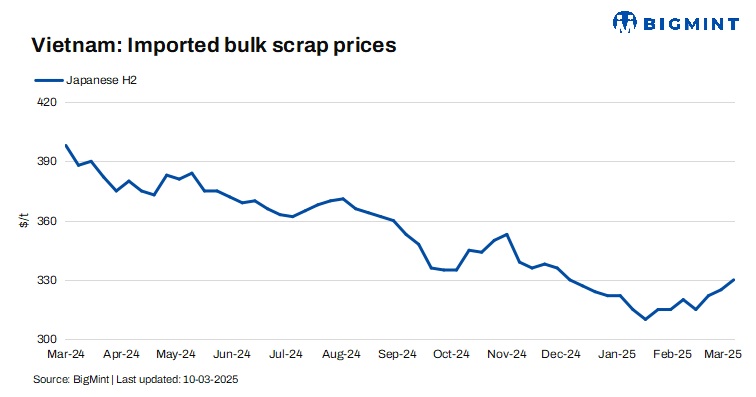

Vietnam’s imported scrap prices rose by $5/t w-o-w, supported by improving construction sentiment, although overall buying activity remained cautious.

Indicative levels for Japanese H2 scrap to Vietnam rose to $330-335/t CFR, while tradable levels were heard around $315-320/t CFR. The bid-offer gap continued to widen, with maximum bids heard at $320/t CFR.

Meanwhile, freight rates for H2 shipments from Japan to Vietnam were heard to have eased slightly, attributed to increased vessel availability.

According to market insiders, a 5,000 t H2 scrap deal was concluded at $330/t CFR Vietnam in the middle of last week.

US-origin deep-sea scrap offers also increased to $360-365/t CFR Vietnam, but buying activity remained subdued.

CFR assessments

- Deep-sea bulk US HMS 80:20 cargoes were assessed at $360/t, up by $5/t w-o-w.

- Japanese-origin H2, a key grade in Vietnam’s scrap market, increased by $5/t to $330/t CFR Vietnam

Market comments

According to a trader, bids for domestic HMS scrap (3-6mm thick) were heard at VND 8,000-8,950/kg (excluding VAT), delivered to mills in the southern region. In the northern region, bid levels were slightly higher, ranging from VND 8,700-9,100/kg ($340-355/t).

HS offers were quoted at $360-365/t CFR Vietnam this week, with workable prices at $358-360/t.

Another trader mentioned that there were slight signs of improved construction steel consumption in Vietnam, noting a modest pickup in demand.

H2 spot prices found support amid growing optimism over government-led construction projects in Northern Vietnam, which have driven up scrap demand.

Recent exchange rate fluctuations have further boosted positive sentiment in the market.

HRC buying slows after February surge

Vietnamese buyers scaled back hot-rolled coil (HRC) bookings this week after purchasing large volumes in late February, estimated at around 150,000 t. Interest in imports remained subdued, though about 10,000 t of Chinese wide HRC (Q235 grade) was sold at $475/t CFR, benefiting from exemption from Vietnam’s temporary anti-dumping duties. With weak domestic demand, the Hoa Phat Group is expected to begin offering HRC for exports next week.

Outlook

Seaborne buyers are likely to adopt a cautious stance in the near term, closely monitoring developments from China’s Two Sessions, potential international anti-dumping measures, and fluctuations in billet prices to gauge market direction.

The industry is keen to gauge future steel consumption trends, raw material demand, and pricing direction, especially for countries like Vietnam that trade heavily with China or are influenced by regional demand flows.

Market participants expect scrap prices in H2 to remain range-bound unless a major rise in finished steel prices is seen, which could drive scrap costs higher.

Leave a Reply