- Trades take a back seat on weak demand

- Auctions fail to receive premium bids

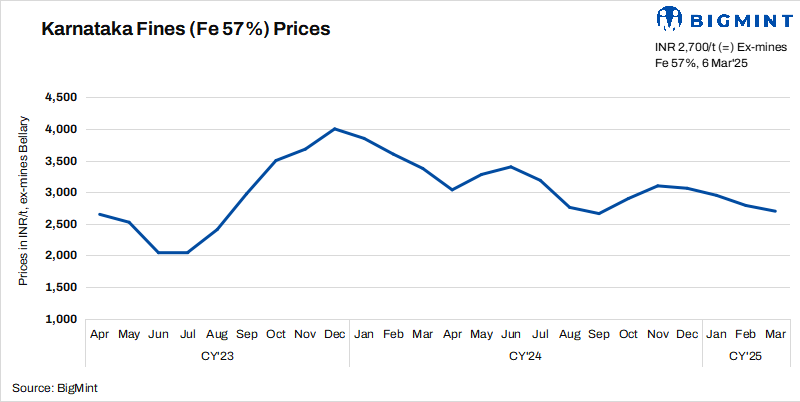

Domestic high grade iron ore fines prices inched down w-o-w. However, the low-grade variant (Fe 57%) remained flat this week in Karnataka’s Bellary region.

BigMint’s weekly index for the same (Fe 57%) stood unchanged w-o-w at INR 2,700/tonne (t) ($31/t) ex-mines Bellary (excluding taxes). However, the Fe 62% fines index dropped w-o-w by INR 100/t ($1/t) to INR 4,800/t ($55/t) ex-mines Bellary, inclusive of taxes. This decline occurred despite a shortage of material in the region, driven by sluggish trading activity amid weak market sentiment in the sponge and steel sectors.

Sources indicate that miners kept prices stable, with no significant changes in offers. Trading activity was subdued, and transactions moderate as miners focused on dispatching older inventory rather than pursuing new sales. This suggests a temporary market slowdown as the fiscal year draws to a close. A source also informed BigMint that low-grade material, mainly Fe57%, is scarce in the merchant market, as miners are not being able to supply that grade.

Meanwhile, NMDC’s recent iron ore auction from its Kumaraswamy mines struggled to secure premium bids, given the current market conditions. The auction witnessed bookings of 180,000 t of fines (Fe 55.63-59.36%) at INR 2,882-3,563/t ($33-41/t) against the base price of INR 2,882-3,543/t ($33-41/t), while 96,000 t of lumps (10-40 mm, Fe 59.79-60.78%) were booked at INR 4,462-4,695/t ($51-54/t) against the base price of INR 4,224/t ($49). Prices are on ex-mines basis, including royalty, DMF & NMET.

Rationale

- Zero (0) trades were recorded in this publishing window, so T1 trade received 0% weightage.

- Eleven (11) offers and indicative prices were reported, out of which eight (8) were considered as T2 trades. Hence, this category was accorded 100% weightage.

Furthermore, one of the major buyers added, “Export sentiments remain weak due to declining global prices impacting the domestic market.” Indian iron ore fines export prices declined by $6-7/t w-o-w due to subdued market sentiments in China and a lack of buyers in the market. Sharp fluctuations in global prices led to fewer inquiries, with exporters awaiting price clarity before making further deals. BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index declined by $4.5/t w-o-w to $62/t FOB east coast, India, on 6 March 2025.

Meanwhile, weak sponge and steel market sentiments have also weighed on domestic market trades, sources informed. BigMint’s daily index for sponge CDRI witnessed a significant drop of INR 300/t ($3/t), w-o-w. Buyers adopted a wait-and-watch approach due to an unstable market, which led to subdued procurement and, consequently, a drop in sponge iron prices.

Karnataka iron ore sales scenario (28 February-6 March 2025)

Outlook

Domestic low-grade iron ore prices are expected to remain volatile in the region, a miner from the region informed BigMint, adding, “Rumours surrounding the potential imposition of anti-dumping levies – whether they will happen or not – are also affecting the steel market, which in turn is influencing the sentiment around iron ore.” Meanwhile, the market is closely watching the developments surrounding the MRT Bill. Trading activity is expected to pick up in the next fiscal year as miners will resume full production following the renewal of their ECs.

Leave a Reply