Prices of Indian domestic stainless steel finished flat and long products remained largely stable w-o-w amid weak demand due to the upcoming Holi festival. Prices were firm despite a rise in London Metal Exchange (LME) nickel prices.

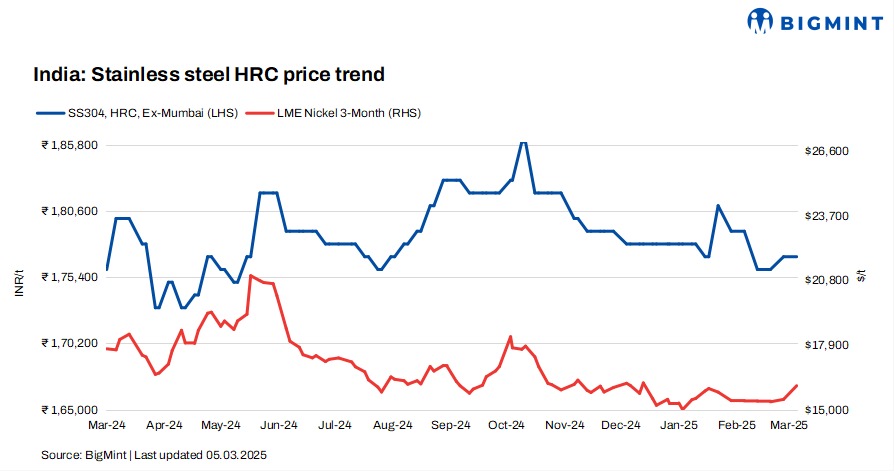

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 177,000/t, stable w-o-w, while 304L (25-100 mm) black round bars remained steady w-o-w at INR 160,000/t, both ex-Mumbai.

LME nickel, Asian NPI rise w-o-w

At the time of reporting, three-month LME nickel prices stood at $16,130/tonne (t), reflecting an increase of 4.3% from last week’s $15,460/t. Nickel stocks in LME-registered warehouses inched up by 2% to 195,360 t compared to 192,642 t in the previous week.

The rise in nickel prices can be attributed to the weakening US dollar and disruptions in Indonesian policies, resulting in tighter mining resources. Additionally, the announcement of US tariffs prevented positive macro sentiments in China. In the short term, nickel prices are expected to remain volatile.

Additionally, Asian nickel pig iron (NPI) prices have been on a steady rise since the start of the year, reaching a year-high of $135.18/t as of today.

Chinese portside prices of NPI (grade 13%>Ni>10%) also witnessed an increase of RMB 18/t ($2/t) w-o-w to RMB 988-990/t ($136-137/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $117/t, up by $2/t w-o-w.

Finished market holds steady w-o-w

As per BigMint’s assessment, SS 316 HRCs remained stable w-o-w at INR 321,000-322,000/t ex-Mumbai.

As per market participants, “Currently, the demand for finished steel is low, but the market has already hit the bottom, so we do not expect a significant decline in finished steel prices in the near future. While market conditions may be subdued for now, the likelihood of a substantial price drop seems unlikely.”

BigMint’s assessment of SS 316L (25-100 mm) black round bars stood at INR 269,000-271,000/t ex-Mumbai. Prices of SS 316L (25-100 mm) bright bars stood at INR 287,000-289,000/t ex-Mumbai, stable w-o-w.

Chinese stainless steel prices rise

In China, domestic stainless steel prices of 304-grade cold-rolled coils (CRCs) stood at RMB 13,850/t ($1,907/t) exw, up by RMB 150/t ($20/t) w-o-w, while FOB prices of 304-grade CRCs were at $1,890/t.

On the demand side, the possibility of an upward momentum in the stainless steel spot market remains weak. However, as stainless steel mills gradually resume operations after the holiday, production is expected to rise, driving optimism for high-grade NPI. Additionally, the recent increase in stainless steel scrap prices has reduced its competitiveness compared to high-grade NPI from a cost-effectiveness perspective.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices remained range-bound w-o-w as compared to the previous assessment.

As per BigMint’s assessment on 5 March, ferro molybdenum prices in India were at INR 2,637,000/t ($30,290/t) exw on a 60% pro rata basis.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,100/t ($1,149/t) exw-Jajpur, range-bound as compared to previous week.

Additionally, China’s Tsingshan kept its ferro chrome tender price stable m-o-m at RMB 6,995/t ($960/t) DAP, including taxes for March 2025. This was below Chinese spot prices (Cr:50%) of RMB 7,350/t ($1,009/t) ex-Inner Mongolia.

Outlook

In the near term, market activity is expected to remain subdued due to the upcoming Holi festival. Moving forward, market participants are not expecting any significant price drop in finished steel.

Leave a Reply