- Supply shortages support higher tags

- Mill’s list prices expected to increase

Trade-level hot-rolled coil (HRC) prices across India increased by up to INR 1,600/tonne (t) w-o-w to INR 48,100-50,500/t. Additionally, cold-rolled coil (CRC) prices rose by up to INR 1,000/t w-o-w, settling at INR 54,200-58,300/t ($617-671/t) across markets. The price hike was driven primarily by material shortages and speculation regarding the imminent imposition of a safeguard duty.

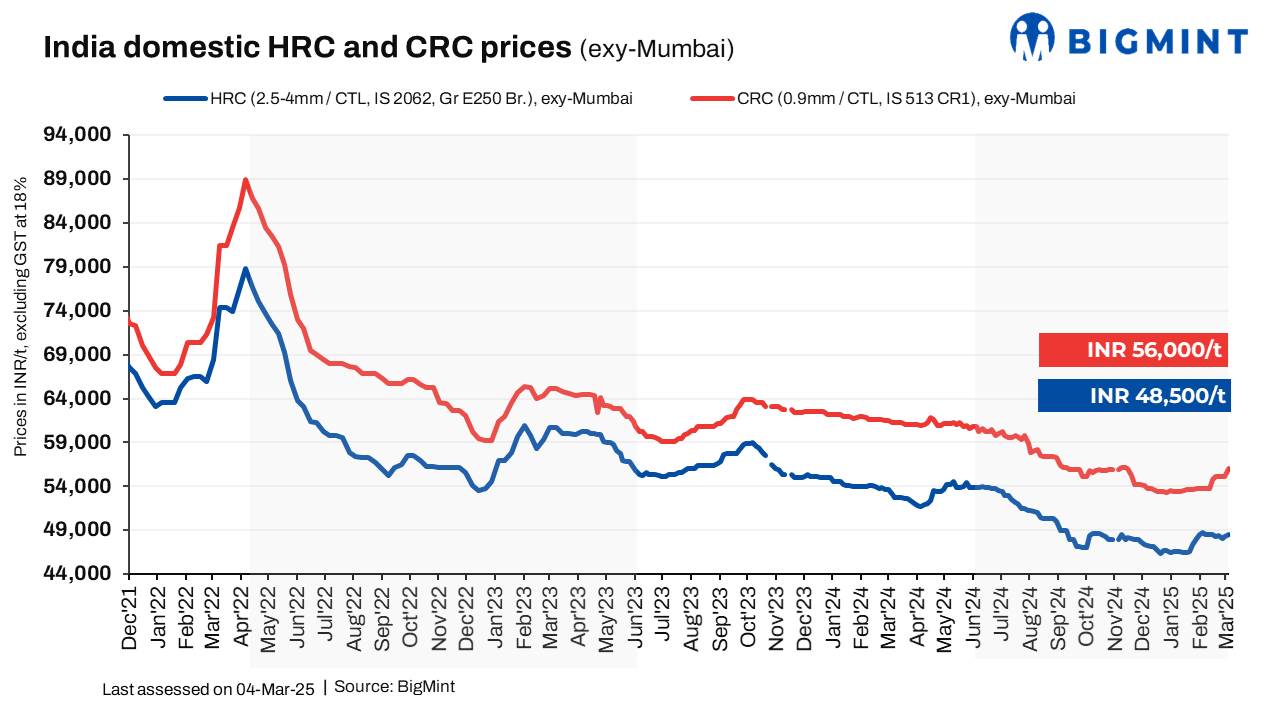

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) increased by INR 200/t w-o-w to INR 48,500/t ($549/t) on 4 March 2025. Meanwhile, CRC (IS513, Gr O, 0.9 mm/CTL) prices surged by INR 900/t w-o-w to INR 56,000/t ($628/t). These prices are quoted ex-Mumbai for the distributor-to-dealer segment and exclude the 18% GST.

Market updates

Mills planning to raise list prices: Certain mills will reportedly raise list prices by INR 1,500/t, indicates market speculation, although this was not officially confirmed. Parallelly, the provision of price support for the prior month has reportedly been discontinued.

However, these potential price hikes were placed on hold as the week progressed, as mills awaited clarification regarding the imposition of safeguard duties. Market participants believe that the implementation of such duties could lead to list price increases in the range of INR 2,000-3,000/t.

Supply shortages push up trade prices: While trade prices surged amid market speculation surrounding the potential imposition of safeguard duties, supply shortages in certain regions further propelled prices upward.

“Material shortages and speculation regarding safeguard duty implementation have contributed to recent price surges. However, underlying demand remains weak, raising concerns about the sustainability of these increases. The market’s direction will be significantly influenced by developments in the coming week,” said a market participant.

Import trends: India’s bulk imports of HRCs and plates touched 413,020 t in February 2025, according to vessel line-up data from BigMint. As of 3 March, imports stood at 59,358 t this month, with an additional 81,604 t expected to arrive later.

Export trends: BigMint’s India HRC (SAE 1006) export index for the Middle East and Vietnam declined by $10/t w-o-w to $495/t FOB east coast India, compared to $505/t last week. Recent export deals to the Middle East indicate a slight improvement in demand in the region. Meanwhile, European demand was subdued due to weak market sentiment and ongoing anti-dumping investigations.

Outlook

List price hikes by mills are expected soon, contingent on safeguard duty confirmation. The higher HRC and CRC prices may also remain supported due to supply constraints. While imports are expected to continue at comparatively high levels, export demand will vary regionally. Future market direction hinges on duty implementation and demand sustainability.

Leave a Reply