- Finished steel edges up on reports of output cuts

- Silico rises 5% amid rising manganese ore tags, export inquiries

- Imports restrictions on met coke keep PHCC prices firm

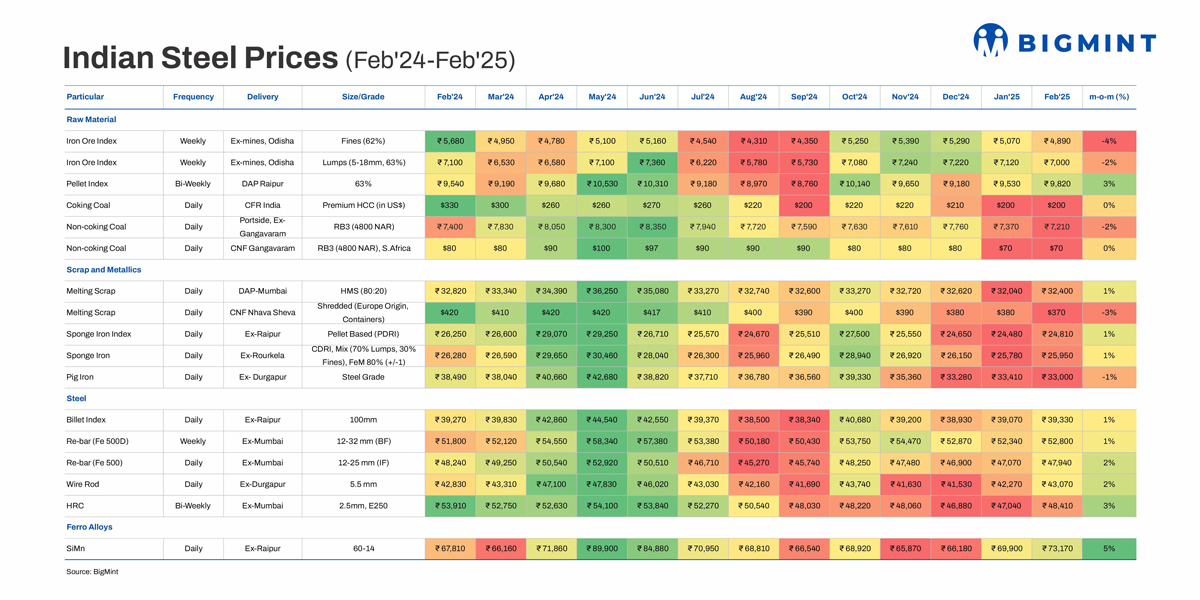

Morning Brief: Domestic steel and raw material prices showed mixed trends m-o-m in February 2025, but most adjustments were minimal.

A number of factors led to range-bound prices last month. First, the market had been looking forward to the Union Budget, but it fell short of expectations, dampening sentiment. Second, the much-anticipated safeguard duty failed to materialise this month, and the announcement of 25% tariffs on US steel imports left the market in a tizzy.

The finished steel segment also witnessed lacklustre prices, although they rallied in the latter half of the month, as speculation surrounding production cuts and declining import pressure intensified. This ultimately led to improved tags towards the month-end and prevented a larger decline overall.

M-o-m, iron ore fines and lumps witnessed slight corrections, coal prices remained depressed, and the scrap and metallics segment was weak, too. However, steel logged slight hikes, and silico manganese climbed up the highest, by 5% m-o-m. Pellets were also up by 3% m-o-m.

Factors impacting domestic steel, raw material prices

Coal

Monthly average prices of Australian coking coal held firm m-o-m, while those of domestic non-coking coal edged down. However, South African non-coking coal was stable.

- Premium hard coking coal (PHCC): In February, PHCC was assessed at $200/tonne (t) CFR, largely unchanged from January. Despite weak steel prices and met coke price cuts in China, Australian PHCC offers were supported by (1) weather-related disruptions such as Cyclone Zelia, which hit Australia in mid-February; (2) extended shipping times from alternative sources such as the US; and (3) lower import activity for met coke, following the imposition of quantitative restrictions.

- Non-coking coal: Indexed portside ex-Gangavaram prices of RB3 (4800 NAR) stood at INR 7,210/t in February, a one-year low, compared to INR 7,370/t in January, reflecting a minor dip of 2%. High portside inventories, amid regular auctions by CIL subsidiaries, pressured tags. Weak sponge iron prices also dampened bids for thermal coal.

Prices of the same variant from South Africa were steady m-o-m at $70/t CNF Gangavaram, though there was weak demand for imported material and limited trades.

Ferro alloys

Silico manganese: The silico manganese index (60:14 grade) for Raipur increased 5% m-o-m to INR 73,170/t in February from INR 69,900/t in the previous month.

First, raw material prices increased. India’s imported manganese ore prices edged up by about $0.5/dry metric tonne unit (dmtu) m-o-m in February, driven by reduced supply from major global miners following a reduction in their production. MOIL’s February offers followed suit, with a 3.5% increase for higher grades and 8.2% for lower ones. Other factors included (1) production cuts amid rising input costs; (2) soaring inquiries from overseas; (3) and limited material offered by key smelters.

Scrap & metallics

Prices in this segment were stable m-o-m, adjusting by 1% for all except imported shredded scrap, which fell by 3%.

- Sponge iron: Prices of sponge iron (pellet-based), ex-Raipur, moved up by 1% to INR 24,810/t in February from INR 24,480/t in January. Sponge CDRI mix climbed up by the same percentage to INR 25,950/t from INR 25,780/t in the previous month.

Sponge iron prices edged up alongside a slight improvement in demand in the induction furnace (IF) rebar market. However, subdued demand overall limited further price gains.

- Pig iron: Offers were firm m-o-m, down by 1% to INR 33,000/t ex-Durgapur in February from INR 33,410/t in January.

Amid weak demand for finished steel, producers maintained their offers due to steady raw material costs, such as of met coke.

- Melting scrap: HMS (80:20) prices climbed up by 1% to INR 32,400/t DAP Mumbai in February from January’s INR 32,040/t but declined INR 50-200/t in other regions. While prices were under pressure during the initial half of the month, trade momentum picked up as steel demand improved in the latter half.

- Imported scrap: European-origin containerised shredded scrap dipped by 3% m-o-m at $370/t CNF Nhava Sheva in February against $380/t in January. Subdued steel demand, a depreciating rupee, and rising freights kept prices under pressure. Moreover, bid-offer mismatches led to limited bookings, and mills turned to more cost-effective domestic scrap. Additionally, US scrap suppliers also focused on their domestic market, limiting its availability in India.

Iron ore

Iron ore prices recorded mixed movements: fines and lumps were down, while pellet tags increased.

- Fines, lumps: In February, iron ore fines (Fe 62%) were down by 4% m-o-m at INR 4,890/t ex-mines Odisha from INR 5,070/t in January.

Overall, prices faced pressure due to limited trades and weak demand. While they picked up in the second half, driven by tight availability of higher-grade material and a rise in OMC premiums, these factors were not able to offset the overall m-o-m downtrend. Some miners’ environmental clearance (EC) extraction limits also approached expiry, which supported offers.

Meanwhile, lumps (Fe 63%) witnessed a 2% drop m-o-m to settle at INR 7,000/t ex-mines Odisha against INR 7,120/t in January.

- Pellets: Prices (Fe 63%) moved up by 3% to INR 9,820/t DAP Raipur in February from INR 9,530/t in January.

Raipur’s pellet offers were bolstered by rising prices in Odisha and active export deals in the Indian Ocean region. Additionally, improving sponge iron and billet prices towards the second half of the month lifted pellet prices.

Steel

Prices trended up across the board, but the changes were mostly minor. HRCs witnessed the highest uptick of 3% m-o-m.

- Billets: Prices were largely firm m-o-m at INR 39,330/t in February, up by 1% compared to INR 38,070/t ex-Raipur in January. Trading activity picked up in the middle of the month, amid improved momentum in the finished longs segment.

- Rebars, wire rods: Prices of blast furnace (BF) grade rebars inched up by 1% to INR 52,800/t ex-Mumbai in February from INR 52,340/t in January.

February initially saw subdued transaction volumes amid need-based procurement. However, production shortages, amid speculation regarding maintenance shutdowns by mills, allowed suppliers to lift prices. The project segment, in particular, saw a rise in sales, and rebar stocks meant for the trade channel had to be diverted to projects.

Meanwhile, induction furnace (IF) rebar prices climbed up by a higher 2% m-o-m to INR 47,940/t ex-Mumbai against INR 47,070/t in January.

Prices increased as trade improved. Stable raw material and semi-finished prices also lent support.

Additionally, wire rods (ex-Durgapur) rose by 2% to INR 42,270/t in February from INR 41,530/t in January.

- HRCs: Prices of hot-rolled coils (HRCs) ex-Mumbai saw a 3% rise to INR 48,410/t in February from INR 47,040/t in January.

Prices were boosted by the following factors: First, Tier-1 mills raised list prices of HRCs by INR 1,500-2,000/t for February against end-January levels. Secondly, the import pressure on the market reduced amid a continued downtrend in India’s HRC imports. Thirdly, supply tightened, with a number of leadings steelmakers opting for maintenance shutdowns this month. However, there are concerns over whether the supply situation is truly as severe as it seems.

Outlook

The uptrend in the finished steel segment is expected to continue. First, supply will remain tight amid maintenance shutdowns by mills, although demand might not strengthen substantially. HRC and rebar shortages will continue; even the CRC segment has been facing limited availability.

Second, rumours abound that the long-awaited safeguard duty might be imposed any day now. As a result, mills are planning to raise list prices for March, though official confirmation is awaited. Some rebar producers have signalled a robust hike, of INR 1,500-2,000/t, for March list prices, and expectations are that mills may elevate tags a few more times throughout the month. Trade-level BF rebar prices might increase by INR 1,000-1,500/t in the near term.

Additionally, with the end of the financial year approaching, trade might accelerate. For instance, rebar sales for projects have shot up, as construction firms are in a race against time to complete their work.

As a result, steel prices may be on the higher side. The bullish sentiment will likely percolate down to the raw material segments.

Leave a Reply