- Exporters turn cautious as bid-offer gap widens

- Domestic prices remain higher by INR 1,550/t ($18/t)

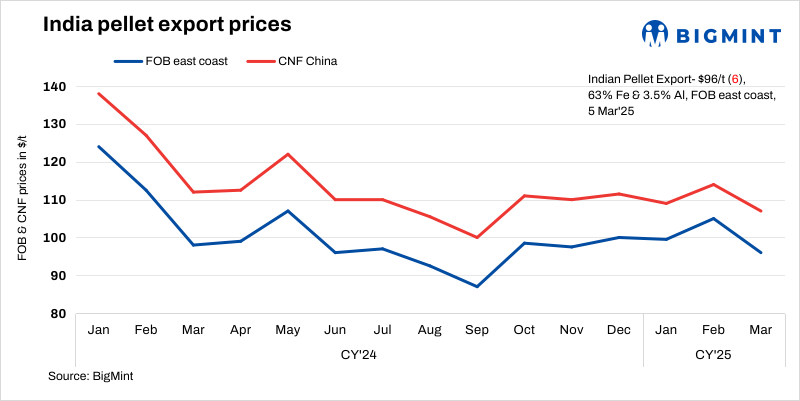

Indian pellet export prices dropped by $6-7/t over the past week due to weak market sentiment and poor macroeconomic indicators from China. The decline in global fines indices further pressured pellet prices in the overseas market. Accordingly, BigMint’s pellet export index also dropped w-o-w, to its lowest level in over a month, last seen in mid-January 2025.

BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) decreased by $6/tonne (t) w-o-w to $96/t on 5 March 2025. Moreover, the index dropped by $4/t against the previous assessment on 28 February. No trades were recorded this week from the east coast; however, a leading exporter concluded a deal for 60,000 t last week.

This week, an export tender for pellets with lower alumina content witnessed a positive response; however, bids dropped by $4/t compared to last week’s tender. An Indian pellet maker concluded an export deal for around 50,000 t of this grade (Fe 63%, 2% AL2O3) at $102-103/t FOB India yesterday, sources informed BigMint.

A pellet producer stated, “We have taken a cautious stance amid widening bid-offer gaps and are refraining from trades due to market volatility. Uncertainty in the Chinese steel market is keeping buyers on the sidelines.”

Currently, there is a bid-offer gap of around $5-8/t, and buyers are reluctant to match offers, resulting in muted trade activity from the east coast. A leading export trading firm stated, “The price gap is too wide, and buyers are not willing to negotiate at current levels. Buyers are searching for deals of $105/t CFR, which is unlikely possible from the seller’s end.”

China’s cautious outlook was influenced by the start of one of its major meetings on Tuesday, while the National People’s Congress will convene on 5 March to discuss essential economic policies.

Adding to the pressure, rumours of a possible steel production cut in China, to the tune of 50 million tonnes (mnt), dampened sentiment. Market participants are closely watching China’s Two Sessions meeting this week for policy direction. “If there is no positive signal from the meeting, we might see further weakness in pellet export demand,” commented a trader.

Meanwhile, the domestic pellet market remained stable, leading to a wider gap between export and domestic realisations. This price difference further deterred exports.

Domestic prices exceeded export offers by INR 1,550/t ($18/t) w-o-w as compared to INR 1,100/t ($12/t) last week. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,000/t ($92/t) exw, down INR 50/t ($0.5/t) w-o-w. Meanwhile, ex-plant realisation in exports from Barbil stood at INR 6,450/t ($74/t) exw.

Rationale

- No confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was not taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for the detailed methodology.

- Eleven (11) indicative prices were received, and eight (8) were considered for calculation of the index and given 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices drop w-o-w: The benchmark iron ore fines index declined by $5/t w-o-w to $102/t CFR China on 4 March. Demand for seaborne raw materials improved after the previous price fall, though it remained modest overall due to significant production cuts in Tangshan, announced for 4-12 March.

- DCE iron ore futures fall w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract fell by RMB 41/t ($6/t) w-o-w to RMB 771/t ($106/t) on 5 March. On a d-o-d basis, futures dropped by RMB 10/t ($1/t).

Outlook

As per BigMint’s analysis, if the Two Sessions meeting fails to bring any favourable developments, the pellet export market is expected to remain subdued, with limited trade activity in the coming weeks.

Leave a Reply