- Indian buyers cautious amid wide bid-offer gap

- Bangladeshi buyers show interest pre-Ramadan

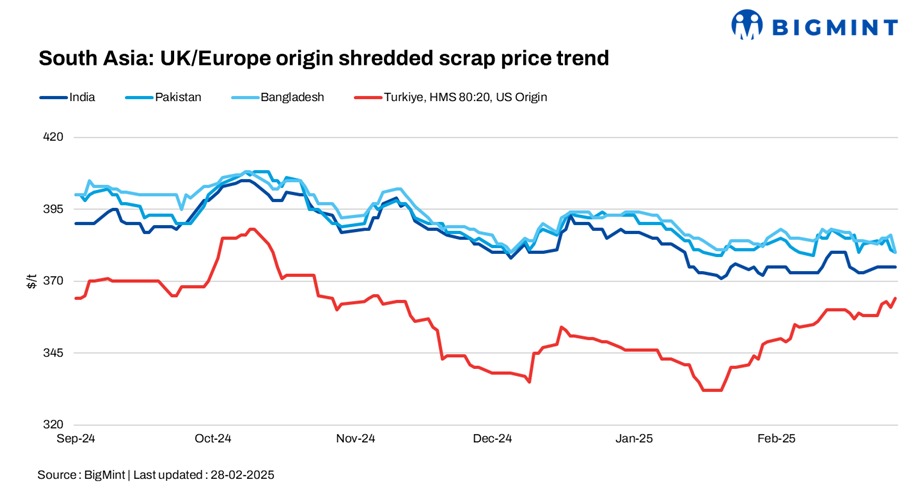

The South Asian imported scrap markets showed mixed trends, with India and Pakistan facing sluggish demand due to liquidity constraints and weak steel sales, while Bangladesh saw a slight improvement in buying interest ahead of Ramadan.

In India, a widening bid-offer gap and currency devaluation kept buyers cautious amid rising Turkish scrap prices. Pakistan’s market remained slow, as mills avoided high-priced offers, keeping bids lower. Meanwhile, Bangladeshi buyers focused on competitive deals, and overall sentiment stayed cautious.

Shredded offers remained unchanged d-o-d in India and edged down by $1/t in Pakistan and $5/t in Bangladesh.

In contrast, Turkiye’s scrap market saw firming prices, as mills continued restocking, but weak rebar demand limited further upside. US bulk HMS (80:20) offers to Turkiye inched up by $4/t d-o-d.

Overview

India: India’s imported scrap market remained slow due to weak demand, liquidity constraints, and a widening bid-offer gap. No firm offers emerged from the US, while UK/European shredded was heard at $375-380/t CFR Nhava Sheva, with bids lower at $365-370/t CFR. HMS (80:20) offers stood at $350-355/t CFR.

Despite improved rebar demand and rising Turkish scrap prices, buyers rejected higher offers due to sufficient availability of domestic material and currency devaluation.

Pakistan: Pakistan’s imported scrap market remained sluggish, as weak liquidity and subdued steel demand kept buyers cautious ahead of Ramadan. Mills were reluctant to accept high offers and kept bids low.

UK/European shredded offers stood at $380-385/t CFR Qasim, but buying interest was limited, with workable levels falling to around $375/t CFR.

Bangladesh: Bangladesh’s imported scrap market showed improved procurement interest ahead of Ramadan, with more buyers returning after a prolonged lull. However, price negotiations remained cautious, with mills favouring competitive offers from Australia and ASEAN countries. Bulk scrap activity remained muted due to a wide bid-offer gap, while containerised material saw selective purchases at lower levels. Weak steel demand and ongoing project delays kept overall sentiment cautious, though some traders anticipated a short-term uptick in bookings.

Australian shredded offers stood at $380/t CFR Chattogram, Hong Kong PNS and UK-origin shredded at $375/t CFR, and Malaysian Busheling at $385/t CFR.

Turkiye: The Turkish imported scrap market strengthened, as mills continued restocking despite sluggish rebar sales. Offers for US-origin bulk HMS (80:20) climbed up to $364/t CFR, with EU-origin deals at $359/t CFR and US/Baltic offers at $360-365/t CFR. Sellers remained firm, anticipating further strength in the US domestic market.

However, mills hesitated on higher prices due to weak rebar demand, keeping the scrap-to-rebar spread tight at $196/t. While traders expect scrap prices to rise further, uncertainties in Turkish steel and global scrap trends will shape market movements in early March.

Price assessments

India: UK-origin shredded indicatives were assessed stable d-o-d at $375/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives edged down by $1/t d-o-d to $385/t CFR Qasim.

Bangladesh: UK-origin shredded indicatives dropped by $6/t d-o-d to $380/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $364/t CFR Turkiye, up by $3/t d-o-d.

Leave a Reply