- Slowing price gains, output cuts push up inventories

- Market awaits demand pick-up in Mar amid uncertainty

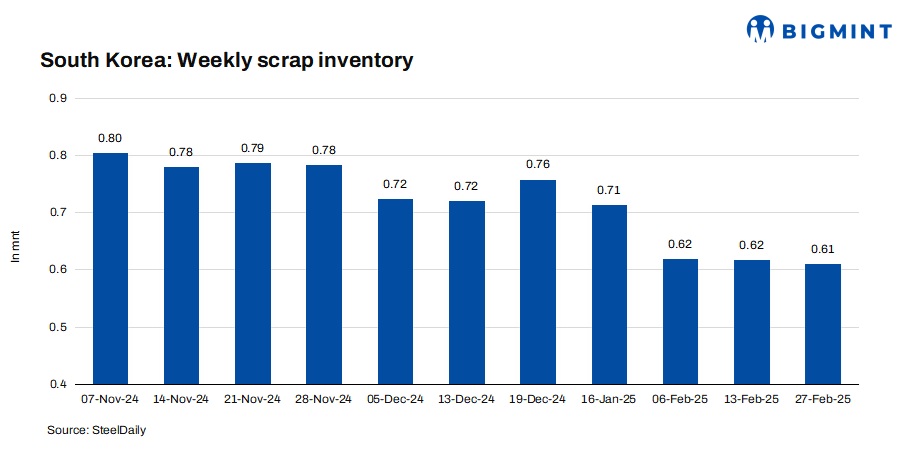

SteelDaily: The combined ferrous scrap inventory of eight major South Korean steel mills rose by 0.4% w-o-w to 611,000 t.

Domestic steelmakers’ inventory increased for the first time in about two months, likely due to slowing price gains and production cuts at the end of the month.

Inventory in the central region trended downward, while the south saw a slight increase.

Region-wise inventory

Central region: The central region’s steel scrap inventory declined by approximately 3.9% from the previous week, to 259,000 t.

Hyundai Steel’s Incheon plant saw a 12.5% decline in inventory. Meanwhile, Dongkuk Steel’s inventory increased by 5%, Hwanyang Steel’s levels decreased by 25% w-o-w, while stocks at Hyundai Steel’s Dangjin plant remained relatively stable.

Hyundai Steel’s Incheon plant reduced scrap steel consumption this week, as rebar production declined, resulting in a significant drop in inventory.

Southern region: The southern region’s steel scrap inventory rose by approximately 3.8% from the previous week, to 352,000 t.

POSCO’s inventory increased by 18% w-o-w, while Hyundai Steel’s Pohang plant saw a 10% decline. Meanwhile, the combined inventory of Korea Iron and Steel, Daehan Steel, and YK Steel remained unchanged w-o-w.

Korea Special Steel’s inventory rose 16% w-o-w. Dongkuk Steel’s Pohang plant is expected to see an inventory increase following the recent resumption of steel scrap imports.

With scrap iron inventory rising at the end of February, the industry is now looking ahead to the peak season in March. Typically, March marks a high-demand period for the steel sector, with increased production of rebar and section steel driving higher scrap iron consumption.

Market update

This year’s scrap supply and demand dynamics remain complex. If the current steel market downtrend persists and demand recovery in March falls short of expectations, scrap prices are likely to fluctuate within a limited range.

A market participant stated, “The market’s direction will depend on whether the recent inventory build-up is temporary or part of a production ramp-up ahead of the peak season. While an increase from February is expected, it ultimately hinges on steelmakers’ production plans and a potential demand rebound from construction.”

Note: This article has been written in accordance with a content exchange agreement between SteelDaily and BigMint.

Leave a Reply