- Chattogram dominates, but supply dips

- Alang & Gadani struggle amid weak sentiment

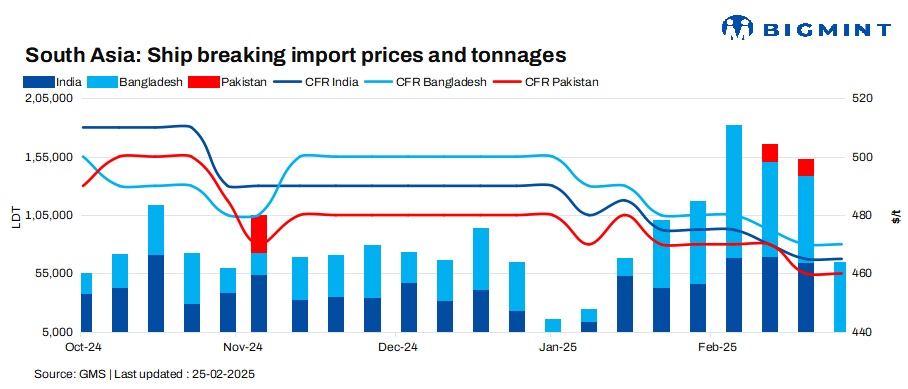

South Asia’s ship-breaking markets saw mixed conditions prevailing this week. Chattogram maintained its dominance with steady prices and strong inflows, though tightening supply may pose challenges ahead. Alang struggled with weak sentiment, a depreciating currency, and falling steel prices, while Gadani remained stagnant, hindered by pricing constraints and economic instability. Overall, uncertainty looms amid fluctuating fundamentals.

Alang struggles as steel slumps, rupee weakens

Alang recyclers continue to struggle as market volatility, currency depreciation, and weakening steel fundamentals impact the sector. With only one vessel arriving at anchorage, including a reportedly sanctioned tanker, awaiting clearance, supply remains tight. The depreciating Rupee has further strained buying sentiment, while steel plate prices have fallen nearly $15/LDT over three weeks.

The introduction of steep US tariffs on Chinese steel has added uncertainty, keeping recyclers cautious at bidding tables. While Alang remains competitive, its ability to secure tonnage consistently has weakened. With declining offers since the start of the year and tightening vessel supply, recyclers face growing challenges in sourcing tonnage at viable prices.

According to a participant, “The ship recycling market remains stagnant this week, with no vessels available for scrapping and limited local support.”

Recent deals:

A oil tanker China built of 13,000 t has been booked for recycling at $440/LDT reported.

Current offers:

- Bulkers: $420-425/LDT

- Tankers: $435-440/LDT

- Containers: $460-465/LDT

Despite the urgency among buyers, activity remains limited as sellers hold out for better pricing.

Pakistan struggles amid pricing constraints

In week 8, Gadani recyclers remained on the sidelines as pricing constraints and limited capacity hindered their ability to secure tonnage. Despite the Pakistani Rupee maintaining stability against USD and steel plate prices holding firm at $644/t, the highest in the region, buying interest remained weak.

Broader economic concerns persist, with the IMF downgrading Pakistan’s 2025 outlook due to financial mismanagement. With the HKC compliance deadline looming in July, non-compliant yards face further restrictions.

Frustration at the bidding tables is growing, and recyclers may soon be forced to raise offers to stay competitive. However, for now, Gadani remains on the backfoot with no clear recovery in sight.

In week 8, no tonnage was reported at Gadani Port compared to the previous week’s 5,204 LDT.

Bangladesh holds firm, maintains dominance

Chattogram recyclers remained active, securing over 52,000 LDT across seven vessels. Recycled ship steel prices held steady at $529/t, marking one of the longest periods of stability since October 2024. However, stalled infrastructure projects continue to limit long-term demand.

Currency volatility persists, with the Bangladeshi Taka briefly weakening. While remittance inflows offer some relief, economic uncertainty and weak reforms continue to pressure local industries.

The delayed progress on HKC compliance remains a challenge. With the BSBRA extending the deadline to 31 March 2025, further delays could weaken Bangladesh’s position against competitors like India. For now, Chattogram remains dominant, though tightening vessel supply may slow activity going ahead.

In week 8, Chattogram Port received 52,434 LDT, down from 74,268 LDT in the previous week.

Leave a Reply