Domestic induction furnace finished long steel offers followed mixed trends. Prices varied in the range of INR 50-700/t. Trade reference prices for hot rolled coil (HRC) and cold rolled coil (CRC) fell by upto INR 300/t this week.

Iron ore and pellet

- OMC conducted the auction for 2.617 mnt of iron ore (1.098 mnt of lumps and 1.519 mnt of fines) on 19 February. Entire 100% of lumps (Fe 58-64%) were booked at INR 4,950-8,000/t with a premium of INR 300-1,400/t over the base prices. Buyers actively responded to the auction, which offered a higher volume compared to last month. Around 1.423 mnt (94%) iron ore fines (Fe 55-65%) was booked at INR 3,150-5,250/t ex-mines. The bids fetched a premium of INR 50-450/t for a few lots against the set base price. The miner increased base prices by INR 200-300/t and INR 150/t m-o-m for fines and lumps, respectively. For Fe55% fines, base prices were raised by INR 850/t.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) remained stable w-o-w at $104.5/tonne (t) on 19 February. An eastern India-based exporter sold 75,000 t (Fe62%) at $115.5/t CFR China. A domestic pellet maker concluded an export deal for around 50,000 t of pellets (Fe 63%, 2% AL2O3) at $108-109/t FOB India.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index remained largely stable w-o-w at $69/t FOB east coast, India, on 20 February 2025. However, prices rose by $2/t against the previous assessment on 17 February. Odisha-based miners sold around 110,000 t of iron ore fines (Fe 57%) at $80/t CFR China recently. In other deals, 75,000 t of fines (Fe57%) were recorded at $67/t FOB concluded a couple of days back. A few more deals a under negotiation.

Coal

- Portside South African thermal coal prices fall: RB2 (5500 NAR) dropped by INR 150/t to INR 8,500/t exw-Gangavaram, while RB3 (4800 NAR) declined by INR 50/t to INR 7,150/t amid weak demand and rising domestic coal availability.

- India’s domestic met coke prices show mixed trends: 25-90 mm BF-grade coke remained stable at INR 34,000/t exw-Jajpur, while Gandhidham prices dropped by INR 800/t to INR 31,200/t amid limited trade and ongoing import restrictions.

- Thermal coal inventories at Indian ports declined significantly in week 7 of CY’25, registering an 8.6% drop to 12.58 million tonnes (mnt) from 13.76 mnt recorded in the previous week, hitting a nearly 3-month low.

Ferro Scrap

- India’s imported scrap market remained subdued as ample domestic availability, weak steel demand, and currency fluctuations kept buyers cautious. Shredded scrap offers from the UK/Europe fell to $375-380/t CFR Nhava Sheva, while HMS (80:20) ranged between $345-355/t CFR, with minimal trades.

- Traders expect limited recovery unless global prices stabilize or local demand improves, with potential movement post-March.

- Market sentiment remained bearish, with bid-offer mismatches and weak finished steel demand limiting activity. Premium scrap supply was tight, while buyers awaited clarity on US tariffs set for 12 March. Sellers held firm, but buyers pushed for lower prices.

- Around 4,500-5,000 t of scrap were booked, including 3,000-3,500 t of HMS (80:20) from Latin America, Mozambique, Australia, West Indies, and Madagascar at $350-375/t. Additionally, 1,000-1,200 t of Blue steel scrap from Brazil and the UK traded at $385-392/t, while 500-600 t of Bundle scrap from Yemen was secured at $310/t.

Ferro Alloys

- Silico Manganese:Indian silico manganese prices were largely steady w-o-w with slight drop by INR 300/t ($3/t) w-o-w to INR 72,600-74,000/t ($838-854/t) in key regions of Durgapur, Raipur and Vizag. The slight fluctuation in the price was due to the need-based purchases amid slow movement in the steel market w-o-w.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices emained unaltered w-o-w and stood at INR 76,000/t ($877/t) exw in Durgapur. Meanwhie, prices exw-Raipur also remained unchaged at INR 76,000/t ($877/t). The stability in the prices was majorly because of the steady market operations and muted export demand.

- Ferro Silicon:Indian ferro silicon prices declined by INR 500/t ($6/t) w-o-w to INR 100,900/t ($1,164/t) exw-Guwahati. Prices also diminished by INR 500/t ($6 /t) in Bhutan to INR 101,100/t ($1,167/t) exw. Prices fell as need-based buying was seen in the market and no significant impact was observed due to the closure of Meghalaya-based plants.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices rose by INR 2,500/t ($29/t) w-o-w on tight supplies to INR 100,700/t ($1,162/t) exw-Jajpur. Most market participants were in a wait-and-watch mode ahead of the chrome ore auction from the Odisha Mining Corporation (OMC). Hence, sellers offered a limited volume in the market.

- At OMC’s ferro chrome auction on 19 Feb’25, only three lots were sold at the base price. The bigger lot of high-carbon ferro chrome (Cr:60-64%, 10-100 mm) was sold at the base price of INR 95,700/t exw and high-carbon low-silicon (Cr:60-63%, 10-100 mm), too, went at the base price of INR 102,500/t exw.

Semi-Finished

- Indian semi-finished steel prices showed mixed as per BigMint’s assessment. Domestic billet prices in almost all key locations decreased by INR 50-700/t across regions, with a major decrease of INR 700/t seen in the Goa market. While, other regions showed slight up INR 100-200/t ex. However, sponge iron prices also showed mixed trend, almost all key locations decreased by INR 100-450/t, with a major decrease of INR 450/t seen in the Bellary market. While Durgapur and Mandi Gobindgarh market moved up by INR 100-200/t

-

Indian DRI (Direct Reduced Iron) export offers decreased by $3 for CPT Raxaul, stood at $340/t while, CPT Benapole offers increased by $4 stood at $342/t.

-

SAIL-Bokaro Steel Plant (BSL) held an auction for 17,500 t of steel-grade pig iron on 19 Feb’25. The total volume was booked at an average price of INR 30,700/t exw. In the previous auction on 1 Jan’25, 14,000 t of steel-grade pig iron – the entire quantity on offer – were sold at an average price of INR 31,350/t exw.

Finished Long Steel

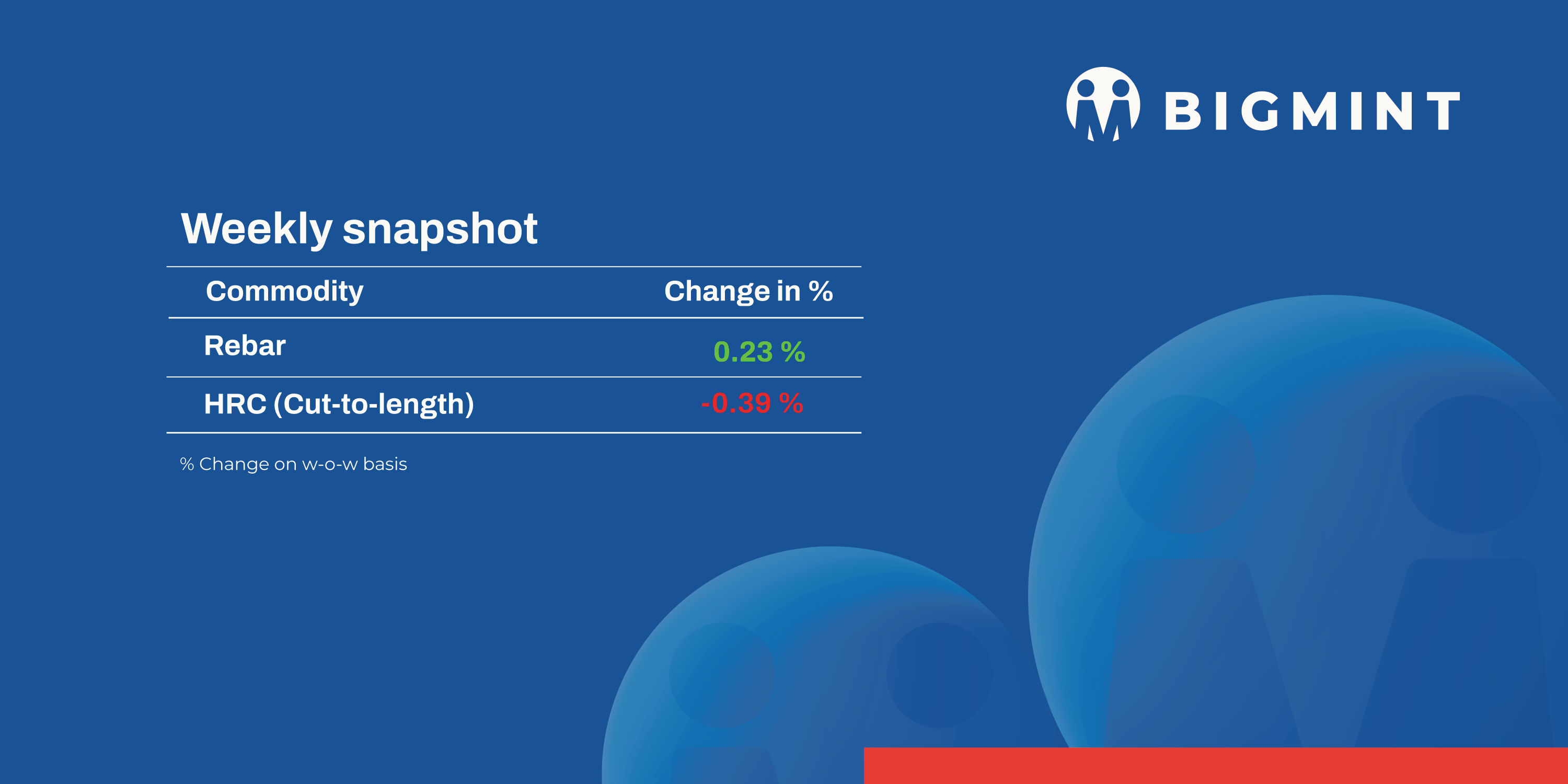

- IF-rebar:India’s induction furnace route finished long steel prices showed mixed trend amid limited trading activity. Buying remained need-based throughout the week due to market uncertainty. Manufacturers maintained stable prices or offered trade-level discounts based on orders. Smooth dispatches of previously booked materials have reduced mill inventories to around 8-10 days. Market participants expect prices to remain range-bound in the near term.

- On a weekly basis, in rebar steel prices witnessed variation in the range of INR 100-700/t across the regions as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 42,500-42,900/t exw Raipur, INR 46,800-47,400/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 44,000-44,500/t exw Raipur.

-

Trade reference prices of wire rod hovering at INR 43,000-43,600/t ex Raipur.

- BF-rebar:Trade-level blast furnace (BF) rebar prices remained range-bound w-o-w across markets owing to dull demand & limited material availability. Current week’s rebar prices (12-32mm) in the trade segment edged down w-o-w by INR 100/t to INR 52,600/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the project segment, prices ranged within INR 50,000-51,000/t FOR Mumbai. Buyers were cautious in placing orders which resulted in need basis demand.

Flat Steel

- Hot-rolled coil (HRC) prices across India decline marginally by upto INR 300/tonne (t) w-o-w at INR 47,300-49,700/t. Conversely, cold-rolled coil (CRC) prices witnessed mixed trends w-o-w, settling at INR 52,600-56,000/t ($617-671/t) across markets.

- The market is currently experiencing a downturn, characterized by reduced sales volumes and a shift towards need-based, minimal-quantity purchasing. Additionally, there are reports of planned maintenance shutdowns at Tata Steel’s Kalinganagar, Meramandali, and Jamshedpur plants, with the Jamshedpur facility expected to undergo an extended maintenance period.

- Imports of bulk HRCs and plates stood at 3,08,819 t till 17 February, as per vessel line-up data maintained with BigMint. It is expected that an additional 64,535 t will be imported by the month-end and 75,900t in first week of March.

- Reports indicate that deals have been finalized for 2,000 MT of HRC at $530 CFR Chennai and 30,000 MT at $485-$490 CFR Mumbai.

- BigMint’s India hot-rolled coil (HRC, SAE1006) export index for the Middle East (ME) and Vietnam remained stable w-o-w. However, export offers to Europe declined w-o-w due to ongoing anti-dumping probes.

Leave a Reply