- Muted demand weighs on traders’ market

- Market awaits mills’ list prices for Mar’25

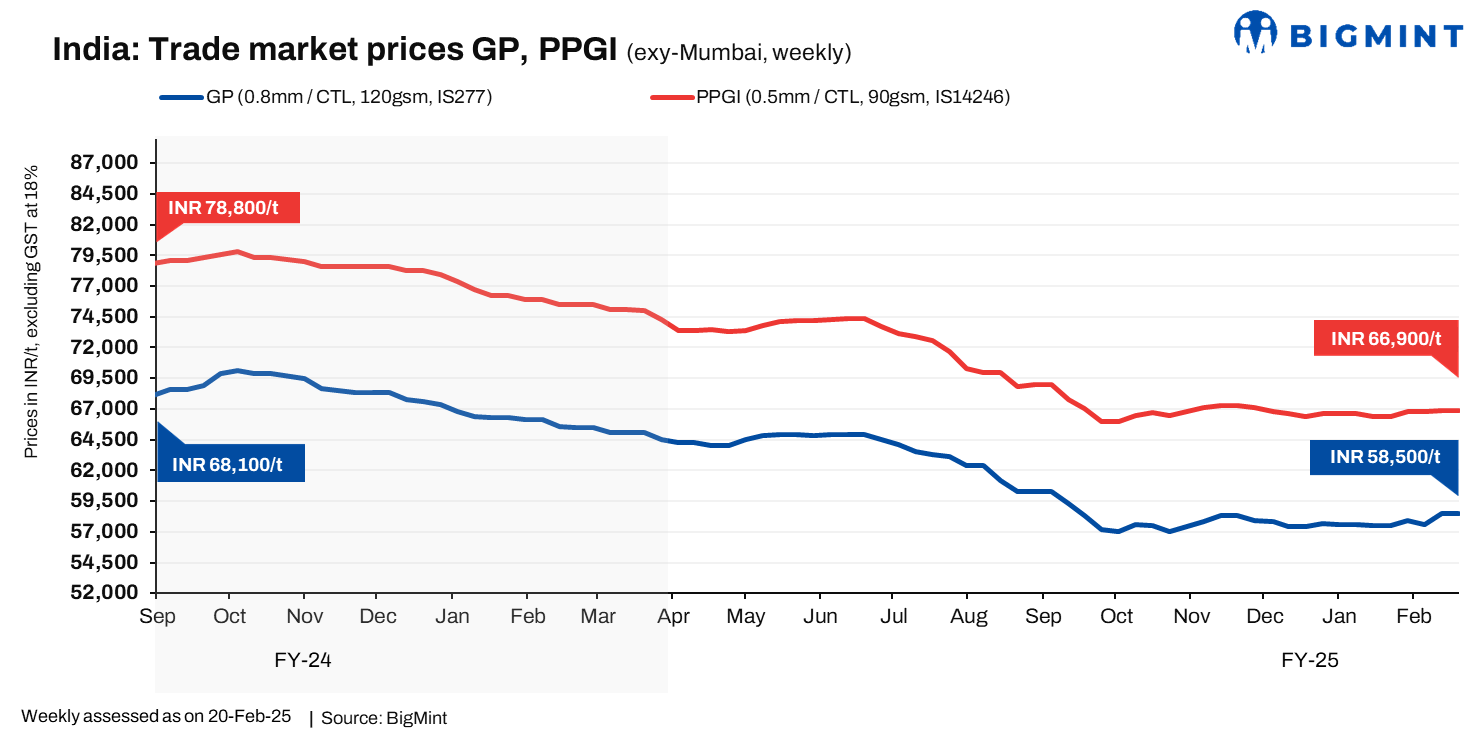

Trade-level coated flat steel prices remained range-bound this week after rising in the preceding one. The spike in demand in the last fortnight was short-lived, though it provided a platform for an increase in prices earlier this month.

The latest weekly assessment placed galvanised plain (GP, 0.8 mm/CTL, 120 gsm, IS277) steel prices at INR 58,500/t ($676/t) exy-Mumbai, with offers varying in the range of INR 58,000-59,000/t ($671-682/t). Similarly, pre-painted galvanised iron (PPGI, 0.5 mm/CTL, 90 gsm, IS14246) was assessed at INR 66,900/t ($773/t) exy-Mumbai, with offers at INR 66,000-67,500/t ($763-780/t). The prices are minus GST at 18% (USD 1 = INR 86.5017; INR 1 = USD 0.0115605).

Market updates

Subdued demand keeps trade market depressed: Trade market participants were left disappointed this week, as demand softened, leading to largely stable prices.

In fact, throughout FY’25 (April 2024-February 2025), buying appetite in the traders’ market has been weak. While distributors were granted a little respite when mills raised list prices, which helped lift offers in the trade market, this occurred only for short durations in the current fiscal year.

The average trade level price hovered at around INR 64,600/t ($768/t) in Q1FY’25, which fell to INR 61,200/t ($708/t) in Q2 and dropped again to INR 57,600/t ($666/t) in Q3. Meanwhile, in the two months of Q4 (January-February), this stands at around INR 57,900/t ($/669t), slightly higher than the preceding quarter. The prices mentioned are on an exy-Mumbai basis, excluding GST at 18%.

“Demand in the traders’ market was sluggish this fiscal year. The only support mills received was from their business-to-consumer (B2C) sales and the pre-determined MoU-based quantity lifted by distributors,” said a distributor source based in western India. “Improved production and supplies, alongside low-volume procurement by end-users in the traders’ market, has kept prices under pressure,” he added.

Additionally, the average monthly price in February 2025 stood at around INR 58,200/t ($673/t), up from the previous month’s INR 57,600/t ($666/t). This increase was followed by the price hike announced by mills for February 2025 sales earlier this month.

Manufacturing index shows signs of improvement: India’s Manufacturing Purchasing Managers’ Index (PMI) improved to 57.7 percentage points in January 2025, up by 1.3 percentage points against the previous month, as per S&P Global data. Driven mostly by the industrial end-user segment’s buying appetite, it relays a positive note that demand has improved m-o-m. The positive trend comes mostly from improved sales in the B2C segment this fiscal year.

Outlook

Trade-level tags are likely to move in a narrow band in the near term, with market participants awaiting mills’ list price announcements for March 2025. Inventory pile-ups in the distribution channel are expected to remain a concern in the near term, as distributors lift their residual MoU quantities for FY’25.

Leave a Reply