- Pak, Bangla buyers cautious, see minimal trade

- Turkiye mills push prices lower, sellers hold firm

South Asia’s imported scrap market remained largely subdued as weak domestic steel demand, currency fluctuations, and Ramadan-driven slowdown kept buyers cautious. In India, ample domestic supply and sluggish steel sales limited interest in fresh imports, while Pakistan’s mills stayed on the sidelines due to weak liquidity and delayed government payments.

Bangladesh saw minimal trade as sufficient mill inventories and a lack of infrastructure projects dampened sentiment.

Meanwhile, in Turkiye, mills pushed for lower prices amid weak finished steel demand, but sellers held firm.

Overview

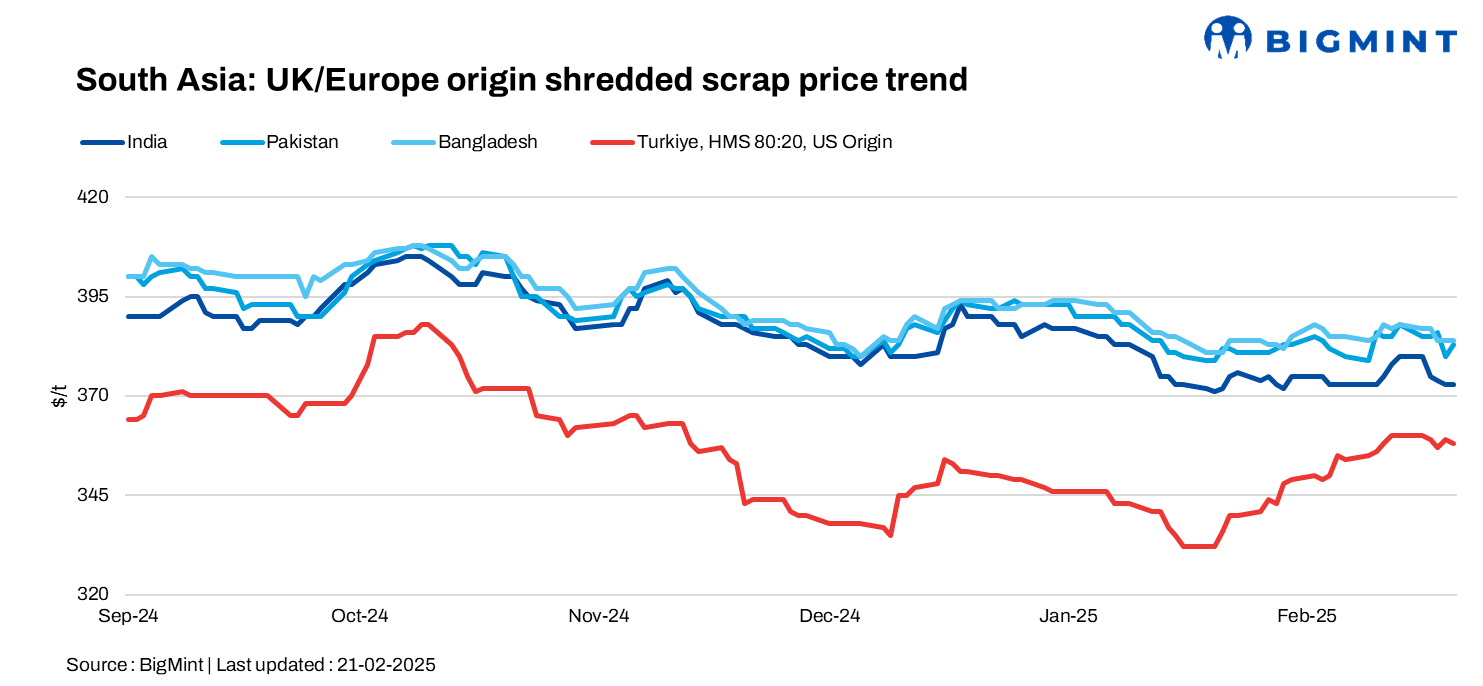

India: India’s imported scrap market remained muted as adequate domestic supplies, weak steel sales, and currency fluctuations deterred buyers. Shredded scrap from the UK/Europe was offered at $375-380/t CFR Nhava Sheva, with bids lagging at $370-375/t CFR, while HMS (80:20) from West Africa and Europe stood at a lower $345-355/t CFR.

Sellers held firm, but buyers pushed for lower prices amid sluggish demand. Market sentiment remained bearish, with traders expecting limited recovery unless global prices correct or local steel demand picks up. Some expect movement post-March, influenced by potential changes in US tariffs affecting global trade flows.

Pakistan: Pakistan’s imported scrap market remained sluggish as buyers stayed on the sidelines ahead of Ramadan, with weak liquidity and slow domestic steel demand limiting activity. Shredded scrap offers from the UK/Europe stood at $385-390/t CFR Qasim, while bids remained lower at $378-382/t CFR, leading to minimal trade. Domestic rebar sales struggled due to delayed government payments and cash flow constraints, further dampening sentiment.

A trader noted, “Shredded scrap offers reached $385‑392/t CFR, but deals were mostly concluded at $380‑385/t CFR,” reflecting cautious buying and a wait-and-see approach by mills.

Bangladesh: Bangladesh’s imported scrap market remained sluggish as weak domestic steel demand and ample mill inventories limited buying interest. With Ramadan approaching, traders adopted a wait-and-see approach, leading to fewer bookings.

Hong Kong PNS was offered at $385-390/t CFR, while Brazilian HMS 80:20 hovered around $365/t CFR.

Some containerised trades occurred for Singapore-origin PNS at $382-385/t CFR, but overall sentiment stayed cautious. The absence of new government infrastructure projects and slow liquidity further pressured demand, keeping scrap purchases subdued.

Turkiye: The Turkish imported scrap market saw slight price declines as mills pushed for lower levels amid weak finished steel demand and competitive billet prices. Despite this, sellers largely held firm.

A Baltic-origin HMS 80:20 deal at $358/t CFR set the tone, with market sentiment remaining cautious.

European recyclers struggled with margins due to high collection costs, while Turkish mills preferred European and Baltic cargoes over costly US shipments. With mills aiming to cut costs and billet prices influencing decisions, scrap demand remained steady but lacked momentum, keeping the market in a wait-and-see mode.

A trader noted, “We booked only six deep-sea cargoes in two weeks, down from 11 earlier in February.”

Price assessments

India: UK-origin shredded indicatives edged down by $1/t d-o-d to $373/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives increased by $3/t d-o-d to $383/t CFR Qasim.

Bangladesh: UK-origin shredded was assessed stable d-o-d at $384/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $358/t CFR Turkiye, down by $1/t d-o-d.

Leave a Reply