- Bangladesh, Vietnam see mild price gains

- Slight rise in freight further pressure US sellers

US ferrous scrap export offers fell by $2/t w-o-w as high import costs for scrap and billet, along with weak rebar demand, kept Turkish steel mills cautious, limiting US deep-sea scrap exports to the region this week.

Current US East Coast offers for HMS 80:20 were heard at $362-365/t CFR Turkiye, and US West Coast offers to Bangladesh and Vietnam stood at $365-370/t and $352-358/t CFR Chattogram and CFR Hai Phong respectively.

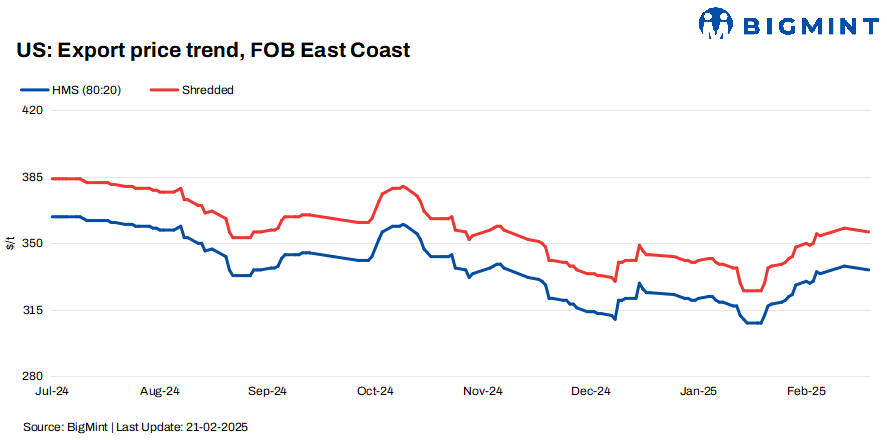

FOB assessments (US East Coast, bulk)

- Shredded fell by $2/t w-o-w to $356/t.

- HMS (80:20) decreased by $2/t w-o-w to $336/t.

CFR assessments (bulk)

- HMS (80:20) was at $358/t CFR Turkiye, down $2/t w-o-w.

- HMS (80:20) stood at $350/t CFR Vietnam, up by $5/t w-o-w.

- HMS (80:20) was at $363/t CFR Chattogram, up w-o-w.

US monthly domestic scrap index

The RMDAS ferrous scrap index in the US saw a notable rise in February 2025, reflecting stronger spot market prices for steel mills and foundries. Shredded scrap climbed by $44/t to $437/t, while prompt industrial composite scrap saw the biggest jump, rising $50/t to $466/t. HMS also gained $30/t, reaching $385/t.

Market updates on key importers

Turkiye: Demand for US-origin ferrous scrap in Turkiye remained subdued as high import costs and weak rebar demand continued to weigh on buying activity.

Market participants indicated workable prices for US and Baltic-origin HMS (80:20) between $355-360/t CFR, though US sellers held firm at a minimum target of $360/t CFR.

A modest increase in freight costs from the US East Coast to Turkiye, rising to $30/t from $29/t in the previous week, put further strain on US exporters. Turkish mills, facing pressure from weak finished steel demand and rising input costs, remained cautious about securing US-origin cargoes, exploring more competitive alternatives from Europe and the Baltic region.

Bangladesh: Demand for US-origin ferrous scrap in Bangladesh showed slight improvement, though overall market activity remained limited.

US HMS 80:20 bulk prices edged up by $3/t w-o-w to $363/t, with offers ranging between $365-370/t CFR. Some buyers have re-entered the market, signalling a modest pick-up in demand. However, LC issuance remains a persistent challenge, albeit with some improvement compared to previous months.

A steel mill official noted that while local scrap prices are steady, mills are keeping rebar offers elevated, supported by stable but comparatively slow regional demand. Despite this, buyers are proceeding cautiously amid financial constraints and subdued construction activity.

Vietnam: Demand for US-origin ferrous scrap remained weak, although there was a $5/t increase in prices last week, reflecting the slow recovery of construction activity post-holidays.

Deep-sea bulk US HMS (80:20) cargoes were assessed at $350/t CFR, up by $5/t w-o-w, while offers for US-origin deep-sea cargoes climbed to $360/t CFR. However, sluggish demand kept buying interest limited, with mills proceeding cautiously amid uncertain market conditions.

Outlook

US exporters remain actively engaged in negotiations, driven by expectations of a further price increase in the domestic ferrous trade for March, following consecutive gains in January and February. While Turkish mills are expected to continue steady scrap restocking for March/April shipments, demand for US-origin material may remain limited unless prices become more favourable for buyers in Turkiye.

Leave a Reply