Japan’s H2 scrap offers edged up slightly on the week owing to multiple factors, including exchange rate fluctuations, higher seaborne offers, and supply constraints at Japanese ports. A slight improvement in Vietnam’s construction activity supported demand, while Japanese shippers focused on fulfilling previous contracts, leading to tighter availability. However, some buyers remained cautious about rising prices, preferring to wait and see. While short supply kept prices firm, the outlook remained mixed, with concerns over global trade policies and competition from US suppliers attempting to push up prices.

Tokyo Steel has revised its scrap procurement prices for the second time this month, effective 21 February, 2025. While prices remained unchanged at most plants, the Kansai plant saw an increase of JPY 1,000/t ($7/t). Following the adjustment, H2 scrap prices stood at JPY 42,000/t ($279/t) for Okayama, Kyushu, and Kansai, JPY 40,500/t ($269/t) for Tahara, JPY 40,000/t ($266/t) for Utsunomiya, JPY 39,500/t ($262/t) for Takamatsu, and JPY 39,000/t ($259/t) for Nagoya.

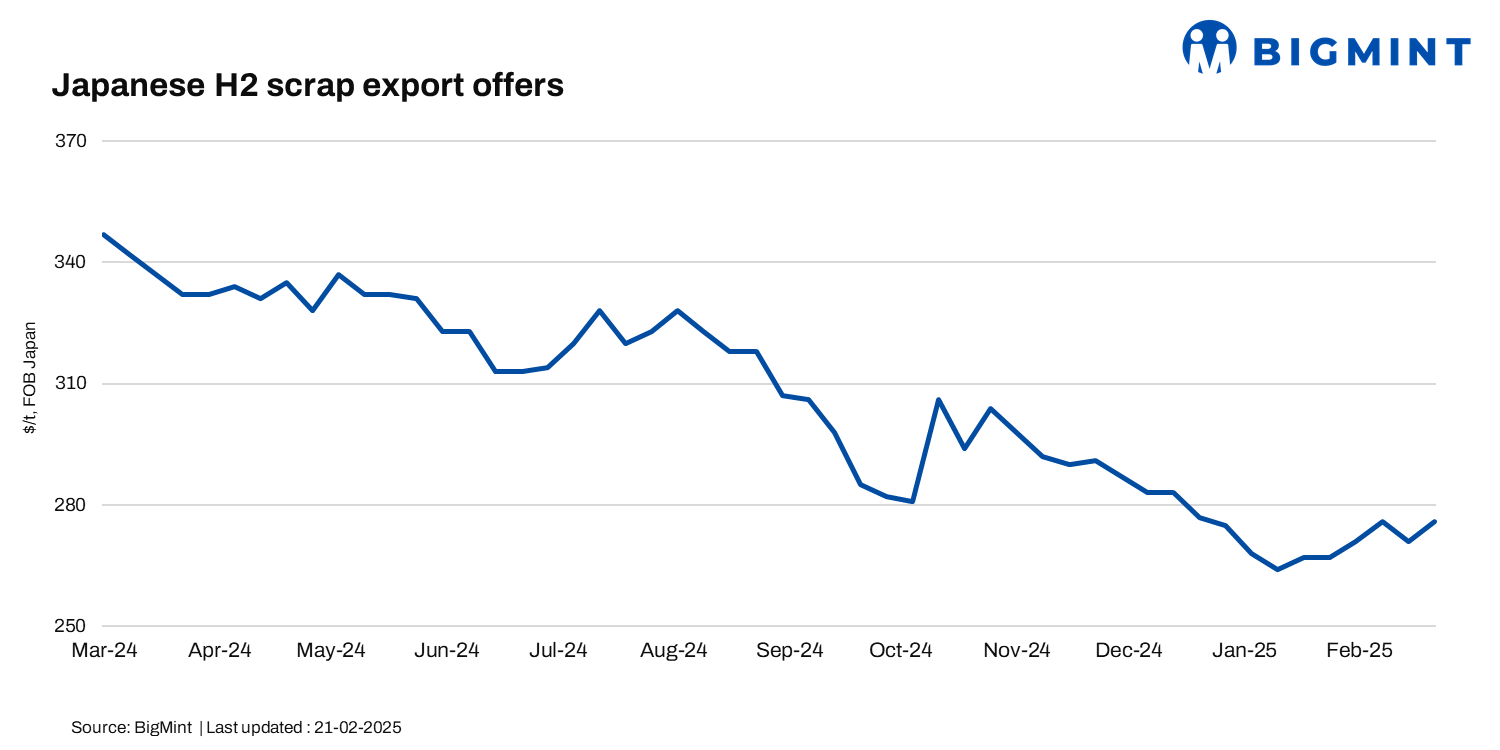

BigMint’s latest assessment showed a slight increase of JPY 100/t ($0.66/t), bringing Japanese H2 scrap export prices to JPY 41,500/t ($276/t) FOB Tokyo Bay from JPY 41,400/t ($275/t) last week.

Updates of other markets

Vietnam: Vietnam’s imported scrap market saw an uptrend as Japanese H2 offers rose to $320-$322/t CFR Vietnam, driven by port congestion and supply tightness. US deepsea offers, however, trended lower at $355-$360/t CFR, while Australian-origin offers dropped to $350-$355/t CFR.

Improved construction activity in Vietnam supported demand, but buyers remained cautious about matching higher prices. Market participants are closely watching trade policies, China’s economic direction, and steel demand recovery to gauge future price trends.

South Korea: South Korea’s imported scrap market remained weak as buyers held back amid bearish sentiment. No confirmed deepsea offers emerged, though indicative US-origin offers hovered at $345-350/t CFR.

Japanese H2 scrap stayed firm due to port congestion and tight supply, but Korean mills showed little buying interest. A struggling construction sector and rebar production cuts further dampened demand, prompting some suppliers to shift focus to Vietnam.

Imported ferrous scrap volumes at major South Korean ports dropped to 79,432 t in mid-February, down 20,000 t w-o-w, though most of this volume is expected to be unloaded starting this weekend.

Taiwan: Taiwan’s imported scrap market maintained an upward trend as US-origin HMS 80:20 scrap reached $313/t CFR, marking a third consecutive weekly increase, while Japanese H2 scrap rose to $320/t CFR. Higher global scrap prices pushed mini-mills like Feng Hsin Steel to raise rebar list prices by TWD 200/t, reflecting increased production costs. Strong rebar sales last week further supported price hikes, driven by end-user replenishments. However, weak finished steel prices in China, where post-holiday demand remained sluggish, created a mixed outlook, with mills closely monitoring regional market trends.

Outlook

Japan’s ferrous scrap prices are expected to remain firm in the near term, supported by tight supply, port congestion, and steady domestic demand. However, upside potential may be limited as some buyers, especially in key importing markets like South Korea and Vietnam, are showing resistance to higher prices. Additionally, competition from US and deepsea suppliers could cap further gains. Exchange rate fluctuations and global trade policies will play a crucial role in determining price movements. While short supply provides near-term support, a clearer trend will emerge based on demand from key steel-producing nations and economic conditions in China.

Leave a Reply