- Crude steel production to grow over 5% y-o-y in FY’25

- Sponge iron capacity to touch 70 mnt by FY’30

- DRI exports by India may reach 1.4 mnt in FY’25

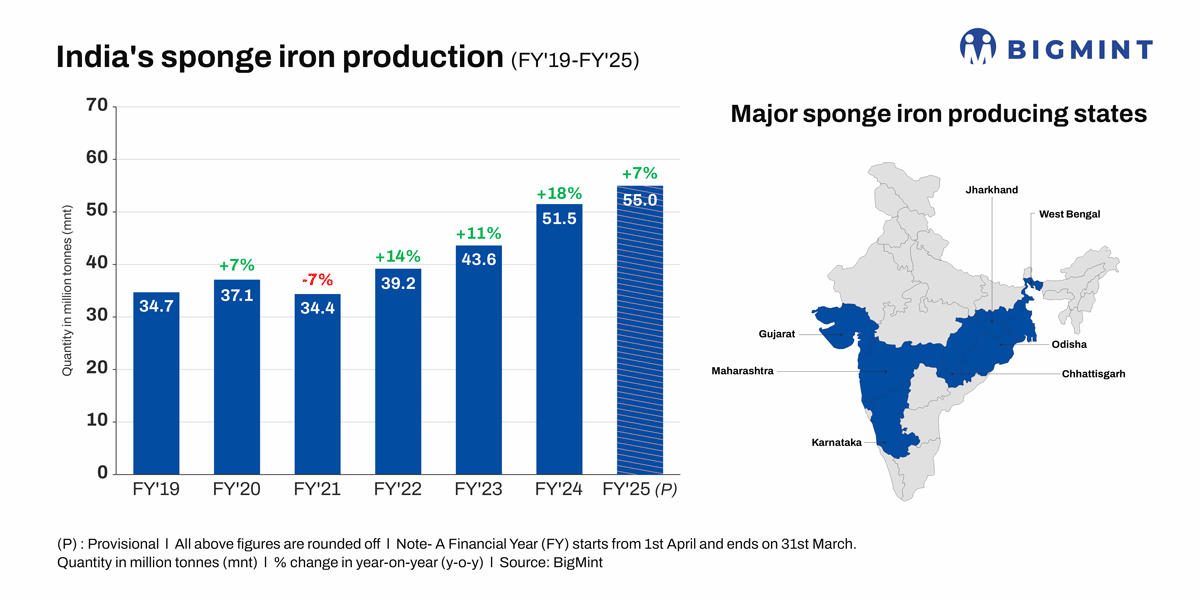

Morning Brief: In the fiscal year 2024-25 (FY’25), India’s sponge iron production is expected to reach approximately 55 million metric tonnes (mnt), with India maintaining its position as the world’s largest producer of sponge iron.

This production level reflects a compound annual growth rate (CAGR) of 8% since FY’19 when output was 34.7 mnt. This growth has been primarily driven by the small and mid-sized enterprises, which have contributed 71% of the total production, while large players accounted for the remaining 29%.

Factors fuelling sponge iron production

Infrastructure development & steel demand: The Indian government’s focus on infrastructure projects and rapid industrialisation has increased the demand for steel, subsequently boosting sponge iron production.

Surge in steel production: India’s crude steel production rose by approximately 14% in FY’24, reaching 144 mnt, up from 127 mnt in the previous year. This surge was largely due to increased production through the induction furnace route, which relies heavily on sponge iron as a raw material. Crude steel production in FY’25 is expected to increase by over 5% y-o-y to 152 mnt, as per provisional data with BigMint.

Higher availability, lower raw material prices: A significant portion (81%) of sponge iron production is based on coal-based processes, capitalising on India’s abundant coal reserves and established production units in mineral-rich states. The higher availability of sponge iron tilts the balance in its favour compared to ferrous scrap, although domestic generation of scrap has been growing.

DRI production also received support from lower raw material costs, with both thermal coal and pellet prices trending down y-o-y throughout 2024. Portside prices of imported South African coal declined by 14% in CY’24. BigMint’s PELLEX witnessed a minor fall of 0.3% in CY’24. These factors helped lift sponge iron output and increase its availability in the market. Higher sponge iron exports: Data show that India’s sponge iron exports have grown to 1.3 mnt till December of the current fiscal from a level of 0.7-0.9 mnt in FY’19 and FY’20. This is due to expansion in steelmaking capacity in India’s neighbourhood and the growing demand for the metallic product. This is also supporting domestic production.

Higher sponge iron exports: Data show that India’s sponge iron exports have grown to 1.3 mnt till December of the current fiscal from a level of 0.7-0.9 mnt in FY’19 and FY’20. This is due to expansion in steelmaking capacity in India’s neighbourhood and the growing demand for the metallic product. This is also supporting domestic production.

Mid-term outlook

The domestic sponge iron market is poised for continued expansion:

Production capacity expansion: In keeping with the increased demand for DRI, producers are focusing on ramping up their facilities. Estimates place India’s DRI capacity at 62.6 mnt in FY’24, which is projected to rise by 10% y-o-y to 68.8 mnt by the end of FY’25. BigMint projects that India’s sponge iron capacity may surpass 70 mnt by FY’30, driven by ongoing investments in infrastructure and industrial projects and growth in steel production.

Technological advancements: Emphasis on improving production technologies and addressing environmental concerns is likely to enhance both the quality and quantity of sponge iron produced. Increasing adoption of ‘green steel’ norms by the government and toughening of the compliance framework, as well as increasing carbon prices, will eventually see a shift away from coal-based sponge iron production processes.

DRI in metallic mix: BigMint estimates that sponge iron usage in India’s crude steel production will drop to around 20-25% by FY’30 compared with 28% in FY’24, with the share of the BF-BOF route in total production increasing to 55% in FY’30 from 43% in FY’24. However, sponge iron production and consumption, in absolute terms, will grow with the surge in steel production.

Leave a Reply