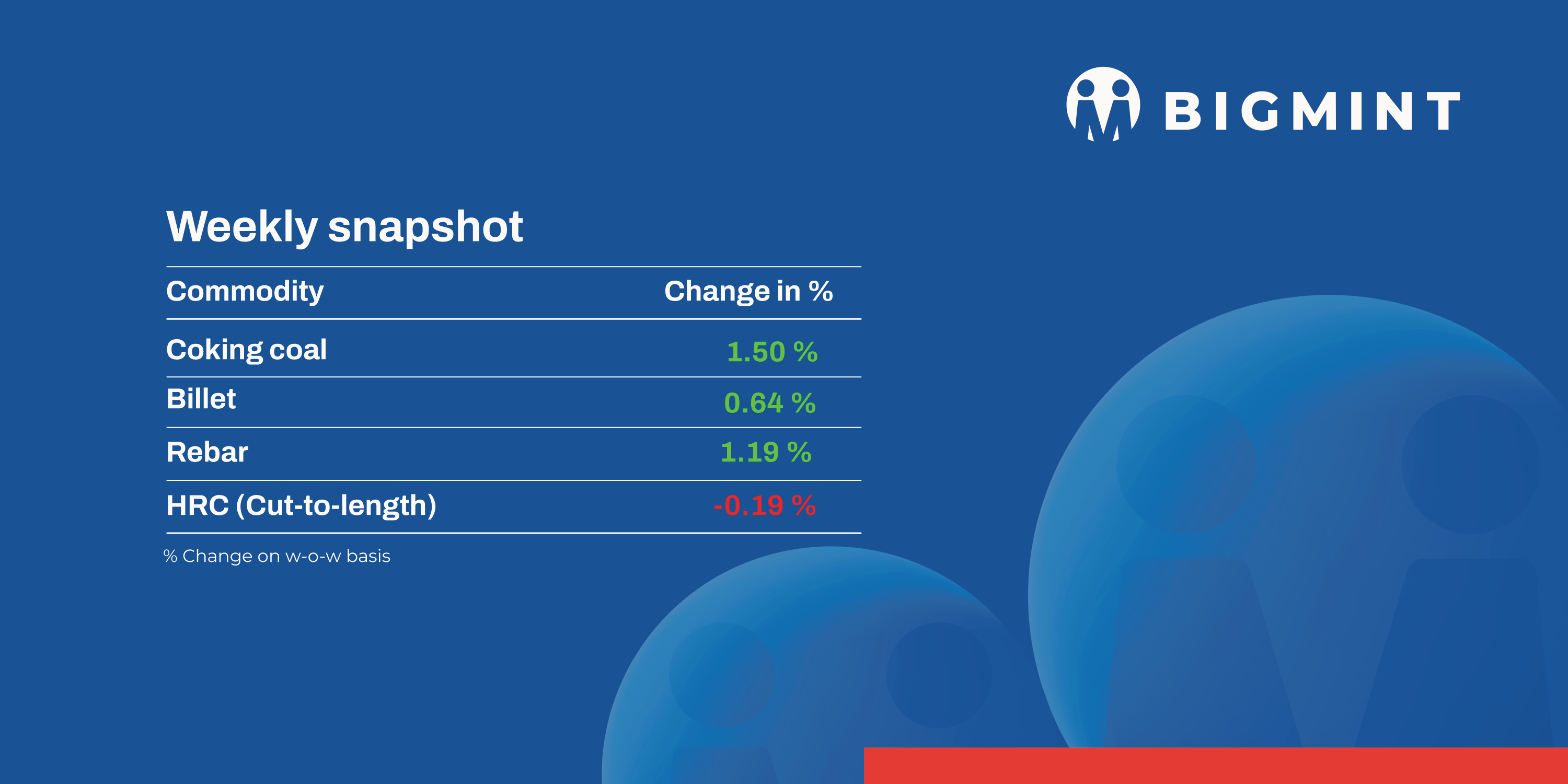

The domestic steel market saw a positive trend in prices during week 7 ( 10-15 February, 2025), as semi-finished steel prices edged up by INR 100-900/tonne (t) across regions.

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, remained stable w-o-w at INR 9,800/tonne (t) DAP Raipur on 14 February. India pellet (Fe 63%, 3% Al) export index (FOB east coast remained stable w-o-w at $105/t on 14 February. A domestic pellet maker concluded an export deal for around 50,000 t of pellets (Fe 63%, 2% AL2O3) at $110-112/t FOB India. Another export deal of 55,000 t pellet was recorded at $117/t CFR China from the east coast

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index rose by $1.5/t w-o-w to $69.5/t FOB east coast, India, on 13 February. However, prices fell by $1/t against the previous assessment on 10 February. This week, approximately 250,000 t of iron ore fines were traded for exports from India. While some exporters received bids from buyers, negotiations continued without final deals in certain cases.

- NMDC auctioned 186,300-t iron ore from Chhattisgarh on 13 February – 92% failed to fetch bids; around 14,300 t were sold. From Bacheli, out of 21,500-t DR-CLO (10-40 mm, Fe 67%), 4,300 t sold at INR 7,130/t (base price); entire 10,000-t Baila-sized lumps (10-20 mm, Fe 65.5%) lot booked at INR 6,500/t (base price); 94,600-t fines (Fe 64%) unsold. However, 60,200-t ROM (10-150 mm, Fe 65.5%) unsold. Prices were on FOR, ex-stockpile/mines basis, including royalty, DMF, and NMET.

Coal

- Portside South African thermal coal prices steady: RB2 (5500 NAR) remained at INR 8,650/t exw-Gangavaram, while RB3 (4800 NAR) held at INR 7,250/t. Weak demand and domestic supply competition kept prices unchanged.

- Thermal coal inventories at Indian ports increased: Stocks rose by 0.7% w-o-w to 13.76 mnt in week 6 of CY’25, as per BigMint data. Despite higher inventories, subdued demand kept market activity low.

- India’s domestic met coke prices stable: 25-90 mm BF-grade coke stood at INR 34,000/t exw-Jajpur and INR 32,000/t exw-Gandhidham, with limited imports preventing price movement.

Ferrous scrap

- India’s imported scrap market saw a slight price increase, but buying interest remained weak due to sluggish finished steel sales and a depreciating INR against the USD. UK-origin shredded scrap rose 2% w-o-w to $380/t CFR from $373/t, yet buyers stayed hesitant amid higher import costs and competitive domestic alternatives.

- Despite the price uptick, momentum remained low as the bid-offer gap persisted.

- Approximately 7,000-8,000 t of scrap were booked, including 2,000-3,000 t of HMS (80:20) from South America and West Africa at $345-362/t, 1,000-1,500 t of shredded scrap from South America at $370/t, 500 t of LMS Bales from Singapore at $310/t, 500 t of Turning Boring from Malaysia at $320/t, 250 t of HMS-LMS Bundle mix from Yemen at $340/t, 1,000 t of PNS from Kuwait at $370/t, and 1,000 t of NTP from the EU at $365/t.

Ferro Alloys

- Silico manganese: Indian silico manganese prices surged to a seven-month high, increasing by INR 1,550/t ($13/t) w-o-w to INR 72,900-74,300/t ($839-855/t) in key regions of Durgapur, Raipur and Vizag. This follows a rise in export prices w-o-w due to increasing demand and limited supply.

- Ferro manganese: Indian ferro manganese (HC 70%) prices went up by INR 1,000/t ($12/t) to INR 76,000/t ($875/t) exw in Durgapur. Prices exw-Raipur were also up by INR 600/t ($7/t) and stood at INR 76,000/t ($875/t). Prices increased because of production cuts and improved export inquiries.

- Ferro silicon: Indian ferro silicon prices increased by INR 500/t ($6/t) w-o-w to INR 101,400/t ($1,167/t) exw-Guwahati. Prices also surged by INR 1,200/t ($14/t) in Bhutan to INR 101,600/t ($1,169/t) exw. Prices increased because most sellers in northeastern India had limited material available for sale, which encouraged them to raise offers.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were rose by INR 900/t ($10/t) w-o-w at INR 98,200/t ($1,130/t) exw-Jajpur. Prices increased following material shortages and a boost in export demand.

Semi-finished

- Indian semi-finished steel prices showed mixed trends, as per BigMint’s assessment. Domestic billet prices in almost all key locations increased by INR 100-900/t, with a major increase of INR 900/t seen in the Goa market. In Mandi Gobindgarh, Durgapur and Ramagarh, prices slipped by INR 50-400/t ex. However, sponge iron prices also showed mixed trends; in almost all key locations prices decreased by INR 50-600/t, with a major decrease of INR 600/t seen in the Durgapur market. However, prices in the Bellary, Raigarh and Hyderabad markets moved up by INR 200-500/t

- Indian DRI (Direct Reduced Iron) export offers remained stable for CPT Raxaul, stood at $343/t while, CPT Benapole offers decreased by $1 stood at $338/t.

Finished Long Steel

- IF-rebar: India’s induction furnace route finished long steel prices saw a w-o-w increase, supported by improved buying activity. Steady procurement throughout the week led manufacturers to marginally raise prices and scale back discounts. Smooth lifting of previously booked material over the past 2-3 weeks has helped ease inventory pressure, with stock levels now averaging 8-10 days, varying by region. Market participants expect prices to remain range-bound in the near term.

- W-o-w, in rebar steel prices witnessed hike of INR 200-1,000/t across the regions except in Jaipur market where prices dropped by INR 200/t as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 42,400-42,800/t exw Raipur, INR 46,800-47,400/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 44,200-44,600/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 43,200-43,700/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices showed mixed trends w-o-w, due to slow domestic demand and material shortages in key markets. As a result, some major private steel mills raised their list prices, leading to price increases in certain markets. Post hike, current list prices are hovering around INR 52,500-53,500/t on landed basis.

- Current week’s rebar prices (12-32mm) in the trade segment remained stable w-o-w at INR 52,700/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the project segment, prices ranged between INR 50,000-51,000/t FOR Mumbai, with cautious buyers and limited purchasing activity.

Flat Steel

- Hot-rolled coil (HRC) prices across India remained stable w-o-w at INR 47,400-49,500/tonne (t). Conversely, cold-rolled coil (CRC) prices witnessed mixed trends w-o-w, settling at INR 53,000-55,700/t ($617-671/t) across markets. The market is experiencing weak demand, and buyers are not accepting the price increases.

- Imports of bulk HRCs and plates stood at 195529t till 10 February 2025, as per vessel line-up data maintained with BigMint. It is expected that an additional 1,22,115 t will be imported by the month-end.

- BigMint’s India hot-rolled coil (HRC, SAE1006) export index for the Middle East and Vietnam remained stable week-on-week. However, exports to Europe continued to struggle due to ongoing anti-dumping investigations.

- The anti-dumping investigations have slowed Indian HRC exports to Europe, with S275 (3 mm thickness) quoted at $590-595/t CFR Antwerp ($540-545/t FOB, east coast India).

Leave a Reply