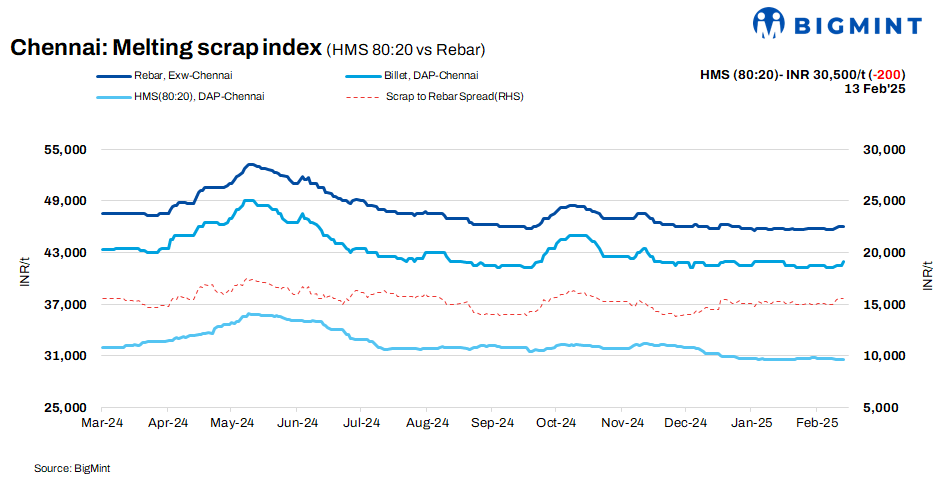

Chennai’s HMS (80:20) scrap prices saw a decrease of INR 200/t w-o-w, settling at INR 30,500/t. Despite this drop, prices remained stable day-on-day (d-o-d). On the other hand, billet prices increased by INR 500/t d-o-d, reaching INR 42,000/t, up INR 800/t w-o-w. Rebar prices also showed an uptick of INR 300/t w-o-w, now at INR 46,000/t, while they remained unchanged d-o-d. The market remains relatively steady with gradual price movements.

Imported, domestic market trends

Shredded scrap from the UK is being offered at $375-380/t CFR Chennai, while HMS 80:20 is priced at $355-360/t. However, demand for these imported materials has been weak, as buyers are leaning toward more affordable domestic scrap options. Domestic scrap is priced lower than imported material making it the more attractive choice for many buyers, impacting the overall demand for overseas scrap.

Domestic prices for HMS (80:20) scrap is in the range of INR 30,000-30,500/t for buyers who settle deals within seven days. For transactions involving extended credit terms, prices rise to INR 30,500 to INR 31,000/t. Most offers are concentrated within the INR 30,200 to INR 30,500/t band, with the majority of deals being finalised at these levels, reflecting a stable market.

Buyer-supplier sentiments

A mill representative recently reported to BigMint that trade activities in the steel sector have slowed since the previous month, with both major project sales and retail transactions experiencing a downturn. This has led to reduced demand for finished steel. A key factor contributing to this slowdown is liquidity concerns, as mills are struggling with cash flow issues, leading to delays in raw material payments by up to 30 days.

The price range for HMS 80:20 scrap is currently between INR 30,000-31,000/t, depending on payment terms, according to a scrap supplier. A liquidity crunch in the market has led to a slowdown in trade activity in recent weeks. Additionally, there has been higher consumption of sponge iron in the charge mix during this period. Major mills are currently operating at 50-60% of their production capacity, reflecting a restrained market environment.

Regional comparison

In the Jalna market, located in western India, rebar and HMS 80:20 prices remained stable d-o-d, priced at INR 47,100/t and INR 31,700/t, respectively. Billet prices increased slightly by INR 100/t to INR 41,900/t d-o-d. Despite these price movements, trade activity in finished steel has been moderate, with liquidity constraints continuing to affect the market. Major buyers are currently bidding for scrap in the INR 31,500-32,000/t range.

Outlook

Despite the current slowdown, scrap prices may remain within a relatively narrow range in the near term, with potential fluctuations of INR +/- 500 per tonne. These fluctuations will be influenced by prevailing market conditions, which may affect price stability in the short term.

Leave a Reply