- Turkish scrap prices rise amid firm US-origin deals

- US tariffs push scrap surge; recyclers hold offers firm

Turkish deep-sea bulk ferrous scrap prices increased by $5/tonne (t) w-o-w, driven by a higher-priced US-origin deals that prompted stronger offers from other recyclers, supported by a robust domestic buying week for February.

In the past seven days, around eight-nine deals were concluded for Turkiye, with six deals for HMS from the Baltic and EU regions at $348-353/t, while HMS, shredded, and bonus were priced within $347-379.5/t CFR Turkiye.

US ferrous scrap prices saw their sharpest increase this week, with most February-delivered trades finalised, driven by rising finished steel prices. The $29-30/t m-o-m jump from January 2025 lowest Prices recorded at $332/t.

BigMint’s price assessments

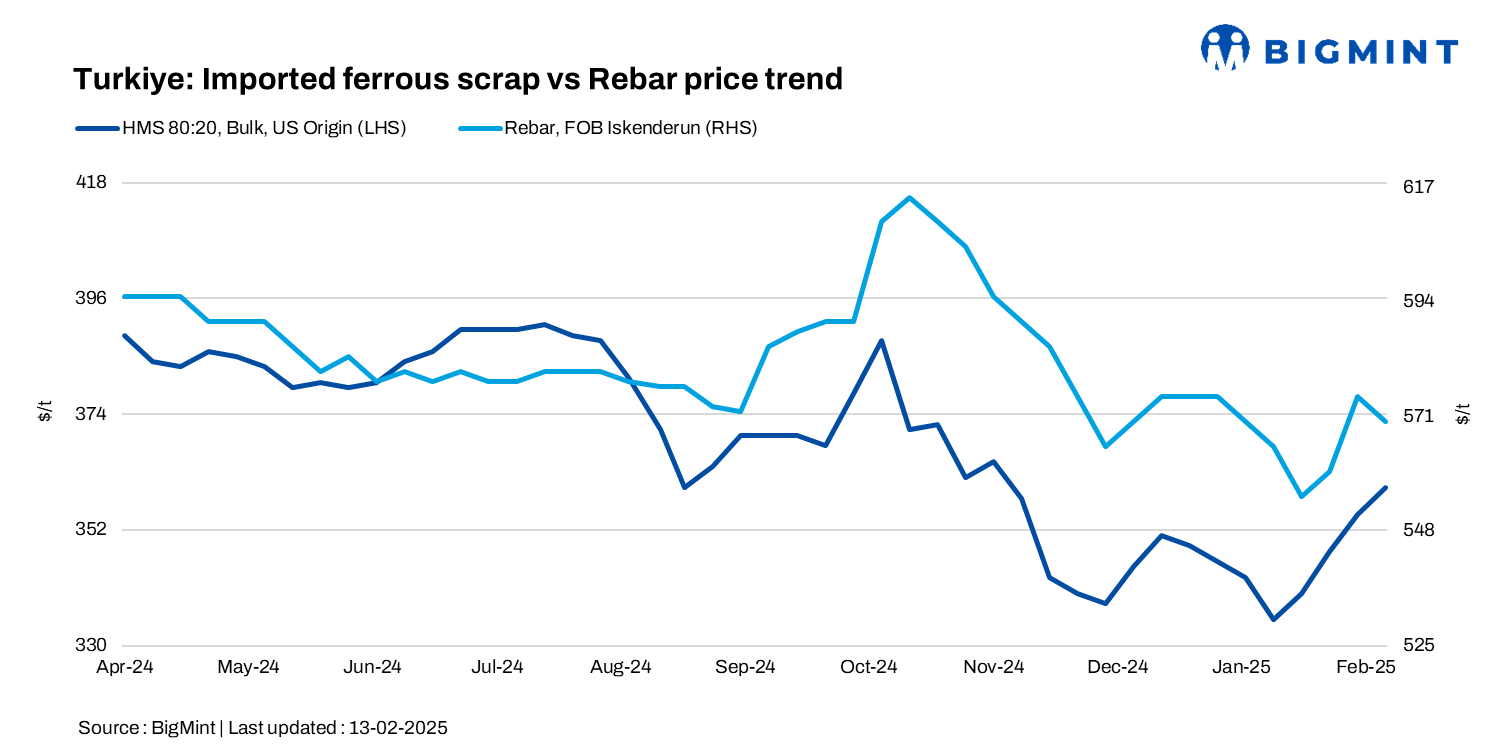

- US-origin HMS (80:20) bulk scrap stood at $360/t CFR Turkiye, up $5/t w-o-w.

- Bulk HMS (80:20) from the US East Coast was at $338/t FOB, also up $3/t w-o-w.

The scrap-to-rebar spread increased w-o-w to $210-215/t, with rebar export prices at $570-575/t FOB.

Workable prices for US and Baltic-origin HMS (80:20) were indicated between $355-360/t CFR, with US sellers holding firm at a minimum target of $360/t CFR.

Recent deals

- Baltic-origin (Aegean region): HMS (80:20) at $355/t

- EU-origin (East Marmara region): HMS (80:20) at $353/t

- UK-origin (Aegean): 18,000t HMS (80:20) and bonus priced at $347/t and $367/t.

- Baltic-origin (Mediterranean): HMS (80:20) at $351/t.

- EU-origin (West Marmara): HMS (80:20) at $348/t.

- UK & Baltic (Mediterranean): HMS (80:20) at $352.5/t.

- US-origin (Mediterranean): 26,000 t HMS (80:20) & PNS at $359.5/t & 379.5/t.

- EU-origin (Black Sea region): HMS (80:20) at $353/t.

Domestic Scrap in the US, combined with higher export offers, strengthened recyclers in the Baltic region. Baltic-origin HMS (80:20) was offered at $363-370/t CFR.

US scrap recyclers grew more confident following a sharp rise in domestic prices after the announcement of tariffs on all steel and aluminum imports to the region.

Market scenario

A Turkish mill-side participant commented, “Offer prices are exceptionally high. With sluggish rebar sales, the surge in scrap costs is only adding to the challenge, leading mills to increase billet purchases and reduce scrap demand.”

The European and Baltic sellers were less aggressive than their US counterparts, as sluggish demand from European mills kept export prices appealing for recyclers, despite increasing HMS collection costs at the docks.

A EU based recycler noted, “Currently, it’s important to sell whenever Turkish mills are buying, as missing an opportunity can leave sellers at a disadvantage and under pressure. When mills are out of the market, prices tend to be less favorable.”

A UK based trader stated that “A deal at $355/t CFR Europe wouldn’t be surprising, as US recyclers are unlikely to accept offers close to $360/t CFR at this point.”

Outlook

Recent bookings have strengthened seller sentiment. A recycler mentioned that there may be expectations of higher domestic prices due to the tariffs. If US President Donald Trump implements a 25% tariff on all steel, steel prices could rise further. This move may drive domestic mini-mills to ramp up production and increase scrap consumption, at least in the near term.

Leave a Reply