- Tags rise in Vietnam, SK amid strong demand

- Slow construction activity limits buying in B’desh

Japanese H2 scrap export offers declined w-o-w amid sluggish activity as buyers made a slow return from their holidays. Seaborne demand remained weak, with buyers waiting for price cues from China’s post-holiday market. Persistent port congestion in Japan delayed shipments, shifting some February orders to March.

BigMint’s latest assessment recorded a slight dip of JPY 400/t ($3/t) in H2 export prices, to JPY 41,600/t ($274/t) FOB Tokyo Bay as of 7 February.

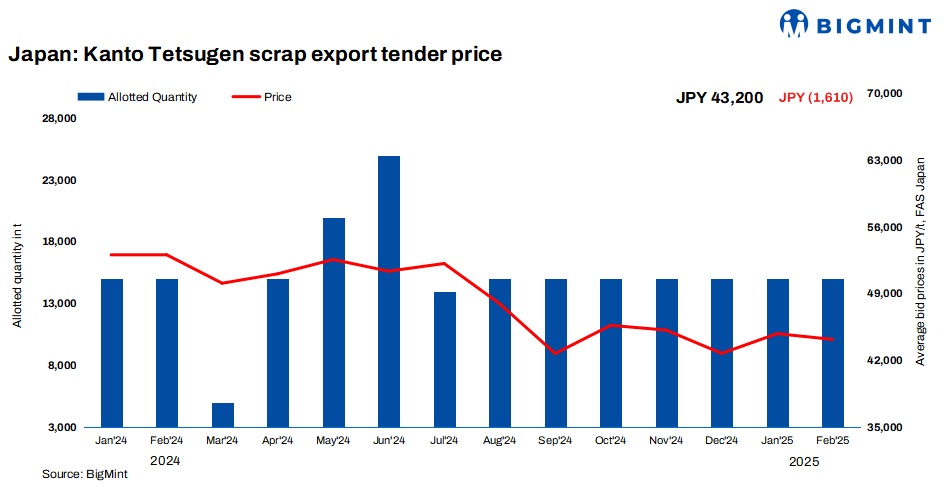

Meanwhile, the Kanto Iron and Steel Cooperative’s February export tender saw bids fall $10/t m-o-m (JPY 1,610/t). The 15,000-t H2 lot was awarded to a Bangladeshi mill at JPY 43,200/t ($281/t) FAS, reflecting limited buying activity as traders awaited clearer market trends.

Other market updates

Bangladesh: Despite a Bangladeshi mill securing the Kanto tender, overall scrap procurement in Bangladesh slowed w-o-w due to weak steel demand amid sluggish construction activity and stalled government projects. As a result, some mills reduced rebar prices by BDT 2,000-3,000/t w-o-w, with Chattogram offers now at BDT 87,000-88,000/t ($714-721/t).

Local scrap prices remained weak, with PNS at BDT 58,500/t ($481/t) and HMS at BDT 56,000-57,000/t ($460-468/t), while progress in construction activity and government projects remained slow.

Imported containerised scrap prices increased w-o-w due to a global supply crunch, though workable levels remained $5-6/t below offers.

Bulk scrap prices showed mixed trends, with limited buying interest except from major bulk players.

Vietnam: The Vietnamese imported scrap market saw a rebound last week, as key buyers returned from the holidays and market activity gained momentum. Japanese bulk H2 scrap was offered at $315-320/t CFR Vietnam, marking a $5-10/t increase w-o-w, while bids rose to around $310-312/t CFR Vietnam.

This price rise was driven by a recovery in demand following a slowdown in procurement and lower shipments to Vietnam in January. Additionally, mills had restocked ahead of the holidays, and the price increase reflects expectations of stronger demand as the market picks up after a quiet period.

Taiwan: Feng Hsin Steel, Taiwan’s largest rebar producer, kept its rebar list prices unchanged for transactions during 10-14 February, offering 13-mm rebars at TWD 18,000/t ($548/t) exw. However, the company raised its local scrap procurement prices, with HMS (80:20) increasing by TWD 300/t ($9/t) w-o-w to TWD 9,200/t ($280/t), following a rise in global scrap tags.

While global scrap prices have continued to climb, with US-sourced HMS (80:20) at $310/t CFR Taiwan and Japanese H2 scrap reaching $315/t CFR Taiwan, Feng Hsin has not adjusted its rebar prices yet. The company cited subdued demand from downstream users and weak rebar sales in the spot market as factors influencing its decision.

South Korea: South Korea’s imported scrap market saw a surge in arrivals, to 109,750 t this week, a sharp rebound from January’s 7,000 t overall. Around 72% of imports were driven by plate and special steelmakers, while shaped steel manufacturers remained subdued due to weak construction demand.

Major buyers included Hyundai Steel, POSCO, and SeAH Besteel. Meanwhile, domestic scrap inventories at major mills fell 11% w-o-w, with sharper declines in the central region, raising concerns over supply shortages.

Major South Korean steelmakers, increased their steel scrap purchase prices, effective 11 February 2025. Hwanyang Steel, Korea Special Steel, Daehan Steel, YK Steel, and Dongkuk Steel’s Incheon Plant raised prices by KRW 10,000/t ($7/t) for all grades. SeAH Besteel followed suit, increasing prices by KRW 10,000/t ($7/t) for most grades, with a higher rise of KRW 15,000/t ($10/t) for certain raw and heavy iron grades.

Outlook

The Japanese H2 scrap market is expected to slow down following the Kanto tender result, as well as ongoing uncertainty surrounding the US imposing tariffs on China. Buyers are holding back on significant purchases, awaiting clearer market direction.

Leave a Reply