- Challenges of weak demand, currency volatility persist

- Bid-offer gaps widen in India, demand a concern

South Asia’s imported scrap market faced persistent challenges as weak demand, currency volatility, and liquidity constraints kept trade subdued. Buyers remained cautious amid fluctuating freight rates and limited financial flexibility, particularly in Pakistan and Bangladesh. In India, bid-offer gaps widened, with secondary mills struggling to secure material at viable rates. Despite a stable pricing trend, demand concerns overshadowed any potential upside.

Pakistan’s market remained under pressure due to cash flow issues and lack of major government projects, while Bangladesh saw sluggish trade despite slight optimism ahead of Ramadan. In contrast, Turkiye’s scrap market showed some resilience, with prices inching up amid improved sentiment.

Overall, while price corrections seemed limited, the near-term outlook remained cautious, with demand yet to show meaningful recovery.

Overview

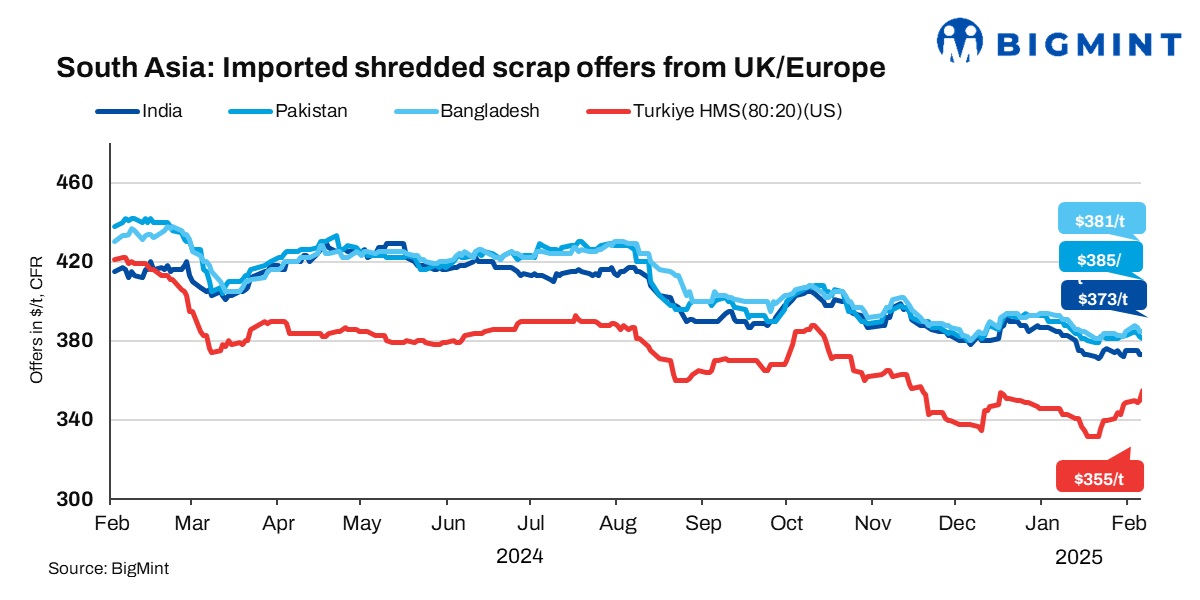

India: India’s imported scrap market remained under pressure due to currency fluctuations, bid-offer mismatches, and weak domestic steel market support. Indicative offers for shredded scrap from the UK/Europe stood at $370-375/t CFR Nhava Sheva, while bids hovered at around $360-365/t CFR. HMS (80:20) from the UK/Europe was assessed at $350-355/t CFR, with buyers targeting around $345/t CFR. Meanwhile, West African HMS (80:20) offers ranged between $345-355/t CFR.

A US-based trader remarked, “No signs of improvement yet. Deals remain tough due to the pricing gap, especially for material from the US, EU, and Australia to India. Additionally, some freight rates from the US have surged, making sales difficult. It depends on the port, but from the West Coast, we were getting rates at $1,800/t last month. Now, these have jumped to $2,400/t for a 40-ft container. Currently, we are seeing a 2-4% gap in most bids.”

Pakistan: Pakistan’s imported scrap market remained sluggish, on weak demand due to cash flow constraints and a struggling construction sector. UK-origin shredded was quoted at $382-385/t CFR Qasim, but buyers resisted beyond $378-380/t CFR. UAE-origin HMS offers stood at $365/t CFR. Local scrap prices ranged from PKR 142,000-147,000/t, while rebar traded between PKR 240,000-250,000/t, depending on payment terms.

With no major government projects announced, buyer interest remained low, though LC-backed mills continued steady operations. Sellers faced pressure to adjust prices to sustain sales, but raw material costs stayed challenging.

Meanwhile, Pakistan has extended the 10% and 5% Regulatory Duty (RD) on flat steel products until March 31, 2025, to support the domestic industry. The duty, initially set to expire on 31 December, 2024, will revert to 0% and 5% from 1 April, 2025, following recommendations from the Tariff Policy Board.

Bangladesh: Bangladesh’s imported scrap market remained sluggish as weak construction demand and falling rebar prices made mills cautious. Major mills in Chattogram reduced rebar rates by BDT 2,000 to BDT 87,000-88,000/t, while Dhaka mills offered at BDT 82,000-84,000/t.

Shredded scrap offers from Malaysia/Singapore stood at $375-380/t CFR, PNS at $385/t CFR, and Australian HMS (90:10) at $370-375/t CFR.

Bulk shipments dominated trade, while containerised scrap saw limited interest due to LC constraints.

Local scrap hovered at BDT 56,000-58,500/t, with shipyard scrap at BDT 54,000-55,000/t.

Despite slight optimism ahead of Ramadan, the outlook remains cautious, with demand yet to stabilise.

Meanwhile, BSRM inaugurated a new eco-friendly steel plant in Chattogram, boosting domestic production with JICA-backed funding. The plant will add 500,000 t of rebar, 100,000 t of wire rods, and 250,000 t of billets annually while enhancing sustainability by reducing greenhouse gas emissions and promoting a circular economy.

Turkiye: Turkiye’s imported scrap market saw a slight uptick, with US-origin bulk HMS (80:20) offers at $355/t CFR, up $5/t. An Iskenderun mill booked EU-origin HMS (80:20) at $350/t CFR and bonus scrap at $370/t CFR.

Indicative tradable levels for US/Baltic-origin scrap ranged between $350-360/t CFR, while EU-origin offers stood at $360-362/t CFR.

Market sentiment remained firm as buyers and sellers assessed the latest price movements.

Price assessments

India: UK-origin shredded indicatives were assessed stable d-o-d at $373/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives were at $381/t CFR Qasim, down $1/t d-o-d.

Bangladesh: UK-origin shredded was assessed unchanged d-o-d at $385/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap edged up by $5/t d-o-d to $355/t CFR Turkiye.

Outlook

According to market participants, prices are unlikely to decrease in the near term in the international markets, with the primary issue being weak demand. Secondary mills in India are facing significant challenges in securing material. Additionally, a depreciation of the dollar in the short term seems unlikely, especially with the potential for the US to impose tariffs on various products.

Leave a Reply