- Active fixtures seen in Australia-China route

- Baltic Capesize index falls by 109 points w-o-w

Dry bulk iron ore freights exhibited mixed trends this week amid subdued market activity due to the Lunar New Year holidays, a shortage of fresh cargoes in the Indian Ocean, and an oversupply of tonnage. With Chinese participants gradually returning to the market, many were in a wait-and-watch mode, leading to limited fixing activity and preventing significant rate fluctuations. Additionally, while bunker prices saw an upward movement, the overall market remained cautious, with ship owners primarily collecting bids rather than aggressively fixing deals, thereby maintaining stability in freight rates.

The slight increase in Capesize freight rates could be attributed to tighter vessel availability for specific loading windows, increased demand for iron ore shipments from certain regions, or market sentiment shifts following prior rate declines. Meanwhile, active fixtures in Australia-China route supported the freight rate.

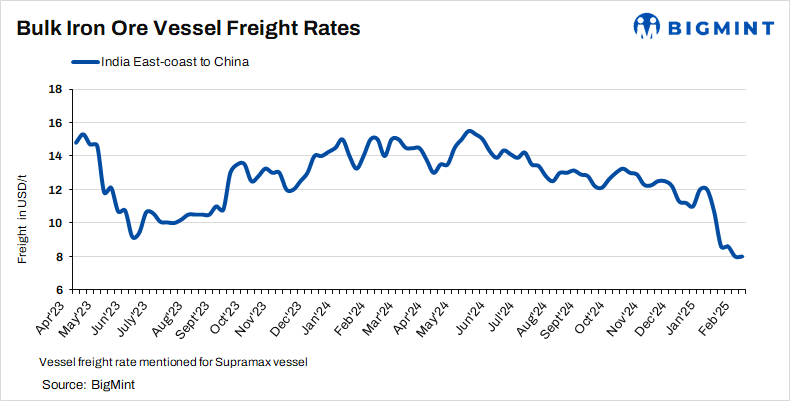

According to BigMint’s assessment, Asia-Pacific Supramax dry bulk freights (50,000-55,000 t) for iron ore shipments from the east coast of India to China remained stable w-o-w at $8/t on 5 February.

Factors influencing freights

- Baltic indices fall w-o-w: The Baltic Dry Index (BDI) was recorded at 735 points on 5 February, down by 43 points w-o-w. Meanwhile, the Baltic Capesize Index (BCI) stood at 874 points, decreasing by 109 points w-o-w. Additionally, the Baltic Supramax Index (BSI) inched down by 36 points w-o-w to 603 points, reflecting lack of demand.

- China’s iron ore spot prices unchanged w-o-w: China’s spot prices of iron ore fines (Fe62%) were assessed at $105.45/t CFR on 4 February, stable w-o-w as the market remained subdued during the Lunar New Year holidays. Sentiment was mixed over potential supply disruptions due to cyclones impacting Rio Tinto’s western operations. While concerns over supply tightness surfaced, sufficient inventories at Chinese ports helped offset immediate risks.

Route specifications

- India-China: Freights from the Indian Ocean to China were recorded at $8/t, firm w-o-w. Although demand from Chinese buyers was weak, a few fixtures remained under negotiation and are expected to be concluded next week.

- Australia-China: Freights for Capesize vessels carrying iron ore from western Australia to China were assessed at $6.20/t on 5 February, increasing by $0.4/t w-o-w. According to sources, major Australian miners Rio Tinto, FMG, and BHP were seen actively booking Capesize vessels from a Western Australia port to Qingdao Port at around $6.20-6.35/t. Shipment is scheduled for 16-22 February.

- Brazil-China: Freights for Capesize vessels from Brazil to China inched down this week. Rates from Tubarao to Qingdao Port were assessed at $16.9/t on 5 February, decreasing by $0.1/t w-o-w. As per sources, Vale booked a large vessel at a lower freight level of around $16.85/t for early March shipment.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port increased by $0.35/t w-o-w to $12.5/t. However, no fresh fixtures have been concluded in this route.

Leave a Reply