- Seaborne pellet exports from India remain subdued

- Domestic pellet prices show upward trend

The Indian pellet export market witnessed a slowdown over the past week due to the Chinese Lunar New Year holidays. Trade activities were largely muted as major Chinese mills and market participants remained absent, impacting Indian pellet exports via spot trades.

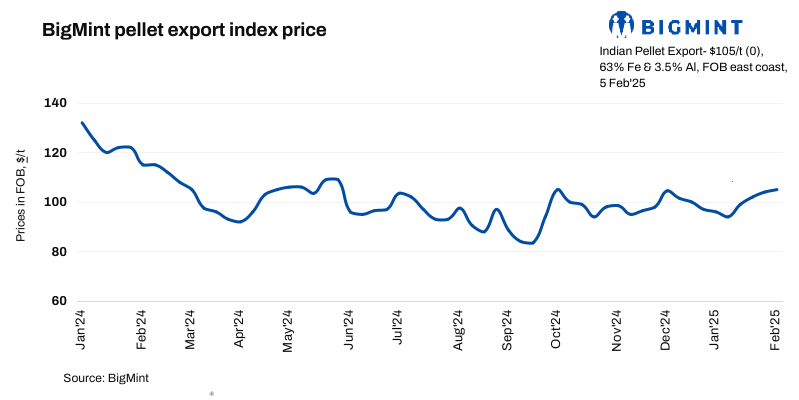

BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) stable this week so far at $105/t on 5 February 2025 as market is still awaiting clarity. Export activity in the seaborne market was subdued due to the Chinese holidays, and no export deal was witnessed from the east coast of the country.

A few export tenders for low-alumina pellets were concluded, which attracted good responses despite the overall subdued market sentiment. With the holidays now over, the seaborne market has resumed today; however, traders and buyers remain cautious, awaiting clarity on prices and future market trends.

An Indian pellet-maker concluded an export deal for around 50,000 t of pellets (Fe 63%, 2% AL2O3) at $108-109/t FOB India recently, sources informed BigMint. Last week, an export deal was concluded at a similar price level.

The gap between export and domestic realisations remained stable w-o-w and domestic prices exceeded export offers by INR 700/t ($8/t). Pellet (Fe63%) prices in Odisha’s Barbil were recorded w-o-w at INR 7,950/t ($89/t) exw. Meanwhile, ex-plant realisation in exports from Barbil stood at INR 7,200/t ($81/t) exw.

A seller commented: “Chinese mills have been largely inactive over the past week, which limited new export deals. However, with trading activities resuming, we expect price indications to become clearer in the coming days.”

Interestingly, during this period, the Indian domestic pellet market witnessed an uptick in prices, supported by active trades. Many sellers focused on completing previously concluded export deliveries while assessing future opportunities.

A trader informed, “Domestic demand has been strong, and we saw firm buying interest from local steelmakers. Exporters are currently watching global market movements before making further deals.”

Rationale

- No deal was recorded this week from the East Coast for the T1 trade. Thus, this category was taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for detailed methodology.

- Eleven (11) indicative prices were received, and Ten (10) were considered for the calculation of the index and given a 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices stable w-o-w: The benchmark iron ore fines index was largely stable w-o-w at $105/t CFR China on 4 February as the market remained subdued during the holidays. Sentiment was mixed over potential supply disruptions due to cyclones impacting Rio Tinto’s western Australia operations. While concerns over supply tightness surfaced, sufficient inventories at Chinese ports helped offset immediate risks.

- DCE iron ore futures drop: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract opened at a lower level of RMB 801/t ($107/t) on 5 February. Before the holidays, it had closed at RMB 810.5/t ($110/t) on 27 January.

- China’s portside pellet prices up w-o-w: Chinese sources said that Qingdao’s portside offers for Indian pellets (Fe 63.5%) rose by RMB 10/t ($1/t) w-o-w to RMB 965/t ($130/t) on 5 February, inclusive of all import taxes and port charges.

Outlook

According to BigMint, the trajectory of pellet prices in the seaborne market will become clearer this week. However, exporters are expecting stronger price trends in the coming days as recent export tenders received a good response.

Leave a Reply