- Major plant reportedly shut for maintenance

- Auto, manufacturing demand remains slack

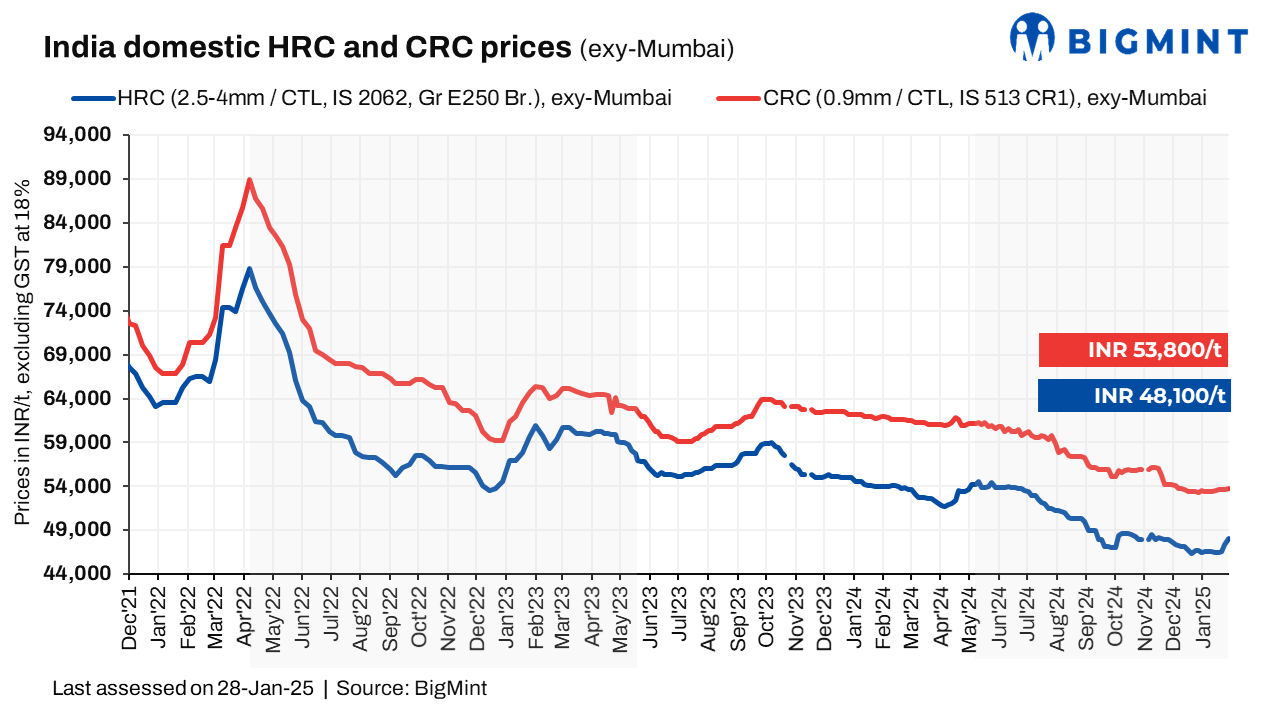

Hot-rolled coil (HRC) prices across India remained range-bound w-o-w at INR 46,800-49,000/tonne (t). Conversely, cold-rolled coil (CRC) prices witnessed mixed trends w-o-w, settling at INR 53,100-56,000/t ($617-671/t) across markets.

BigMint’s benchmark assessments (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL), however, increased by INR 700/t ($5/t) w-o-w to INR 48,100/t ($549/t) on 28 January 2025. Meanwhile, CRC (IS513, Gr O, 0.9 mm/CTL) prices increased marginally by INR 100/t w-o-w to INR 53,600/t ($628/t). These prices are quoted ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market updates

Major plant undertakes maintenance: There are reports that the HSM2 at JSW Vijayanagar is under major maintenance for 20-30 days, with an expected production loss of 150,000-170,000 t. However, this information has not been officially confirmed by the mill.

Trade segment sees mixed trends: The trade market exhibited mixed trends, with prices in most regions declining due to weak demand. However, Mumbai saw a notable increase in offers, to INR 48,000-49,000/t ($/t). Despite this, actual trades were executed largely at the lower end of the price range, at INR 48,000-48,500 ($/t).

“The Mumbai market has surged rapidly, with momentum inflating as quickly as a balloon. However, there is uncertainty around the sustainability of the price hikes and the future trajectory of the market. The primary driver behind this sudden increase is the declining availability of import stocks, which now account for approximately 20% of the market share. Additionally, widespread speculation about a potential price hike of INR 1,500-2,000 by mills next month, along with rumours regarding the implementation of a safeguard duty, has further fuelled bullish sentiments,” noted a market participant.

Auto, manufacturing demand remains slack: Subdued demand continues in the automotive and manufacturing segments, suggests the latest data. According to SIAM, automobile production in December 2024 dropped by 20% m-o-m to 1,921,268 units, continuing with the declining trend seen over the past three months. Sales also fell 26% m-o-m to 1,552,582 units, similarly marking a third consecutive monthly decrease.

The purchasing managers’ index (PMI) mirrored this trend, edging down to 56.4 in December from 56.5 in November and 57.5 in October.

Import trends: Imports of bulk HRCs and plates stood at 426,405 t till 27 January 2025, as per vessel line-up data maintained with BigMint. It is expected that an additional 9,133 t will be imported by the month-end and another 135,870 t in the first week of February.

Export offers resume amid Lunar New Year: BigMint’s India HRC (SAE1006) export index for the Middle East and Vietnam resumed after two months, as mills began to actively offer in the market again, driven by reduced Chinese offers during the Lunar New Year. Prices stood at $505/t FOB eastern coast of India. However, European demand was weak amid sluggish sentiment and anti-dumping investigations, with Indian offers to the region at $590-595/t CFR Antwerp ($540-545/t FOB).

Outlook

HRC pricing trends will depend on demand recovery and the confirmation of potential mill price hikes. Global factors, including Chinese market movements post-Lunar New Year and trade policy developments, will also play a crucial role in shaping India’s HRC market trajectory.

Leave a Reply