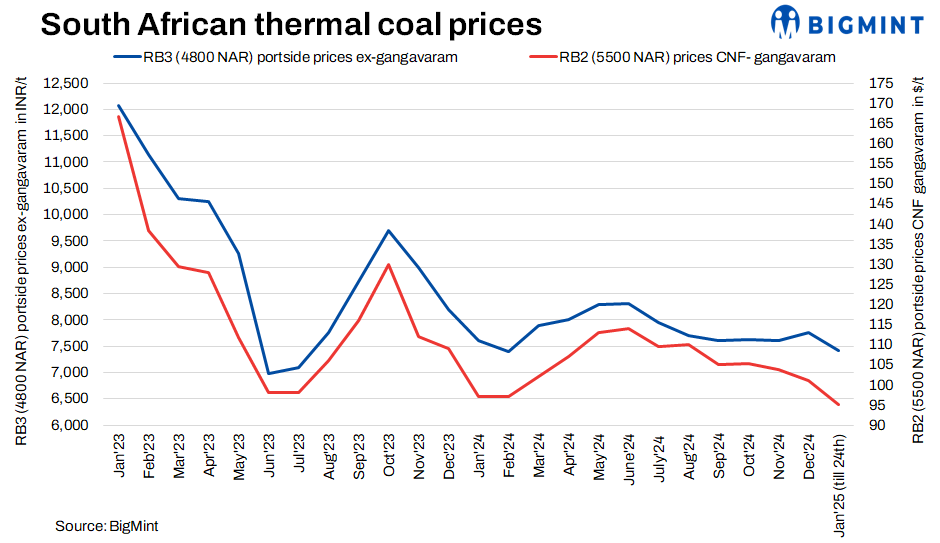

India’s portside prices for South African thermal coal remained largely unchanged this week due to subdued buying interest. RB2 (5500 NAR) prices hovered at INR 8,800/tonne (t), while RB3 (4800 NAR) prices stayed steady at INR 7,300/t, both ex-Gangavaram.

Sluggish demand from sponge iron manufacturers, several of whom are cutting or halting production, continues to weigh heavily on the market. Additionally, many buyers are utilising existing inventories or opting for cheaper domestic coal options.

Thermal coal inventories at Indian ports dropped by 2.3% to 13.89 million tonnes (mnt) in week 3 of CY’25 from 14.22 mnt in week 2, as per BigMint’s data.

Market overview

South Africa’s export prices fall slightly: South Africa’s RB2 (5500 NAR) export offers remained at $82/t FOB, while RB3 (4800 NAR) offers dipped slightly by $0.5/t w-o-w to $61.5/t FOB.

Domestic thermal coal prices drop: Domestic thermal coal prices in India saw a slight decline this week. 4500 GCV was assessed at INR 4,750/t, down by INR 50/t w-o-w, while 5000 GCV stood at INR 5,550/t, also down by INR 50/t, both exw-Bilaspur. Market sentiment remains cautious as domestic coal offers are expected to change following the recent SECL auction. With increased quantities available, prices are likely to face downward pressure as supply improves, particularly for key grades. Buyers may delay purchases in anticipation of further declines, adding to subdued demand.

Sponge iron prices stable: Sponge C-DRI prices were assessed at INR 25,600/t exw-Rourkela, unchanged w-o-w.

Outlook

India’s portside and imported thermal coal markets are likely to see continued pressure, with limited price improvement in the short term. Sponge iron production cuts, coupled with weak end-user demand and ample domestic supplies, are expected to sustain challenging market conditions.

Leave a Reply