- US mills favouring domestic scrap more than pig iron

- Winter weather, tariffs likely to push up scrap prices in Feb’25

US ferrous scrap export offers have risen by up to $13/t w-o-w amid tightening domestic supply and increasing scrap prices across major regions.

The domestic price gap between Busheling scrap and basic pig iron remains high, making scrap the more cost-effective option for mills. For instance, the spread between busheling scrap (delivered mill Chicago) and pig iron (Brazil FOB New Orleans) ranges from $60-100/t. As a result, mills are likely to continue favouring scrap unless pig iron prices stabilise or scrap prices increase further.

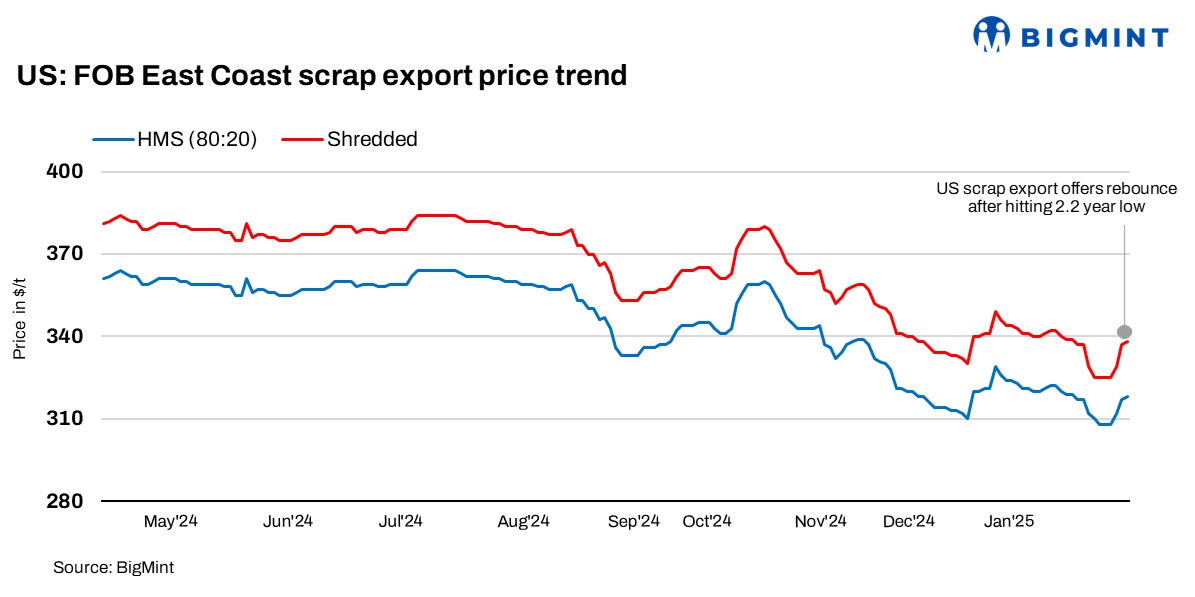

FOB assessments (US East Coast, bulk)

- Shredded rise by $13/t w-o-w to $338/t.

- HMS (80:20) increased by $10/t w-o-w to $318/t.

CFR assessments (bulk)

- HMS (80:20) was at $340/t CFR Turkiye, up $8/t w-o-w.

- HMS (80:20) stood at $335/t CFR Vietnam, down by $5/t w-o-w.

- HMS (80:20) was at $365/t CFR Chattogram, up $2/t w-o-w.

Updates on key buyers

Turkiye: The strong demand for US-origin scrap in Turkiye is driven by tightening supply and rising prices as mills look to secure materials for February shipments. Despite euro-dollar volatility, European recyclers have kept prices stable. US recyclers are reportedly targeting offers above $340/t CFR Turkiye, further reflecting the market’s tightening conditions.

Turkish deep-sea ferrous scrap prices rose, with HMS (80:20) reaching $340/t CFR, marking a recovery from the lowest levels since June 2022. Turkish mills have been actively sourcing scrap, expecting limited access to cheap material going forward. US-origin HMS (80:20) was priced at $340/t CFR.

Bangladesh: Demand for US-origin scrap in Bangladesh has been sluggish due to high inventory levels at major Chattogram-based mills and weak domestic market activity, particularly in Dhaka.

However, a Chattogram-based mill, currently operating at reduced capacity, is expected to resume purchases soon, hinting at a possible recovery in demand.

US-origin HMS (80:20) bulk prices rose by $2/t w-o-w to $365/t, with offers ranging from $366-372/t. Buyers, however, remained hesitant, keeping bids below $358-360/t. Shredded scrap offers from the US stood at $378-380/t, but limited buyer interest was noted.

Despite slight improvements in LC openings, bulk scrap inquiries remained muted, with major mills showing limited appetite for fresh purchases amid weak local steel demand and cautious market sentiment.

Vietnam: The Vietnamese imported scrap market saw a decline, mainly due to a gap between buyer and seller expectations.

HMS (80:20) deep-sea bulk scrap offers from the US were limited, driven by weak demand and differing price expectations.

This has kept the market subdued. US-origin HMS (80:20) deep-sea bulk cargoes were priced at $335/t, down $5/t w-o-w.

A mill participant in Vietnam noted that many are taking a cautious, wait-and-see approach, with some anticipating market fluctuations due to potential US-China tariff changes, adding uncertainty to pricing trends.

Demand in Vietnam remains soft, with mills holding sufficient inventories, minimal restocking before the Tet holidays, and slow market activity.

Outlook

Severe winter weather in the northern US, along with the anticipation of upcoming tariffs, is expected to push domestic scrap prices higher in February. A market participant mentioned, “Domestic scrap prices could increase by $20-22/t, driven by weather disruptions and prevailing market conditions.” These factors are likely to drive up scrap export prices as demand recovers in key steel sectors.

Leave a Reply