- Bids decline m-o-m for most grades at OMC’s chrome ore auction

- Tsingshan’s tender prices unchanged for Feb’25 deliveries

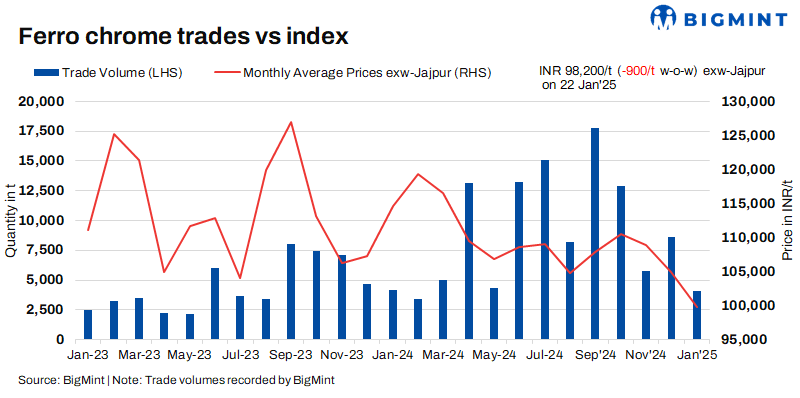

Indian high-carbon ferro chrome (HC60%, Si:4%) dipped by INR 900/t ($10/t) w-o-w in comparison to the previous assessment on 15 January. Prices fell as OMC’s chrome ore auction on 17 January witnessed m-o-m drop in bids for majority of the grades.

BigMint assessed Indian high-carbon ferro chrome (HC60%, Si:4%) prices at INR 98,200/t ($1,136/t) exw-Jajpur on 22 January. Approximately 600 t of deals were concluded last week in the price range of INR 98,000-98,500/t ($1,134-1,140/t) exw. Prices have fallen to 1.5 years low as similar levels were last seen in Jul’23, as per BigMint.

“We are waiting for prices to touch INR 95,000-96,000/t exw Jajpur levels. Hence we are holding back from booking at current levels”, highlighted stainless steel players.

Low-silicon ferro chrome prices came down by INR 1,100/t ($13/t) w-o-w to INR 104,900/t ($1,214/t) exw-Jajpur. In addition, low-carbon (C:0.1%) ferro chrome witnessed a drop in prices too, falling by INR 1,450/t ($17/t) w-o-w to INR 207,800/t ($2,404/t) exw-Durgapur.

Market over the week (16-22 January 2025)

Bids decline at recent domestic auction: At OMC’s chrome ore auction on 17 January, 59,100 t was sold out of 76,900 t offered. Prices for most grades fell by 4-7% (INR 801-1,306/t) m-o-m, while higher grades (48-54+%) surged by 29-39% (INR 7,237-7,785/t).

Additionally, at the Vedanta-FACOR’s ferro chrome auction on 20 January, buyer’s didn’t showed much interest in purchasing material. Base price for it was set at INR 98,500/t ($1,140/t) exw for bigger lot of 10-150 mm and INR 99,000/t ($1,145/t) exw for smaller lot. In reference to it, a source informed BigMint, “The feedback of the market is that there’s no demand at all.”

With the current state of the market, most of the producers are currently in wait-and-watch mode and offering material cautiously. On the other hand, a primary domestic buyer who’s monthly procurement is of around 3,000-4,000 t was quoted as saying, “Market is down currently which was evident at recent FACOR’s auction. I’m still bearish on the prices and will buy if material is offered at lower rates. Additionally, we have enough inventories to survive till April.”

Chinese tender price effect: Tsingshan, one of the major stainless steel manufacturer in China, kept its ferro chrome tender price unchanged m-o-m at RMB 6,995/t ($961/t) DAP, including taxes for February 2025. The tender prices usually serves as benchmark for suppliers to export material to China. The unchanged tender prices could be attributed to sufficient supplies along with sluggish demand of the stainless steel segment.

Domestic prices (HC60%) were unchanged w-o-w as well at RMB 7,200/t ($989/t) exw-Inner Mongolia.

Need-based buying continues to exert pressure at end-user market: Stainless steel prices for 304 grade HRC witnessed an uptick of INR 3,000/t ($35/t) w-o-w to INR 180,000/t ($2,083/t) exw-Mumbai. This rise was primarily driven by INR 2,000/t ($23/t) increase in 304 grade HRC’s and CRC’s by a major domestic producer due to rise in LME nickel price levels. However, overall buying interest remained weak and only need-based buying was done. A seller also recently informed that they’re currently operating at 50% capacity looking at current market trends.

Despite this, the market still remains optimistic, as the upcoming budget is expected to bring opportunities through government infrastructure projects. Industry participants are expecting improved demand and price movements following the budget.

Outlook

The market is lacking active trades as majority of sellers and buyers are in wait-and-watch mode. Hence, clarity regarding prices will only emerge after few days.

Leave a Reply