- Tight supply, price fluctuations support imports

- Australia remains largest supplier

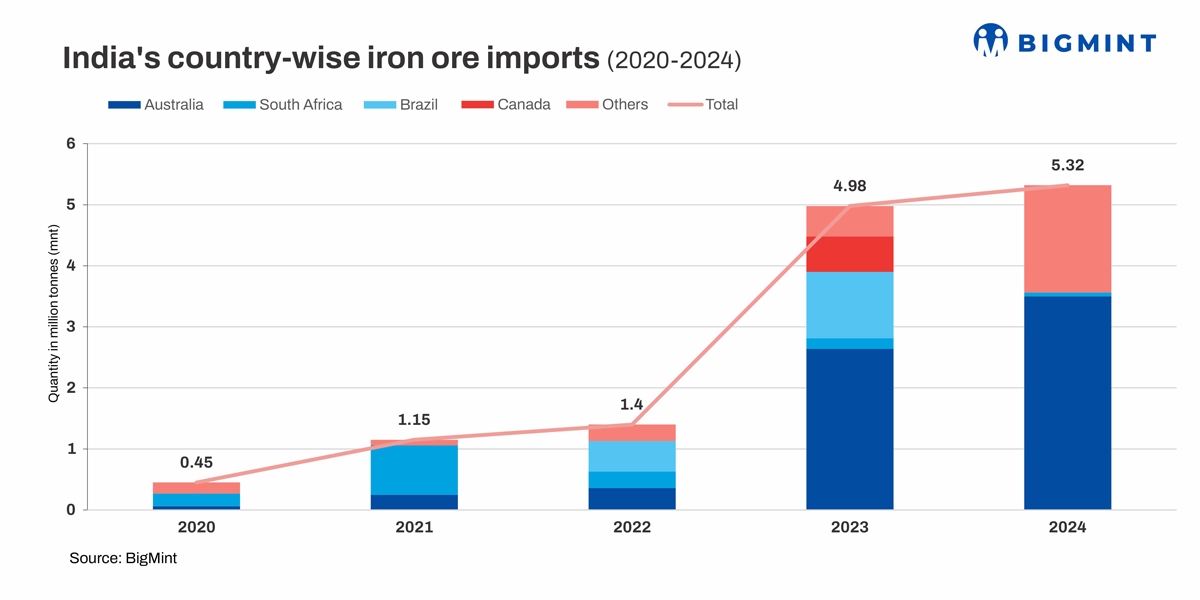

India’s iron ore imports reached 5.32 million tonnes (mnt) in CY’24. Volumes witnessed an increase of around 7% y-o-y against 4.98 mnt in CY’23 driven by factors such as rising domestic demand, supply constraints from key mining regions, and fluctuations in global iron ore prices.

After surpassing 1 mnt in November 2024 and reaching 1.19 mnt – the highest level in nearly six years – import volumes declined by approximately 16% m-o-m to 1 mnt in December 2024, data maintained with BigMint shows.

Australia leading exporter

Australia was the largest exporter of iron ore to India at 3.50 mnt in CY’24, a significant increase of 33% when compared to 2.64 mnt in the year-ago period.

Oman and Malaysia occupied the second and third position among the top exporters with 1.09 mnt and 0.60 mnt, respectively. However, according to sources, this was largely Brazilian ore which was routed to Oman and Malaysia post-processing from these units.

JSW largest importer

JSW Steel, with an import of 4.50 mnt, stood as the major iron ore importer in the period under review.

Port-wise imports

Amongst the ports, Jaigarh port accounted for the major share of 3.39 mnt of imports, followed by Krishnapatnam and Mumbai port at 1.02 and 0.91 mnt, respectively.

Why iron ore imports increased in CY’24?

- Higher crude steel production: India’s crude steel production witnessed a growth of around 6% y-o-y in CY’24. Production of crude steel in the country increased to around 149 mnt compared with 141 mnt recorded in CY’23. Data shows that the growth in production was undoubtedly spearheaded by the IFs which grew 14% y-o-y to 55 mnt against 48 mnt seen in CY’23.

- Domestic supply concerns: Tight domestic supply owing to extended monsoons, coupled with strong demand, has led to a rise in import volumes to fulfill the country’s industrial requirements. At the same time, domestic production has struggled to meet the increasing demand for iron ore in mid of the previous year, causing supply shortages. India’s iron ore output fell sharply by 27% to 19.25 mnt in July 2024, and declined further by 1% to 18.99 mnt in August, creating a need for imports to bridge the gap.

- Global iron ore price fluctuations: Iron ore prices in global markets remained volatile throughout the year, and Indian mills found it economically viable to import iron ore to maintain steady production. In March 2024, global prices for iron ore fines (Fe 62%) fell to approximately $100/t CFR China from $143/t CFR China in January 2024 and continued to exhibit volatility over the months, reaching around $90/t CFR China in mid-September 2024, according to data from BigMint.

- Logistical bottlenecks make imports cost-effective: Over and above the high domestic freight charges, logistical hurdles – transporters’ issue impacted dispatches in Odisha. Logistical difficulties which intensified during the monsoon season, tilted the balance in favour of imports for some coast-based mills. Notably, iron ore dispatches from Odisha declined by approximately 27%, reaching 14 mnt by mid-year under review.

- Quality issues of domestic ore: Domestic iron ore has a higher gangue content compared to imported ore. The level of alumina and silica in domestic ore is markedly higher than in Australian material. Thus, the latter is obviously better suited for sintering purposes and leads to higher efficiency in blast furnaces. Moreover, with most merchant miners having hit their EC limits, mining high grade ore became a challenge, compelling mills to look at imports more intently.

Outlook

Although import volumes have increased, the quantum is small with respect to India’s overall iron ore consumption, with demand expected to reach around 350 mnt in financial year 2029-30 (FY’30). With production rebounding post monsoons and global iron ore prices recovering to nearly $105/t CFR China towards the end-January 2025, fresh import bookings have slowed down, cited sources.

Leave a Reply