- Ample offers allow Turkish mills to secure lower tags

- US domestic prices may rise amid supply disruptions

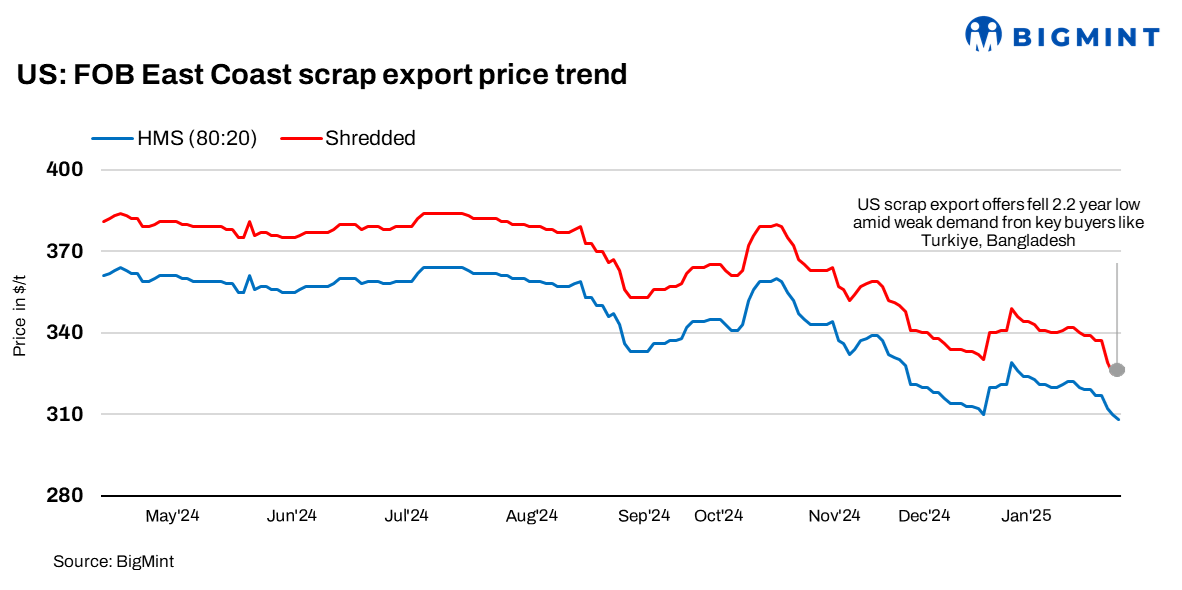

US ferrous scrap export offers fell by up to $14/tonne (t) w-o-w, as demand from key buyers such as Turkey and Bangladesh remained subdued.

Notably, the index has plunged to its lowest point in over two years, with similar levels last seen in November 2022.

In the domestic market, ferrous scrap prices are expected to rise in January in the Midwest and southeast, as mini-mills work on replenishing their depleted inventories.

A Midwest scrap dealer noted that heavy snowfall during the week ending 8 January disrupted scrap deliveries to yards in the Chicago area and possibly other regions. This supply disruption fuelled optimism about higher scrap prices for January.

FOB assessments (US East Coast, bulk)

- HMS (80:20) decreased by $11/t w-o-w to $308/t.

- Shredded fell by $14/t w-o-w to $325/t.

CFR assessments (bulk)

- HMS (80:20) was at $333/t CFR Turkiye, a dip of $10/t w-o-w.

- HMS (80:20) stood at $340/t CFR Vietnam, down by $8/t w-o-w.

- HMS (80:20) was at $363/t CFR Chattogram, dropping by $1/t w-o-w.

Buyer-side updates

Turkiye: Turkish demand for US-origin imported ferrous scrap was subdued, with buyers cautious due to weak finished steel sales. Prices of HMS (80:20) were assessed at $335/t CFR, reflecting an $8/t drop w-o-w. Mills took advantage of ample offers in the market, which allowed them the flexibility to restock at lower prices. Despite the availability of February shipments and leftover January cargoes, some sellers believe prices may have reached their floor.

However, some market participants were cautious, suggesting further price declines are possible. A Turkish mill source reported tradable values for US and Baltic-origin HMS (80:20) at $335/t CFR or slightly below, driven by limited steel demand. As US sellers were largely absent from the market this week, transaction volumes remained limited.

Bangladesh: Bangladesh’s demand for imported scrap was lower this week, with prices dropping by $5-6/t w-o-w. Bulk inquiries were mainly from large mills, while smaller buyers continued to bid below suppliers’ offers, leading to a slight price drop of around $1/t w-o-w for US-sourced HMS.

US-origin scrap prices ranged within $365-370/t, but bids were below $360/t due to cautious market sentiment. Despite this, Bangladesh’s scrap imports grew 9% y-o-y in CY’24, indicating ongoing reliance on US-origin scrap, though demand remains subdued at the moment.

Vietnam: Indicative deep-sea offers for US-origin cargoes were heard at $345-350/t CFR Vietnam, with bids ranging between $335-340/t. Amid limited offers and subdued demand, Vietnamese buyers turned to containerised HMS (80:20) as a cost-effective alternative. A Vietnam-based trader noted that mills are expected to restock minimally post-New Year due to weak sales.

Outlook

Limited demand from Turkiye and Bangladesh is likely to exert downward pressure on US export offers in the near term. Additionally, with an increase in domestic demand, material flow in the domestic market is expected to increase. Export prices are likely to remain subdued amid weak demand until there is some firm rebound in Turkiye and other regions.

Leave a Reply